Advertisement

- United States

- /

- Beverage

- /

- NasdaqGS:PEP

Institutional owners may consider drastic measures as PepsiCo, Inc.'s (NASDAQ:PEP) recent US$9.7b drop adds to long-term losses

Key Insights

- Given the large stake in the stock by institutions, PepsiCo's stock price might be vulnerable to their trading decisions

- A total of 25 investors have a majority stake in the company with 42% ownership

- Using data from analyst forecasts alongside ownership research, one can better assess the future performance of a company

To get a sense of who is truly in control of PepsiCo, Inc. (NASDAQ:PEP), it is important to understand the ownership structure of the business. We can see that institutions own the lion's share in the company with 75% ownership. That is, the group stands to benefit the most if the stock rises (or lose the most if there is a downturn).

And so it follows that institutional investors was the group most impacted after the company's market cap fell to US$198b last week after a 4.7% drop in the share price. The recent loss, which adds to a one-year loss of 12% for stockholders, may not sit well with this group of investors. Often called “market movers", institutions wield significant power in influencing the price dynamics of any stock. As a result, if the downtrend continues, institutions may face pressures to sell PepsiCo, which might have negative implications on individual investors.

Let's delve deeper into each type of owner of PepsiCo, beginning with the chart below.

Check out our latest analysis for PepsiCo

What Does The Institutional Ownership Tell Us About PepsiCo?

Institutional investors commonly compare their own returns to the returns of a commonly followed index. So they generally do consider buying larger companies that are included in the relevant benchmark index.

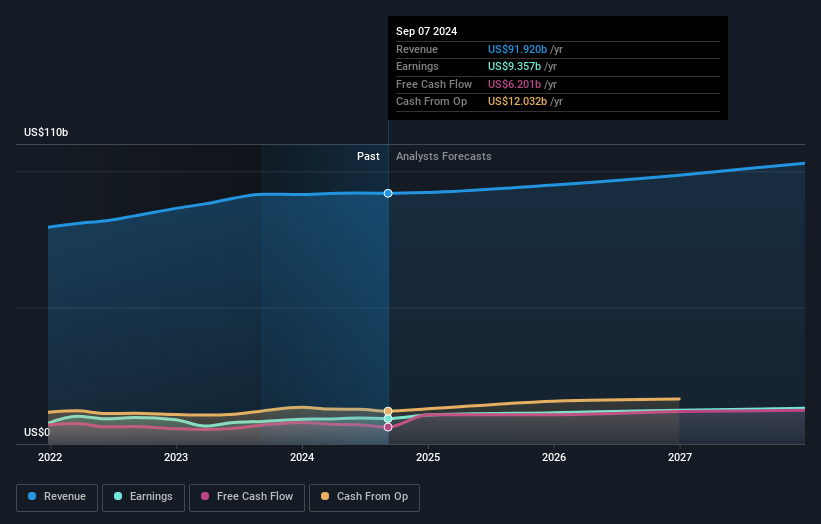

We can see that PepsiCo does have institutional investors; and they hold a good portion of the company's stock. This implies the analysts working for those institutions have looked at the stock and they like it. But just like anyone else, they could be wrong. It is not uncommon to see a big share price drop if two large institutional investors try to sell out of a stock at the same time. So it is worth checking the past earnings trajectory of PepsiCo, (below). Of course, keep in mind that there are other factors to consider, too.

Investors should note that institutions actually own more than half the company, so they can collectively wield significant power. We note that hedge funds don't have a meaningful investment in PepsiCo. Our data shows that The Vanguard Group, Inc. is the largest shareholder with 9.5% of shares outstanding. In comparison, the second and third largest shareholders hold about 7.9% and 4.1% of the stock.

Our studies suggest that the top 25 shareholders collectively control less than half of the company's shares, meaning that the company's shares are widely disseminated and there is no dominant shareholder.

Researching institutional ownership is a good way to gauge and filter a stock's expected performance. The same can be achieved by studying analyst sentiments. Quite a few analysts cover the stock, so you could look into forecast growth quite easily.

Insider Ownership Of PepsiCo

While the precise definition of an insider can be subjective, almost everyone considers board members to be insiders. Management ultimately answers to the board. However, it is not uncommon for managers to be executive board members, especially if they are a founder or the CEO.

I generally consider insider ownership to be a good thing. However, on some occasions it makes it more difficult for other shareholders to hold the board accountable for decisions.

Our most recent data indicates that insiders own less than 1% of PepsiCo, Inc.. Being so large, we would not expect insiders to own a large proportion of the stock. Collectively, they own US$265m of stock. In this sort of situation, it can be more interesting to see if those insiders have been buying or selling.

General Public Ownership

The general public-- including retail investors -- own 25% stake in the company, and hence can't easily be ignored. While this group can't necessarily call the shots, it can certainly have a real influence on how the company is run.

Next Steps:

While it is well worth considering the different groups that own a company, there are other factors that are even more important. Case in point: We've spotted 2 warning signs for PepsiCo you should be aware of.

Ultimately the future is most important. You can access this free report on analyst forecasts for the company.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:PEP

PepsiCo

Engages in the manufacture, marketing, distribution, and sale of various beverages and convenient foods worldwide.

Good value with proven track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.5% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|18.7% undervalued

TI

Community Contributor