Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:WMB

The Compensation For The Williams Companies, Inc.'s (NYSE:WMB) CEO Looks Deserved And Here's Why

Key Insights

- Williams Companies' Annual General Meeting to take place on 30th of April

- Salary of US$1.39m is part of CEO Murray Armstrong's total remuneration

- The total compensation is similar to the average for the industry

- Williams Companies' total shareholder return over the past three years was 87% while its EPS grew by 150% over the past three years

We have been pretty impressed with the performance at The Williams Companies, Inc. (NYSE:WMB) recently and CEO Murray Armstrong deserves a mention for their role in it. The pleasing results would be something shareholders would keep in mind at the upcoming AGM on 30th of April. It is likely that the focus will be on company strategy going forward as shareholders hear from the board and cast their votes on resolutions such as executive remuneration and other matters. We think the CEO has done a pretty decent job and we discuss why the CEO compensation is appropriate.

View our latest analysis for Williams Companies

How Does Total Compensation For Murray Armstrong Compare With Other Companies In The Industry?

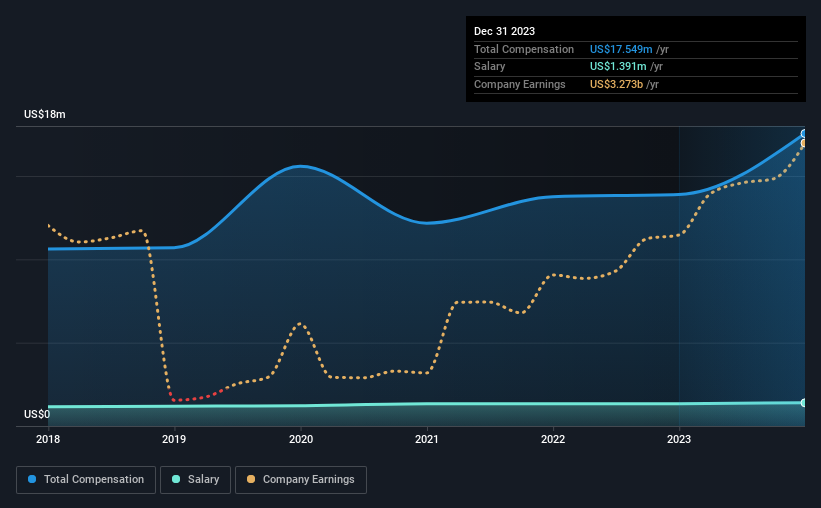

According to our data, The Williams Companies, Inc. has a market capitalization of US$47b, and paid its CEO total annual compensation worth US$18m over the year to December 2023. That's a notable increase of 26% on last year. We think total compensation is more important but our data shows that the CEO salary is lower, at US$1.4m.

For comparison, other companies in the American Oil and Gas industry with market capitalizations above US$8.0b, reported a median total CEO compensation of US$15m. This suggests that Williams Companies remunerates its CEO largely in line with the industry average. What's more, Murray Armstrong holds US$94m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | US$1.4m | US$1.3m | 8% |

| Other | US$16m | US$13m | 92% |

| Total Compensation | US$18m | US$14m | 100% |

On an industry level, around 13% of total compensation represents salary and 87% is other remuneration. Williams Companies sets aside a smaller share of compensation for salary, in comparison to the overall industry. If non-salary compensation dominates total pay, it's an indicator that the executive's salary is tied to company performance.

A Look at The Williams Companies, Inc.'s Growth Numbers

The Williams Companies, Inc.'s earnings per share (EPS) grew 150% per year over the last three years. In the last year, its revenue is down 12%.

Overall this is a positive result for shareholders, showing that the company has improved in recent years. While it would be good to see revenue growth, profits matter more in the end. Looking ahead, you might want to check this free visual report on analyst forecasts for the company's future earnings..

Has The Williams Companies, Inc. Been A Good Investment?

Most shareholders would probably be pleased with The Williams Companies, Inc. for providing a total return of 87% over three years. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

In Summary...

The company's solid performance might have made most shareholders happy, possibly making CEO remuneration the least of the matters to be discussed in the AGM. However, investors will get the chance to engage on key strategic initiatives and future growth opportunities for the company and set their longer-term expectations.

CEO pay is simply one of the many factors that need to be considered while examining business performance. We identified 2 warning signs for Williams Companies (1 shouldn't be ignored!) that you should be aware of before investing here.

Of course, you might find a fantastic investment by looking at a different set of stocks. So take a peek at this free list of interesting companies.

Valuation is complex, but we're here to simplify it.

Discover if Williams Companies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:WMB

Williams Companies

Operates as an energy infrastructure company primarily in the United States.

Slight with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Most Undervalued of the Magnificent 7

Fair Value US$237.43|36.3% undervalued

IN

Community Contributor

PVA TePla's New Strategy Aims for 22% Revenue Growth in Semiconductor Recovery

Fair Value €19.19|20.8% undervalued

MI

Community Contributor