Advertisement

- United States

- /

- Food

- /

- NasdaqGS:CPB

Does Expected Q1 Margin Pressure From Tariffs And Marketing Reframe Campbell's (CPB) At‑Home Demand Story?

Simply Wall St

Reviewed by Sasha Jovanovic

- Campbell's is set to report its first-quarter fiscal 2026 earnings on 9 December 2025, with analysts expecting pressure on revenue and margins from tariffs and higher marketing expenses, alongside softness in the Snacks segment.

- Despite these headwinds, analysts highlight Campbell's consistent record of exceeding earnings estimates and continued support from at-home cooking trends bolstering its Meals & Beverages division.

- We’ll now examine how expectations for margin pressure from tariffs and marketing spend may influence Campbell's broader investment narrative.

We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Campbell's Investment Narrative Recap

To own Campbell’s, you need to believe its core pantry brands can offset slow category growth and cost pressure from tariffs and marketing. The latest earnings expectations mainly reinforce the key near term catalyst, which is whether Meals & Beverages can keep leveraging at home cooking demand, while the biggest current risk remains sustained margin compression from tariffs on aluminum and imported ingredients.

Among recent announcements, the appointment of Todd Cunfer as CFO in October 2025 stands out in this context, as investors weigh how new financial leadership might respond to tariff driven cost pressure and higher marketing spend. How effectively capital allocation, cost control and brand support are balanced from here will help shape whether Campbell’s can preserve earnings quality despite softer Snacks performance.

Yet behind the comfort of resilient soup demand, investors should be aware of how exposed Campbell’s margins are to prolonged tariff pressure on...

Read the full narrative on Campbell's (it's free!)

Campbell's narrative projects $10.2 billion revenue and $868.6 million earnings by 2028. This requires a 0.0% yearly revenue decline and about a $266.6 million earnings increase from $602.0 million today.

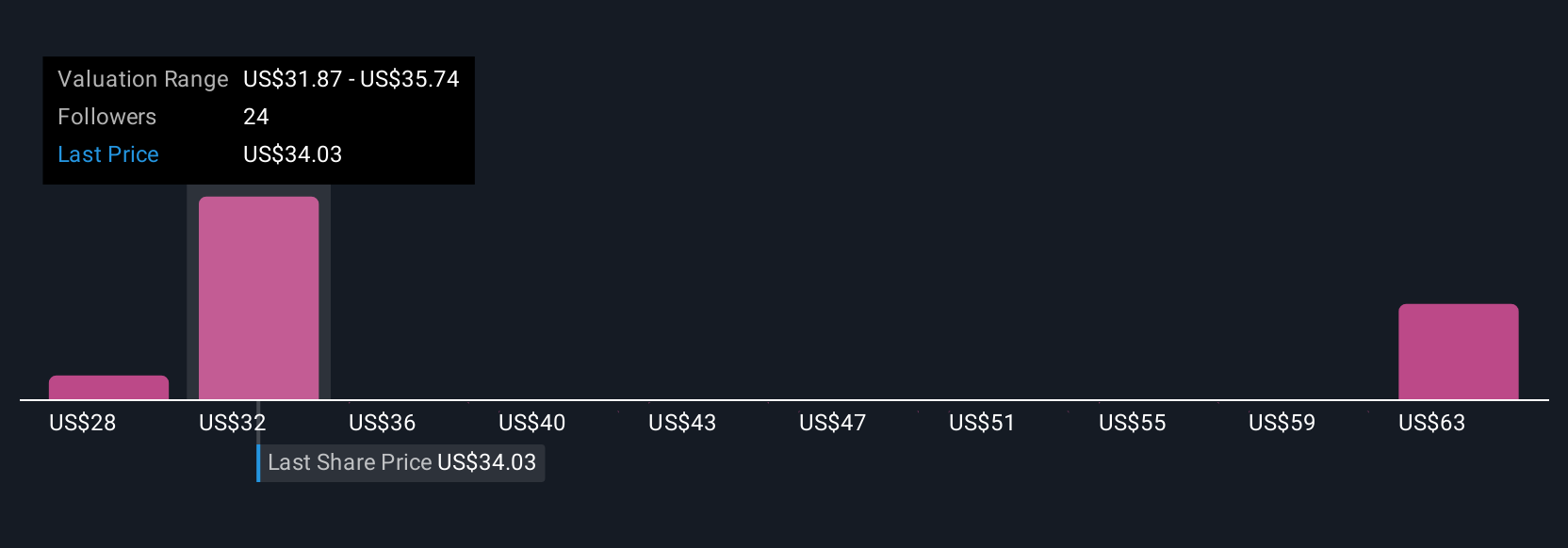

Uncover how Campbell's forecasts yield a $33.84 fair value, a 14% upside to its current price.

Exploring Other Perspectives

Five members of the Simply Wall St Community value Campbell’s between US$29 and about US$63, underscoring how far apart individual views on upside potential really are. You might weigh those alongside current concerns that tariffs on aluminum and imported ingredients could lock in a lower profit base and shape Campbell’s performance over the next few years.

Explore 5 other fair value estimates on Campbell's - why the stock might be worth over 2x more than the current price!

Build Your Own Campbell's Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Campbell's research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Campbell's research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Campbell's overall financial health at a glance.

Contemplating Other Strategies?

Markets shift fast. These stocks won't stay hidden for long. Get the list while it matters:

- Trump's oil boom is here - pipelines are primed to profit. Discover the 22 US stocks riding the wave.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:CPB

Campbell's

Manufactures and markets food and beverage products in the United States and internationally.

6 star dividend payer and good value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

65 followersusers have followed this narrative

7 commentsusers have commented on this narrative

19 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

11 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Magma Silver ·

Silver's Breakout to over $50US will make Magma’s future shine with drill sampling returning 115g/t Silver and 2.3 g/t Gold at its Peru Mine

Fair Value:CA$0.3534.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on SEGRO ·

SEGRO's Revenue to Rise 14.7% Amidst Optimistic Growth Plans

Fair Value:UK£9.3924.7% undervalued

0 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

PI

PicaCoder on Microsoft ·

After the AI Party: A Sobering Look at Microsoft's Future

Fair Value:US$42015.0% overvalued

62 followersusers have followed this narrative

12 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

958 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

65 followersusers have followed this narrative

7 commentsusers have commented on this narrative

19 likesusers have liked this narrative