Advertisement

- United States

- /

- Medical Equipment

- /

- NasdaqGS:ALGN

Assessing Align Technology (ALGN) Valuation After Invisalign Mandibular Launch and 6% Share Price Jump

Simply Wall St

Reviewed by Simply Wall St

Align Technology (ALGN) just gave investors a fresh data point to chew on by rolling out its Invisalign System with mandibular advancement in the Philippines, and the stock quickly climbed about 6% on the news.

See our latest analysis for Align Technology.

The upbeat reaction to the Philippines launch sits against a tougher backdrop, with a roughly 9% one month share price return, but a year to date share price return still down about 28%, and a one year total shareholder return of around minus 36%, suggesting momentum is only just starting to rebuild as investors reassess growth and competitive risks.

If Align’s latest move has you thinking more broadly about healthcare opportunities, this could be a good moment to explore other healthcare stocks that are quietly reshaping patient care and investor expectations.

With shares still well below their highs but trading on improving sentiment, the real debate now is whether Align’s recent weakness leaves the stock undervalued or if today’s price already bakes in a healthier growth trajectory.

Most Popular Narrative Narrative: 16.4% Undervalued

With Align Technology last closing at $150.93 versus a narrative fair value near $180.50, the current gap sets up a compelling valuation story driven by medium term earnings power.

The continued expansion of clinical indications for Invisalign (such as Invisalign First for teens/kids and palate expanders) and the increasing adoption by general practitioner dentists are broadening Align's addressable market, positioning the company for higher long term revenues and double digit earnings growth as these new segments mature.

Curious how steady, not explosive, revenue growth could still justify a richer earnings multiple and rising margins over time, even as share count falls and cash flows are discounted at a measured rate? The most followed narrative stitches these moving parts together into one bold fair value target, but the exact growth runway, margin lift, and earnings bridge sit just out of sight. Want to see the full playbook behind that gap to intrinsic value and the assumptions it makes about Align’s next few years?

Result: Fair Value of $180.50 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, that upside case hinges on easing macro pressures and steadier orthodontic demand, both of which are vulnerable to weaker consumer confidence and shifting preferences back toward traditional braces.

Find out about the key risks to this Align Technology narrative.

Another Way to Look at Value

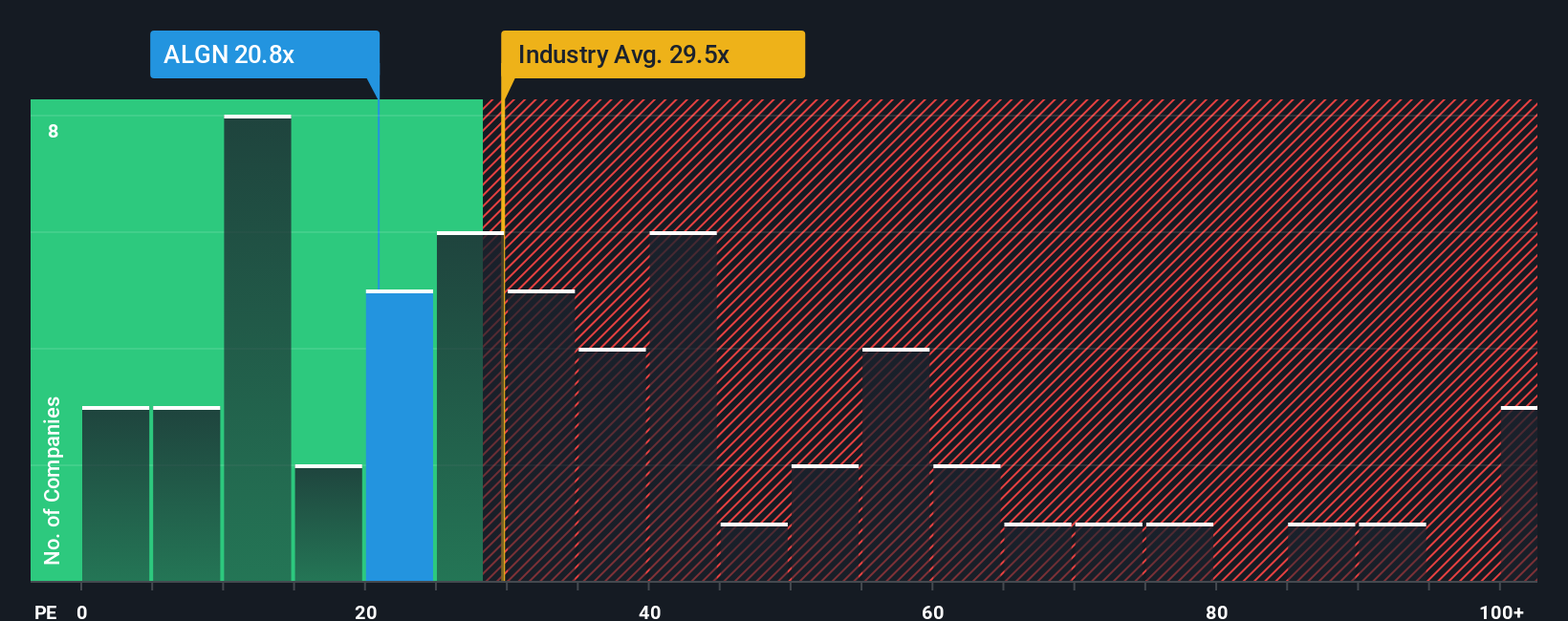

While the narrative suggests Align is about 16% undervalued, its 28.6 times price to earnings ratio actually sits slightly above both peer and industry averages, 27.9 times and 28.4 times, yet below a fair ratio of 30.5 times. This hints at only modest upside and real re rating risk if growth disappoints.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Align Technology Narrative

If you see the story differently or want to stress test the assumptions with your own inputs, you can build a fresh narrative in minutes: Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Align Technology.

Ready for your next investing move?

Before the market’s next swing leaves you on the sidelines, put your strategy to work with focused screeners that surface ideas aligned with your goals.

- Capture early stage momentum by scanning these 3576 penny stocks with strong financials that already show financial strength instead of chasing hype after prices have run.

- Position your portfolio at the forefront of intelligent automation with these 24 AI penny stocks that pair real business traction with AI powered growth potential.

- Identify value opportunities using these 927 undervalued stocks based on cash flows that trade below their cash flow based estimates before the broader market reacts.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:ALGN

Align Technology

Provides Invisalign clear aligners, Vivera retainers, and iTero intraoral scanners and services in the United States, Switzerland, and internationally.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

15 followersusers have followed this narrative

5 commentsusers have commented on this narrative

2 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MA

MarkoVT on Applied Digital ·

Staggered by dilution; positions for growth

Fair Value:US$35.4520.9% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

YE

Yellow_fever on China Starch Holdings ·

China Starch Holdings eyes a revenue growth of 4.66% with a 5-year strategic plan

Fair Value:HK$0.563.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on Power Solutions International ·

PSIX The timing of insider sales is a serious question mark

Fair Value:US$37.3845.7% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.5% undervalued

948 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.1% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative