Advertisement

- United States

- /

- Energy Services

- /

- NYSE:WTTR

How Does Select Water Solutions Stack Up After Recent 11% Price Surge?

Reviewed by Bailey Pemberton

If you are wondering what to do with Select Water Solutions stock right now, you are not alone. Investors have been keeping a close eye on this name, especially after its recent rollercoaster ride in the market. In just the last 30 days, Select Water Solutions popped up 11.1%, but that came after a tough 7-day stretch that saw the price dip by 8.8%. Over the longer term, the stock tells an interesting story. Year-to-date, it is down a sizable 28.6%. Zoom out and you will see that over the past five years, the return is an eye-popping 194.4%. That kind of performance is bound to catch attention, especially against a backdrop of evolving market demand for water infrastructure and services, and broader commentary on energy sector supply chains.

Despite some recent downside, this is a company that still has growth potential, and the way investors perceive risk seems to be shifting. Perhaps that is why, according to six widely followed valuation checks, Select Water Solutions scores a 2 out of 6 for being undervalued. This means it passed two different measures where value seems to be on your side, but there are several areas that still raise questions.

Now, let us get right into how these valuation methods stack up and what they reveal about where Select Water Solutions stands today. Later on, I will share a perspective that goes beyond the checkboxes to give you the bigger picture on how to really judge this stock's worth.

Select Water Solutions scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Select Water Solutions Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model works by forecasting a company’s expected future cash flows and then discounting them back to the present to estimate what the business is fundamentally worth today. For Select Water Solutions, this method projects how the company’s ability to generate cash may evolve over the coming years.

Currently, Select Water Solutions reports a Free Cash Flow (FCF) of approximately $43.4 Million. Analyst estimates suggest strong growth ahead, with annual FCF expected to reach over $73.5 Million by 2026 and potentially up to $128.7 Million by 2035, according to extended projections. While analyst coverage generally spans up to five years, figures further into the future are extrapolated based on company and industry trends.

Running these cash flow projections through the DCF model yields an estimated intrinsic value of $16.96 per share. Compared to the current market price, this analysis points to the stock trading at a 42.1% discount, suggesting that Select Water Solutions is significantly undervalued at this time.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Select Water Solutions is undervalued by 42.1%. Track this in your watchlist or portfolio, or discover more undervalued stocks.

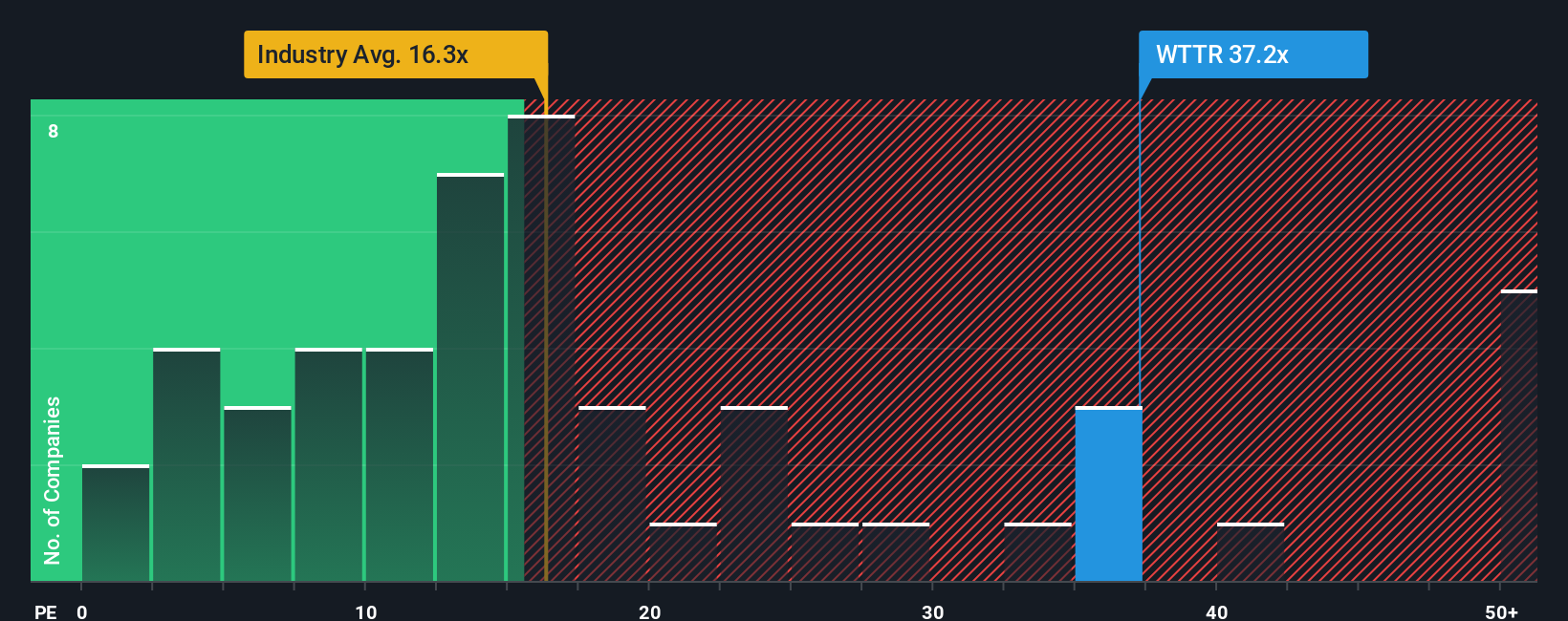

Approach 2: Select Water Solutions Price vs Earnings (PE)

The Price-to-Earnings (PE) ratio is a favored metric for valuing established, profitable companies like Select Water Solutions, because it gives a direct snapshot of what investors are willing to pay for each dollar of current earnings. It is widely used for quickly comparing how the market prices one company versus another on an earnings basis.

