Advertisement

- United States

- /

- Energy Services

- /

- NYSE:VAL

Valaris (VAL) Valuation Check After New Offshore Drilling Contracts and Strengthening Contract Backlog

Simply Wall St

Reviewed by Simply Wall St

Valaris (VAL) has been back in the spotlight after securing fresh offshore drilling contracts, a move that tightens its backlog and reinforces its role as a geared play on the offshore recovery.

See our latest analysis for Valaris.

The new contracts arrive as momentum builds, with the share price up 32.5% year to date and a 41.97% one year total shareholder return signaling that investors are increasingly pricing in a stronger offshore cycle.

If this offshore rebound has caught your attention, it could be a good moment to broaden your search and discover aerospace and defense stocks as another corner of the market with cyclical exposure and contract driven growth stories.

Yet with shares rallying ahead of fundamentals and trading at a premium to analyst targets, is Valaris still an underappreciated offshore recovery play or has the market already priced in the next leg of growth?

Most Popular Narrative: 8.2% Overvalued

With Valaris last closing at $59.60 against a narrative fair value of $55.10, the current price leans ahead of projected fundamentals.

The analysts have a consensus price target of $52.1 for Valaris based on their expectations of its future earnings growth, profit margins and other risk factors. However, there is a degree of disagreement amongst analysts, with the most bullish reporting a price target of $62.0, and the most bearish reporting a price target of just $38.0.

Curious what kind of earnings ramp and margin reset could justify that gap between bullish and bearish views? The narrative leans on a specific profit trajectory and a future valuation multiple that quietly reshapes today’s price debate. Want to see the full set of assumptions driving that fair value line in the sand?

Result: Fair Value of $55.10 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, faster than expected energy transition or a bout of offshore overcapacity could pressure day rates and margins, undermining the current bullish narrative.

Find out about the key risks to this Valaris narrative.

Another Lens on Valuation

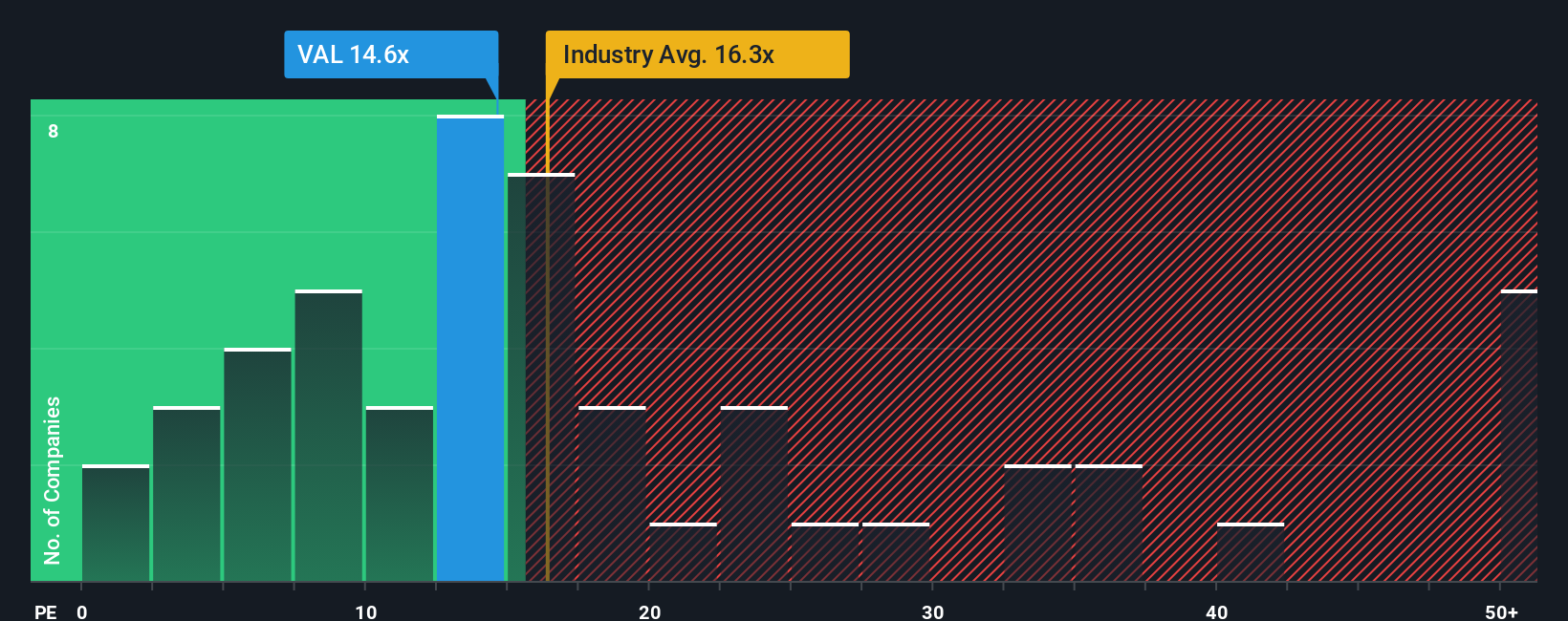

Analysts may call Valaris 8.2% overvalued on narrative fair value, but our earnings based check points the other way. At 10.4x earnings versus an industry 17.6x and a fair ratio of 15.8x, the current price looks discounted. Is sentiment lagging the fundamentals?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Valaris Narrative

If you see the story differently or want to stress test the assumptions yourself, you can build a personalized view in just minutes: Do it your way.

A great starting point for your Valaris research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Ready for your next move?

Before you stop at Valaris, give yourself an edge by scanning other high potential ideas on Simply Wall Street so you are not leaving returns on the table.

- Capture potential multi baggers early by scanning these 3577 penny stocks with strong financials that already pair tiny market caps with balance sheet strength and improving fundamentals.

- Position ahead of the next wave of innovation by targeting these 26 AI penny stocks that fuse cutting edge technology with scalable business models.

- Lock in quality at sensible prices by screening these 908 undervalued stocks based on cash flows where discounted cash flows point to meaningful upside versus current market expectations.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:VAL

Valaris

Provides offshore contract drilling services in Brazil, the United Kingdom, U.S.

Undervalued with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$247.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4729.5% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$482.8% undervalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6410.8% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

AN

AnalystConsensusTarget on Alphabet ·

GOOGL: AI Platform Expansion And Cloud Demand Will Support Durable Performance Amid Competitive Pressures

Fair Value:US$323.70.8% undervalued

1342 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative