- United States

- /

- Food

- /

- NasdaqCM:TWNK

Is Hostess Brands, Inc.'s (NASDAQ:TWNK) Stock Price Struggling As A Result Of Its Mixed Financials?

It is hard to get excited after looking at Hostess Brands' (NASDAQ:TWNK) recent performance, when its stock has declined 15% over the past three months. It is possible that the markets have ignored the company's differing financials and decided to lean-in to the negative sentiment. Long-term fundamentals are usually what drive market outcomes, so it's worth paying close attention. In this article, we decided to focus on Hostess Brands' ROE.

Return on Equity or ROE is a test of how effectively a company is growing its value and managing investors’ money. In other words, it is a profitability ratio which measures the rate of return on the capital provided by the company's shareholders.

See our latest analysis for Hostess Brands

How Do You Calculate Return On Equity?

ROE can be calculated by using the formula:

Return on Equity = Net Profit (from continuing operations) ÷ Shareholders' Equity

So, based on the above formula, the ROE for Hostess Brands is:

9.3% = US$168m ÷ US$1.8b (Based on the trailing twelve months to September 2022).

The 'return' is the profit over the last twelve months. That means that for every $1 worth of shareholders' equity, the company generated $0.09 in profit.

Why Is ROE Important For Earnings Growth?

So far, we've learned that ROE is a measure of a company's profitability. Depending on how much of these profits the company reinvests or "retains", and how effectively it does so, we are then able to assess a company’s earnings growth potential. Assuming all else is equal, companies that have both a higher return on equity and higher profit retention are usually the ones that have a higher growth rate when compared to companies that don't have the same features.

Hostess Brands' Earnings Growth And 9.3% ROE

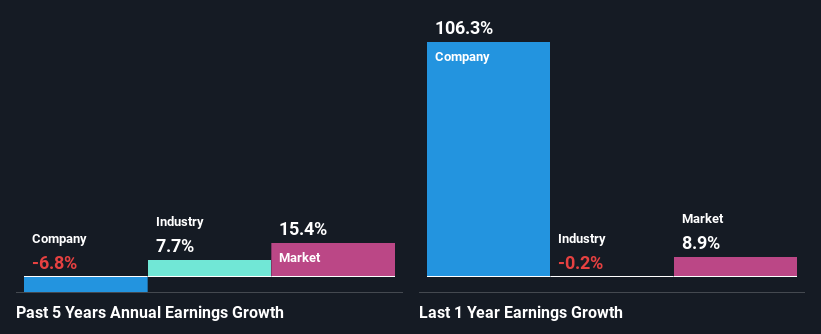

On the face of it, Hostess Brands' ROE is not much to talk about. Next, when compared to the average industry ROE of 14%, the company's ROE leaves us feeling even less enthusiastic. Given the circumstances, the significant decline in net income by 6.8% seen by Hostess Brands over the last five years is not surprising. We believe that there also might be other aspects that are negatively influencing the company's earnings prospects. Such as - low earnings retention or poor allocation of capital.

That being said, we compared Hostess Brands' performance with the industry and were concerned when we found that while the company has shrunk its earnings, the industry has grown its earnings at a rate of 7.7% in the same period.

The basis for attaching value to a company is, to a great extent, tied to its earnings growth. The investor should try to establish if the expected growth or decline in earnings, whichever the case may be, is priced in. By doing so, they will have an idea if the stock is headed into clear blue waters or if swampy waters await. What is TWNK worth today? The intrinsic value infographic in our free research report helps visualize whether TWNK is currently mispriced by the market.

Is Hostess Brands Efficiently Re-investing Its Profits?

Hostess Brands doesn't pay any dividend, meaning that the company is keeping all of its profits, which makes us wonder why it is retaining its earnings if it can't use them to grow its business. So there might be other factors at play here which could potentially be hampering growth. For example, the business has faced some headwinds.

Summary

In total, we're a bit ambivalent about Hostess Brands' performance. Even though it appears to be retaining most of its profits, given the low ROE, investors may not be benefitting from all that reinvestment after all. The low earnings growth suggests our theory correct. With that said, we studied current analyst estimates and discovered that analysts expect the company's earnings growth to improve slightly. This could offer some relief to the company's existing shareholders. Are these analysts expectations based on the broad expectations for the industry, or on the company's fundamentals? Click here to be taken to our analyst's forecasts page for the company.

Valuation is complex, but we're here to simplify it.

Discover if Hostess Brands might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqCM:TWNK

Hostess Brands

Hostess Brands, Inc. develops, manufactures, markets, sells, and distributes snack products in the United States and Canada.

Adequate balance sheet and slightly overvalued.