What counts as a "fair" PE ratio, though, is shaped by factors such as growth outlook and perceived risk. Companies expected to deliver faster earnings growth or viewed as less risky often justify higher PE ratios, while riskier or slow-growth businesses tend to see lower ones.

Right now, Select Water Solutions trades at a PE ratio of 31x. To put this in perspective, the average PE for peers is just 4.83x and the broader Energy Services industry average sits at 13.97x. This suggests the market is already assigning a significant earnings premium to Select Water Solutions compared to its competitors and sector.

Instead of relying solely on peer or industry comparisons, the Simply Wall St “Fair Ratio” goes further. It customizes the benchmark PE for Select Water Solutions by factoring in this company’s own earnings growth, profit margins, size, sector, and specific risks. For Select Water Solutions, the Fair Ratio is 19.53x, which is above the industry average but below the company’s current multiple. This more nuanced view provides a better anchor for valuation, as it adapts to real differences in company profiles and future prospects.

Comparing the current PE of 31x to the Fair Ratio of 19.53x, Select Water Solutions is trading above what would be considered justified based on its fundamental characteristics. This points to the shares being overvalued on this metric at present.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Select Water Solutions Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives. A Narrative is simply the story you tell about a company: your view of its future, using your own expectations for revenue growth, profit margins, and what the business is truly worth. By linking your perspective directly to a financial forecast and a fair value estimate, Narratives transform valuation from a static number into something dynamic and meaningful to you.

Rather than relying solely on ratios or analyst opinions, Narratives empower you to clearly lay out your assumptions and see how your reasoning leads to a specific fair value for Select Water Solutions. This powerful tool is accessible right now in the Community section on Simply Wall St, where millions of investors share and update Narratives in real time as new information or earnings emerge. Narratives make it easier to spot when your fair value diverges from the current market price, helping you decide if now is the right time to buy or sell.

For instance, some investors see resilient water infrastructure contracts and advanced recycling driving a fair value of $18.00 per share, while others, weighing sector risks and cost pressures, arrive at $10.00. Your unique Narrative can be just as valid and actionable as theirs.

Do you think there's more to the story for Select Water Solutions? Create your own Narrative to let the Community know!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WTTR

Select Water Solutions

Provides water management solutions to the energy industry in the United States.

Adequate balance sheet with slight risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

LO

Lou_Basenese on Virtuix Holdings ·

From a “Shark Tank” Snub to an Air Force “Yes”: Why Virtuix at $3.50 May Be the Market’s Most Mispriced AI Story

Fair Value:US$7.559.3% undervalued

33 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

HE

HedgeY on IonQ ·

The Best-Funded Quantum Platform and Still a Stock Priced for Perfection

Fair Value:US$4811.0% overvalued

14 followersusers have followed this narrative

0 commentsusers have commented on this narrative

2 likesusers have liked this narrative

BL

BlackGoat on Cerebras Systems ·

The Wafer Giant Threatening NVIDIA's GPU Hegemony

Fair Value:US$415.5446.8% undervalued

23 followersusers have followed this narrative

1 commentusers have commented on this narrative

6 likesusers have liked this narrative

IV

Ivoed on Netflix ·

Netflix’s Business Quality Is Clear. The Harder Question Is Whether The Stock Is Still Cheap

Fair Value:US$8212.9% undervalued

18 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

Recently Updated Narratives

AS

AstrisCorporateAdvisory on MIRAI ·

Improving NOI growth visibility on wider rent gap

Fair Value:JP¥77.06k45.8% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AN

andre_santos on NIKE ·

Nike - A Fundamental and Historical Valuation

Fair Value:US$36.8311.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TR

TripleS on AnaptysBio ·

ANAB has a scaling and rising royalty stream, one up and coming new royalty, a loan that dies in 2027 which will result in a doubling

Fair Value:US$9025.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

IN

Investingwilly on Mastercard ·

Mastercard: The Best Dividend Stock You're Ignoring

Fair Value:US$75031.5% undervalued

79 followersusers have followed this narrative

1 commentusers have commented on this narrative

9 likesusers have liked this narrative

HA

HarishPK on Adobe ·

Adobe: A Probabilistic Case for Undervaluation

Fair Value:US$319.9635.9% undervalued

62 followersusers have followed this narrative

9 commentsusers have commented on this narrative

19 likesusers have liked this narrative

MA

martinarauz on Nu Holdings ·

Investment Analysis (May 2026)

Fair Value:US$22.7441.2% undervalued

68 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative