- United States

- /

- Medical Equipment

- /

- NasdaqCM:NMTC

We Think NeuroOne Medical Technologies (NASDAQ:NMTC) Needs To Drive Business Growth Carefully

Even when a business is losing money, it's possible for shareholders to make money if they buy a good business at the right price. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. Having said that, unprofitable companies are risky because they could potentially burn through all their cash and become distressed.

So, the natural question for NeuroOne Medical Technologies (NASDAQ:NMTC) shareholders is whether they should be concerned by its rate of cash burn. For the purposes of this article, cash burn is the annual rate at which an unprofitable company spends cash to fund its growth; its negative free cash flow. The first step is to compare its cash burn with its cash reserves, to give us its 'cash runway'.

View our latest analysis for NeuroOne Medical Technologies

How Long Is NeuroOne Medical Technologies' Cash Runway?

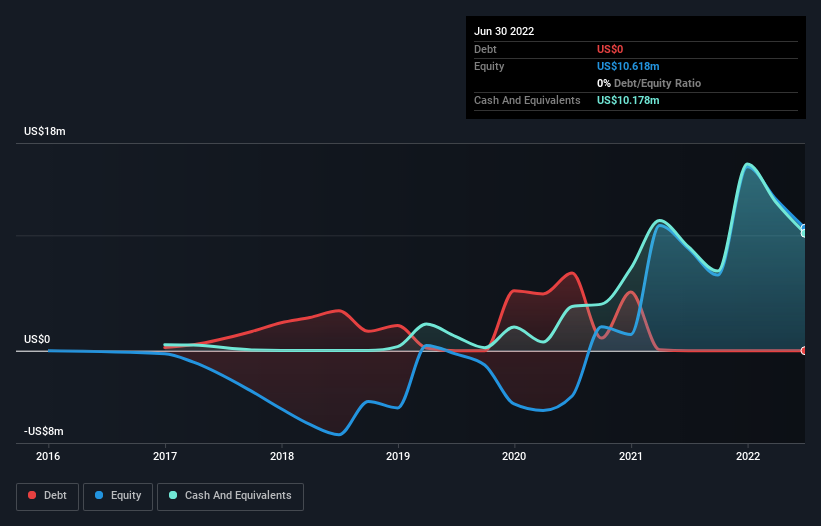

A cash runway is defined as the length of time it would take a company to run out of money if it kept spending at its current rate of cash burn. When NeuroOne Medical Technologies last reported its balance sheet in June 2022, it had zero debt and cash worth US$10m. Importantly, its cash burn was US$11m over the trailing twelve months. Therefore, from June 2022 it had roughly 11 months of cash runway. That's quite a short cash runway, indicating the company must either reduce its annual cash burn or replenish its cash. The image below shows how its cash balance has been changing over the last few years.

How Is NeuroOne Medical Technologies' Cash Burn Changing Over Time?

In our view, NeuroOne Medical Technologies doesn't yet produce significant amounts of operating revenue, since it reported just US$162k in the last twelve months. As a result, we think it's a bit early to focus on the revenue growth, so we'll limit ourselves to looking at how the cash burn is changing over time. Over the last year its cash burn actually increased by a very significant 69%. While this spending increase is no doubt intended to drive growth, if the trend continues the company's cash runway will shrink very quickly. While the past is always worth studying, it is the future that matters most of all. For that reason, it makes a lot of sense to take a look at our analyst forecasts for the company.

Can NeuroOne Medical Technologies Raise More Cash Easily?

Since its cash burn is moving in the wrong direction, NeuroOne Medical Technologies shareholders may wish to think ahead to when the company may need to raise more cash. Issuing new shares, or taking on debt, are the most common ways for a listed company to raise more money for its business. One of the main advantages held by publicly listed companies is that they can sell shares to investors to raise cash and fund growth. We can compare a company's cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year's operations.

Since it has a market capitalisation of US$35m, NeuroOne Medical Technologies' US$11m in cash burn equates to about 31% of its market value. That's not insignificant, and if the company had to sell enough shares to fund another year's growth at the current share price, you'd likely witness fairly costly dilution.

So, Should We Worry About NeuroOne Medical Technologies' Cash Burn?

NeuroOne Medical Technologies is not in a great position when it comes to its cash burn situation. Although we can understand if some shareholders find its cash runway acceptable, we can't ignore the fact that we consider its increasing cash burn to be downright troublesome. Looking at the factors mentioned in this short report, we do think that its cash burn is a bit risky, and it does make us slightly nervous about the stock. Separately, we looked at different risks affecting the company and spotted 7 warning signs for NeuroOne Medical Technologies (of which 4 don't sit too well with us!) you should know about.

Of course NeuroOne Medical Technologies may not be the best stock to buy. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

If you're looking to trade NeuroOne Medical Technologies, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentValuation is complex, but we're here to simplify it.

Discover if NeuroOne Medical Technologies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:NMTC

NeuroOne Medical Technologies

A medical technology company, provides solutions for continuous electroencephalogram (cEEG) and stereoelectrocencephalography (sEEG) recording in the United States.

Flawless balance sheet slight.

Similar Companies

Market Insights

Community Narratives