Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:WMB

A fresh look at Williams Companies (WMB) valuation after new $250 million credit agreement announcement

Simply Wall St

Reviewed by Simply Wall St

Williams Companies (WMB) just lined up a new $250 million credit agreement through its Northwest Pipeline unit, giving it fresh flexibility to refinance debt, fund projects, and keep growth plans moving without stressing the balance sheet.

See our latest analysis for Williams Companies.

That extra liquidity is landing at a time when sentiment is already positive, with a roughly 10 percent year to date share price return and a three year total shareholder return above 100 percent suggesting momentum is still building rather than fading.

If this kind of steady infrastructure story appeals to you, it might be worth seeing what else is working in the space by exploring fast growing stocks with high insider ownership.

With earnings still growing, a solid value score, and shares trading at a discount to analyst and intrinsic estimates, are investors overlooking further upside here, or has the market already priced in Williams’s next leg of growth?

Most Popular Narrative Narrative: 9.1% Undervalued

With Williams Companies last closing at $61.55 against a narrative fair value near the high 60s, the story leans toward upside backed by ambitious growth assumptions.

The company’s robust, fully contracted project backlog (extending beyond 2030), disciplined layering of short and long-cycle projects, and committed capital plan are driving upward revisions to EBITDA and AFFO guidance, indicating future earnings and dividend visibility that may not be fully reflected in current valuation.

Curious how long dated contracts, rising margins, and a richer future earnings multiple all combine into that higher fair value estimate? The full narrative unpacks the precise growth runway, the profitability reset, and the valuation leap it assumes, step by step.

Result: Fair Value of $67.70 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, faster decarbonization policies or renewed permitting setbacks on marquee projects could curb throughput growth and challenge the premium multiple embedded in today’s narrative.

Find out about the key risks to this Williams Companies narrative.

Another Angle on Valuation

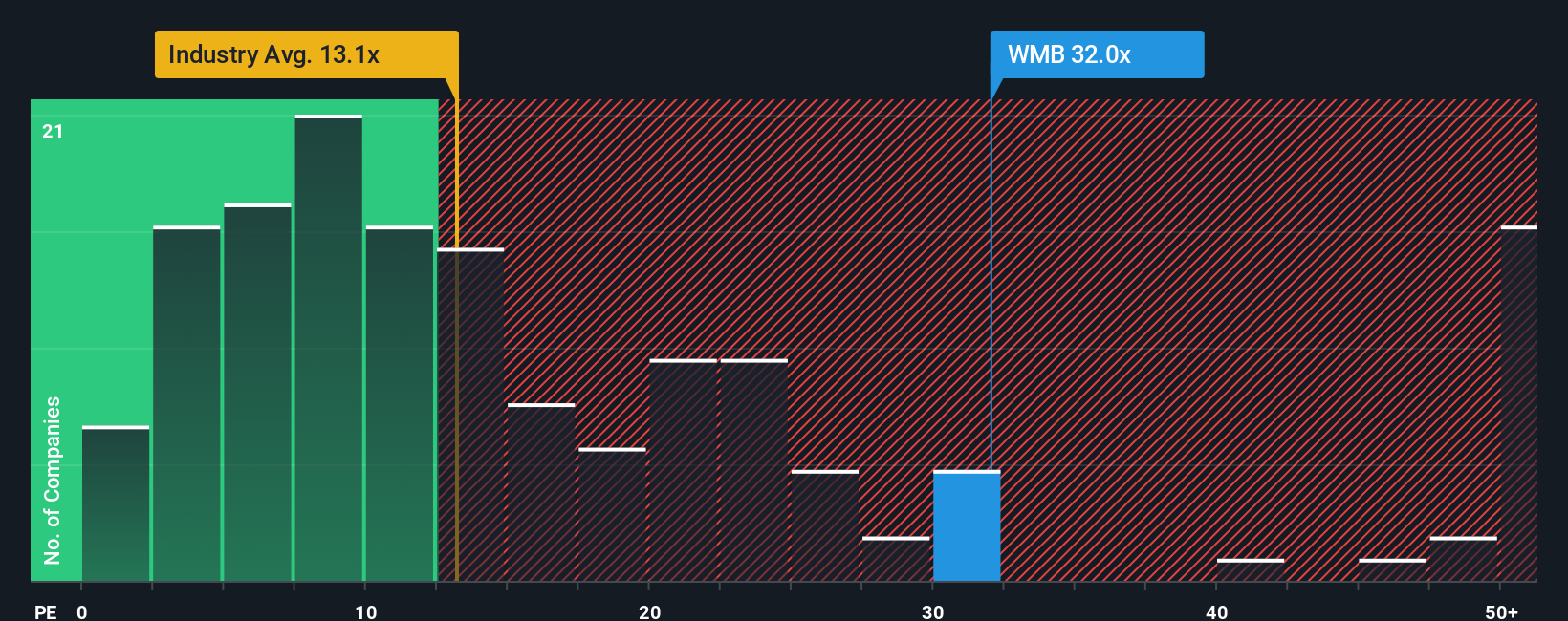

While the narrative and our fair value work suggest upside, the earnings multiple tells a more cautious story. Williams trades on a 31.8x price to earnings ratio versus 13.6x for the US Oil and Gas industry, 14.8x for peers, and a 23.1x fair ratio, implying investors are already paying a steep premium. How comfortable are you betting that growth, execution, and sentiment will keep supporting that gap?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Williams Companies Narrative

If this perspective does not quite match your own, or you prefer digging into the numbers yourself, you can build a personalized view in minutes: Do it your way.

A great starting point for your Williams Companies research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, lock in your next opportunity by using the Simply Wall St screener to surface focused, high conviction ideas tailored to your strategy.

- Capture potential rebound plays with these 3571 penny stocks with strong financials that already show the financial strength many bargain hunters overlook.

- Position yourself ahead of the next tech shift by targeting these 25 AI penny stocks that are building real businesses around artificial intelligence, not just hype.

- Secure more value for every dollar by zeroing in on these 915 undervalued stocks based on cash flows that our cash flow models flag as mispriced by the market.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Williams Companies might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:WMB

Williams Companies

Operates as an energy infrastructure company primarily in the United States.

Limited growth with questionable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

39 followersusers have followed this narrative

6 commentsusers have commented on this narrative

11 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1918.1% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5190.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

114 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

952 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative