- United States

- /

- Healthcare Services

- /

- NasdaqGM:CSTL

Castle Biosciences (CSTL): Assessing Valuation After Expert Consensus Endorses DecisionDx-Melanoma Test

Reviewed by Simply Wall St

A new expert consensus paper backing Castle Biosciences (CSTL) DecisionDx Melanoma test has pushed the stock higher, as investors weigh what wider physician adoption could mean for growth and valuation.

See our latest analysis for Castle Biosciences.

The expert backing for DecisionDx Melanoma comes on top of an already powerful move in the stock, with a roughly 69 percent three-month share price return and a nearly 50 percent one-year total shareholder return. This suggests momentum is building as investors re rate Castle Biosciences growth prospects and risk profile.

If this kind of evidence-driven re rating interests you, it may be worth exploring other innovative healthcare names using our screener for healthcare stocks as potential next ideas.

Yet with shares already near Wall Street targets but still implying a sizable intrinsic discount, is Castle Biosciences stock now a compelling entry point, or are investors simply paying up for growth that is already priced in?

Most Popular Narrative Narrative: 2.3% Overvalued

With Castle Biosciences last closing at 39.66 dollars against a most popular narrative fair value of 38.75 dollars, the story hinges on specific growth and margin assumptions that underpin this modest premium.

The analysts have a consensus price target of 35.625 for Castle Biosciences based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of 41.0, and the most bearish reporting a price target of just 30.0.

Curious why a steadily rising revenue base, a step change in profit margins, and a punchy future earnings multiple all converge on this fair value signal? The full narrative unpacks which growth engines must fire, how fast operating leverage needs to kick in, and what kind of premium valuation Castle would need to command for the current setup to make sense.

Result: Fair Value of $38.75 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, persistent reimbursement uncertainty for DecisionDx SCC and intensifying competition in molecular diagnostics could undermine margin expansion and the current growth narrative.

Find out about the key risks to this Castle Biosciences narrative.

Another View on Value

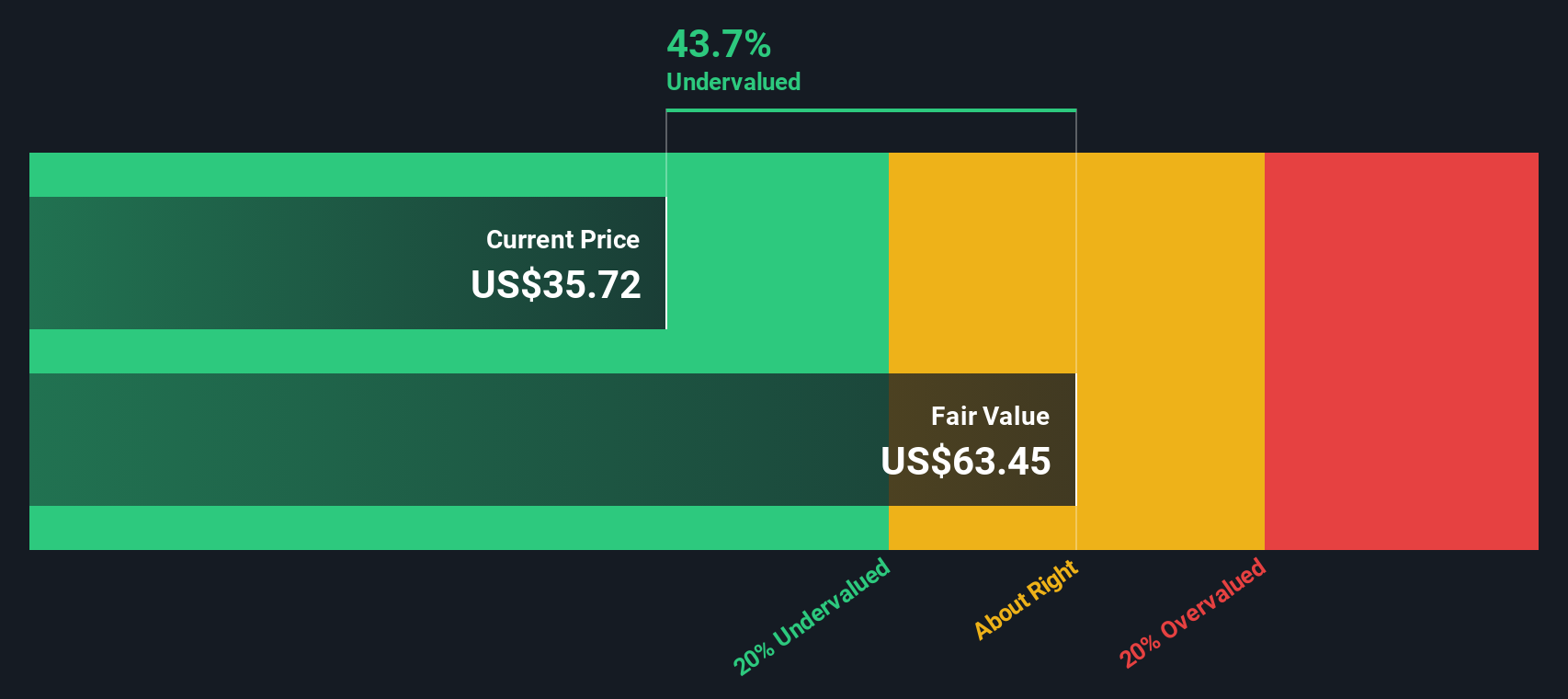

While the narrative framework suggests Castle Biosciences is about 2.3 percent overvalued, our DCF model paints a different picture, indicating the shares trade roughly 38.5 percent below fair value. If the cash flow math is closer to reality than the growth narrative, the market may be underestimating the long term upside.

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Castle Biosciences for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover 913 undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Castle Biosciences Narrative

If you see the story differently or want to stress test your own assumptions with the same data, you can build a personalized view in just a few minutes: Do it your way.

A great starting point for your Castle Biosciences research is our analysis highlighting 1 key reward and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Do not stop with one opportunity. Use Simply Wall Street's powerful screener tools to uncover more stocks that match your strategy before the crowd catches on.

- Capture potential mispricings early by scanning these 913 undervalued stocks based on cash flows that look attractive based on future cash flows and fundamentals.

- Tap into the next wave of innovation by targeting these 26 AI penny stocks positioned at the forefront of artificial intelligence advances.

- Build a resilient income stream by focusing on these 12 dividend stocks with yields > 3% that can support long term total returns.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGM:CSTL

Castle Biosciences

A molecular diagnostics company, provides test solutions for the diagnosis and treatment of dermatologic cancers, Barrett’s esophagus (BE), uveal melanoma, and mental health conditions.

Flawless balance sheet and slightly overvalued.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)