Advertisement

- United States

- /

- Beverage

- /

- NasdaqGS:KDP

Should KDP Investors Reconsider Strategies After Raised 2025 Outlook and Pending Company Split?

Simply Wall St

Reviewed by Sasha Jovanovic

- Keurig Dr Pepper recently reported third-quarter sales of US$4.31 billion and net income of US$662 million, alongside announcing progress on its acquisition of JDE Peet’s and preparations to split into two independent companies by the end of 2026.

- The company raised its guidance for 2025, now expecting constant currency net sales to grow in the high-single-digit range, highlighting management’s positive outlook and the ongoing restructuring of its leadership and operating structure.

- We'll assess how the raised 2025 guidance and upcoming company separation could influence Keurig Dr Pepper's investment narrative.

Explore 28 top quantum computing companies leading the revolution in next-gen technology and shaping the future with breakthroughs in quantum algorithms, superconducting qubits, and cutting-edge research.

Keurig Dr Pepper Investment Narrative Recap

To be a shareholder in Keurig Dr Pepper, you need to be confident in the company’s ability to grow its beverage and coffee brands while managing operational complexity, especially as it moves toward splitting into two independent entities. The latest update on acquisition progress and leadership restructuring supports the company's push for higher 2025 sales growth, but does not materially alter the immediate focus on stabilizing US Coffee segment performance or addressing inflationary cost risks.

Among recent announcements, the revised 2025 guidance to high-single-digit net sales growth stands out, signaling greater confidence from management even as the company prepares for a significant organizational split. As the company sets its sights on separating Global Coffee Co. and Beverage Co., the ability to maintain margin stability, particularly in the face of persistent commodity inflation and tariff pressures, will be closely watched as a key catalyst for the stock.

On the other hand, investors should be aware that unresolved cost headwinds in the coffee segment could become more challenging if inflation persists and...

Read the full narrative on Keurig Dr Pepper (it's free!)

Keurig Dr Pepper's narrative projects $24.1 billion in revenue and $3.6 billion in earnings by 2028. This requires a 15.2% yearly revenue growth and a $2.1 billion earnings increase from current earnings of $1.5 billion.

Uncover how Keurig Dr Pepper's forecasts yield a $34.06 fair value, a 25% upside to its current price.

Exploring Other Perspectives

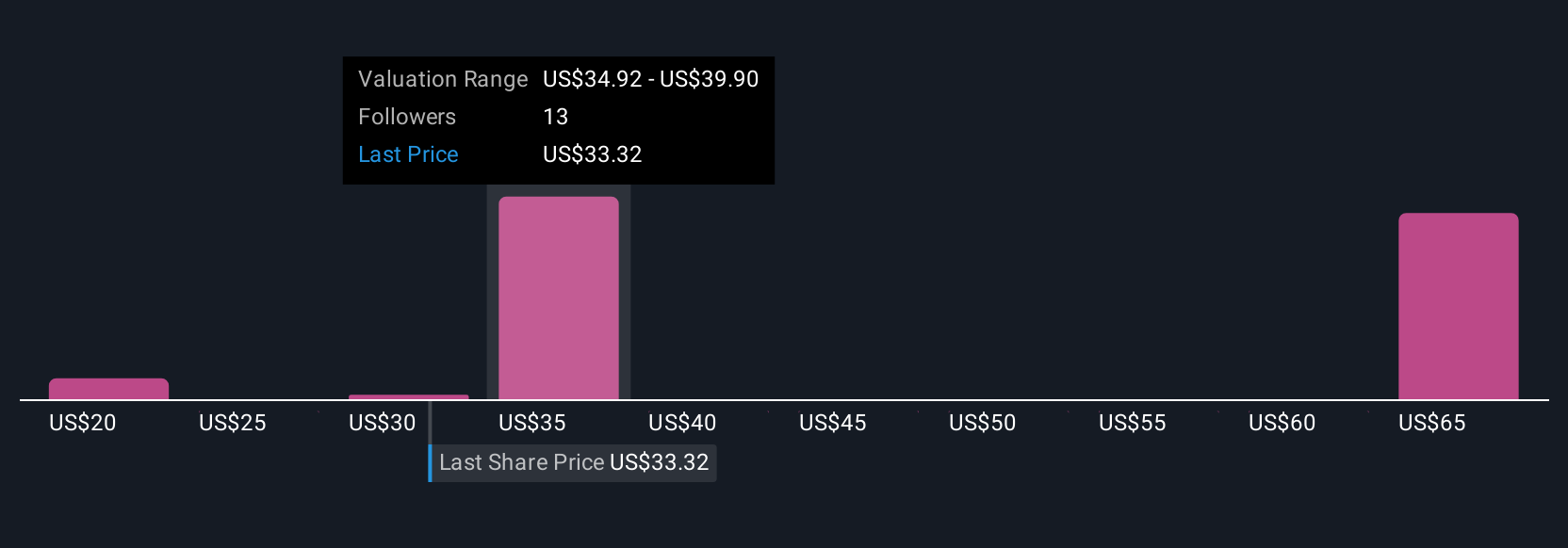

Simply Wall St Community members estimate Keurig Dr Pepper’s fair value between US$22.62 and US$64.96, reflecting eight distinct viewpoints. With continued inflationary pressure in coffee, you may want to compare these opinions before deciding which performance drivers matter most for your outlook.

Explore 8 other fair value estimates on Keurig Dr Pepper - why the stock might be worth 17% less than the current price!

Build Your Own Keurig Dr Pepper Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Keurig Dr Pepper research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Keurig Dr Pepper research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Keurig Dr Pepper's overall financial health at a glance.

Curious About Other Options?

Our top stock finds are flying under the radar-for now. Get in early:

- Find companies with promising cash flow potential yet trading below their fair value.

- AI is about to change healthcare. These 33 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The end of cancer? These 27 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Keurig Dr Pepper might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:KDP

Keurig Dr Pepper

Owns, manufactures, and distributors beverages and single serve brewing systems in the United States and internationally.

Undervalued with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor