Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:TRGP

Did Targa Resources’ (TRGP) $1.6 Billion Permian Expansion Just Shift Its Long-Term Investment Narrative?

Simply Wall St

Reviewed by Sasha Jovanovic

- In late September 2025, Targa Resources Corp. announced a major expansion in the Permian Basin, including the construction of the Speedway NGL Pipeline and the Yeti gas processing plant, representing a commitment of approximately US$1.6 billion to connect growing NGL and natural gas volumes to its key Mont Belvieu hub.

- This expansion underscores Targa’s intent to support rising production and capitalize on increased infrastructure demand, with five new gas processing plants coming online in the next two years and a pipeline expandable to 1 million barrels per day.

- We'll explore how Targa's large-scale pipeline project could influence its long-term growth prospects and impact its investment outlook.

The end of cancer? These 28 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

Targa Resources Investment Narrative Recap

If you’re considering Targa Resources as an investment, the core belief is in sustained growth for NGL and natural gas volumes in the Permian, and Targa’s ability to capture this rising demand through infrastructure scale. The recent Speedway pipeline and new plants are designed to support these trends; however, their near-term impact on key catalysts and top risks, especially industry overbuild and margin compression, appears incremental rather than transformative at this stage.

Among recent developments, the Speedway NGL Pipeline announcement stands out for its direct link to potential volume-driven revenue growth through 2027. This project exemplifies how Targa is expanding throughput capacity, yet also highlights the common sector risk of pushing major expansions just as competitors do, which could impact future pricing power if infrastructure growth outpaces demand.

Yet, amid these large-scale investments, investors should also be mindful of a very different and equally important factor when it comes to...

Read the full narrative on Targa Resources (it's free!)

Targa Resources' outlook projects $23.6 billion in revenue and $2.4 billion in earnings by 2028. This scenario assumes an annual revenue growth rate of 11.4% and a $0.9 billion increase in earnings from the current $1.5 billion level.

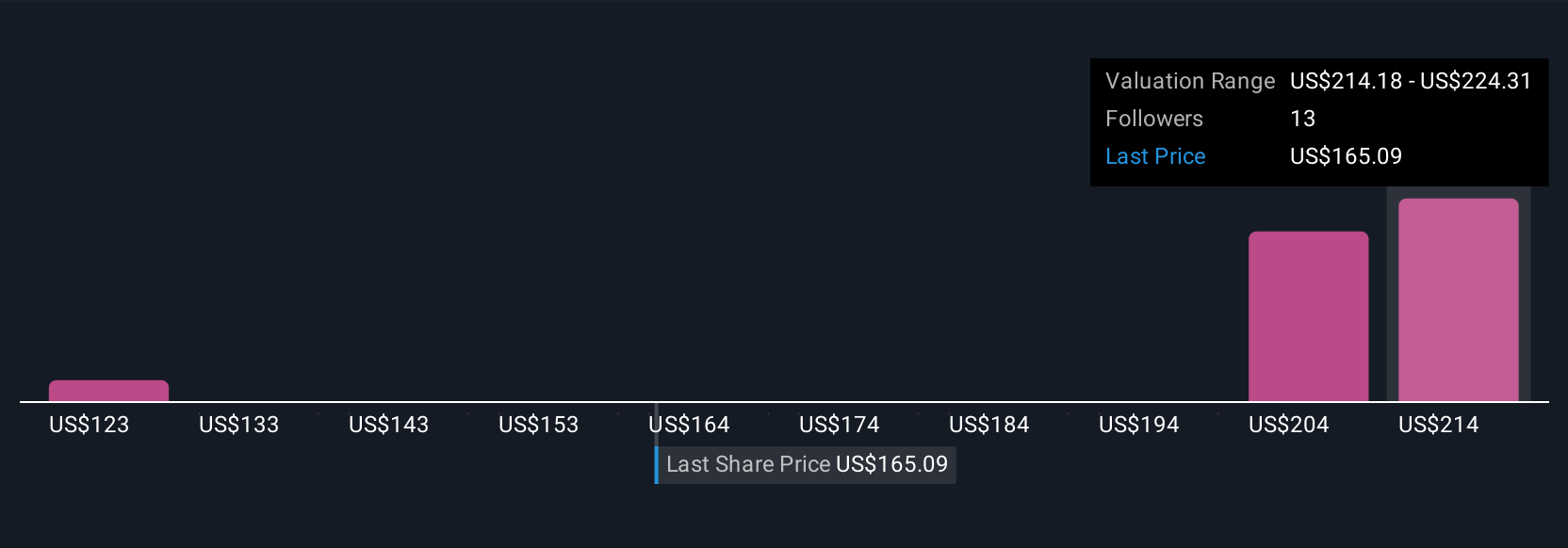

Uncover how Targa Resources' forecasts yield a $205.30 fair value, a 23% upside to its current price.

Exploring Other Perspectives

Fair value estimates for Targa Resources from six Simply Wall St Community members range from US$123 up to US$321.46 per share. With so much variation, and as midstream overbuild remains a key risk for margin stability, you may find sharply contrasting expectations about what the future holds for the company’s performance, consider reviewing several viewpoints before deciding where you stand.

Explore 6 other fair value estimates on Targa Resources - why the stock might be worth 26% less than the current price!

Build Your Own Targa Resources Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Targa Resources research is our analysis highlighting 4 key rewards and 3 important warning signs that could impact your investment decision.

- Our free Targa Resources research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Targa Resources' overall financial health at a glance.

Seeking Other Investments?

Our top stock finds are flying under the radar-for now. Get in early:

- Outshine the giants: these 25 early-stage AI stocks could fund your retirement.

- Find companies with promising cash flow potential yet trading below their fair value.

- Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 35 best rare earth metal stocks of the very few that mine this essential strategic resource.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Targa Resources might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TRGP

Targa Resources

Together with its subsidiary, Targa Resources Partners LP, owns, operates, acquires, and develops a portfolio of complementary domestic infrastructure assets in North America.

Proven track record and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|0.7% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|14.9% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor