Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:SUN

Sunoco (SUN): Revisiting Valuation After Recent Pullback and Strong 5-Year Total Shareholder Return

Sunoco (SUN) has quietly outperformed many income names over the past year, and the recent drift in its unit price is giving investors a fresh chance to revisit the fuel distributor’s long term story.

See our latest analysis for Sunoco.

The recent pullback, including a 7 day share price return of negative 3.2 percent from 54.43 dollars, comes after a solid 3 month share price return of 7 percent and a standout 5 year total shareholder return of roughly 157 percent. This suggests that long term momentum remains firmly intact even as short term sentiment cools.

If Sunoco’s steady gains have you thinking bigger picture, this is a good moment to broaden your watchlist and explore fast growing stocks with high insider ownership.

With analysts still seeing upside from here and earnings expanding faster than revenue, the key question is whether Sunoco’s strong fundamentals are underappreciated or if the market is already pricing in years of growth ahead.

Most Popular Narrative Narrative: 15.9% Undervalued

Compared with Sunoco’s last close, the most widely followed narrative implies a higher fair value, framing today’s price as a potential discount entry point.

The NuStar and upcoming Parkland and TanQuid acquisitions are expected to deliver substantial double-digit accretion and cost synergies, further increasing operating leverage and net margins while materially enhancing Sunoco's international and midstream asset footprint.

Want to see what kind of revenue runway and profit margins are baked into that outlook, and how fast earnings must climb to justify it? The narrative maps out a precise growth path, a sharply lower future multiple, and a specific discount rate that all have to line up perfectly. Curious how those moving parts combine to reach its fair value target? Dive in to see the full playbook behind the numbers.

Result: Fair Value of $64.71 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, sustained EV adoption or weaker US gasoline demand could pressure volumes and margins, challenging the acquisition-driven growth path behind today’s undervaluation.

Find out about the key risks to this Sunoco narrative.

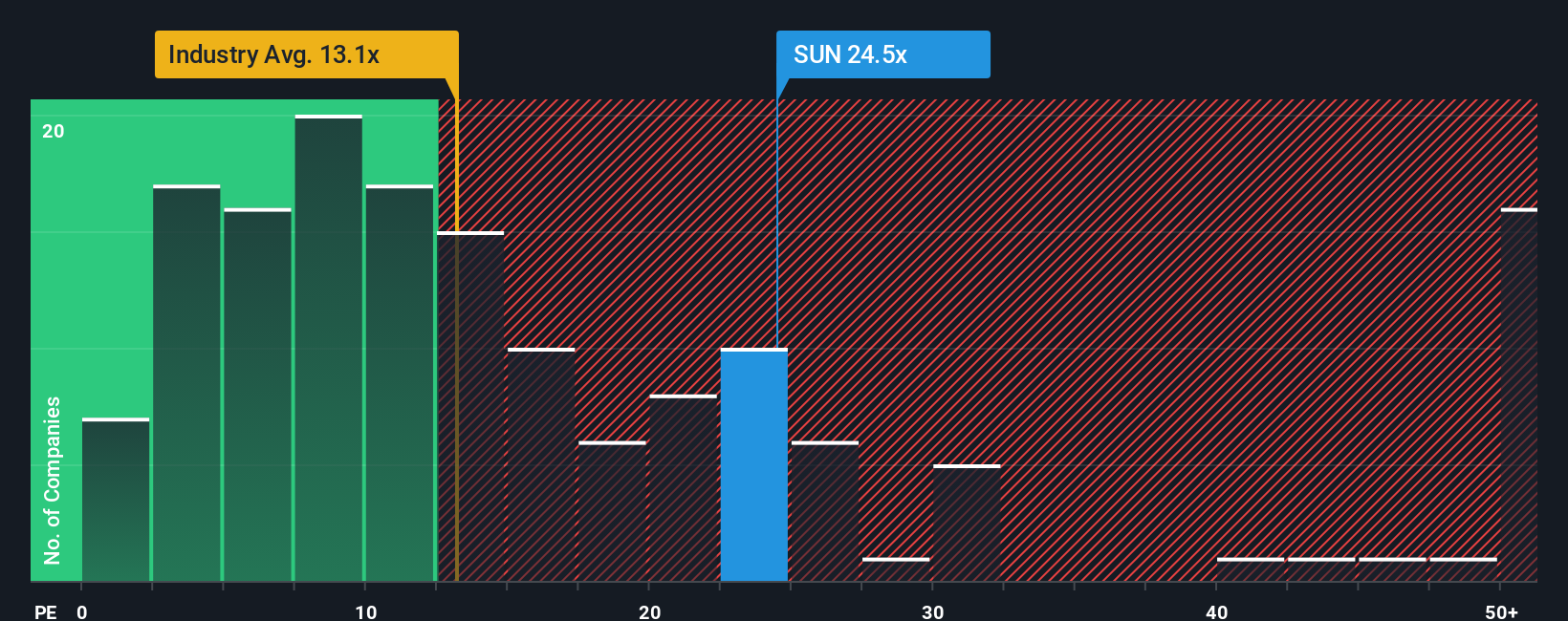

Another Angle on Valuation

Analysts and narratives see upside, but the market is currently paying 25.5 times earnings for Sunoco, richer than both the US Oil and Gas industry at 13.8 times and peers at 22.7 times, even though our fair ratio sits higher at 29 times. Is that a cushion or a warning?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Sunoco Narrative

If you see the story unfolding differently or want to follow your own research trail, you can craft a complete narrative in minutes, Do it your way.

A great starting point for your Sunoco research is our analysis highlighting 2 key rewards and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, explore your next potential opportunity with tailored stock ideas from the Simply Wall Street Screener, built to match focused strategies.

- Target long-term growth by screening for these 906 undervalued stocks based on cash flows that the market may not have fully priced in.

- Consider cutting edge innovation by following these 26 AI penny stocks positioned within the AI theme.

- Explore income-focused opportunities with these 15 dividend stocks with yields > 3% offering dividend yields above 3 percent.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:SUN

Sunoco

Engages in the energy infrastructure and distribution of motor fuels in the United States.

Established dividend payer and fair value.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RI

Rick_Orford on Upside Gold ·

This OVERLOOKED Gold Stock Could TRIPLE - 3.3M Ounces, Bottom-of-Peer Valuation

Fair Value:CA$470.5% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

6 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9719.1% undervalued

54 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1925.7% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

BJ

Bjergby on PagSeguro Digital ·

PagSeguro: A Cheap Bet on a Bank Hiding Inside a Payments Company, Priced for Failure

Fair Value:US$19.251.3% undervalued

17 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

Recently Updated Narratives

KA

kapirey on Hangzhou Oxygen Plant Group ·

The company must capitalize on its R&D&I over the next 10 years; it is still too early to infer the outcome.

Fair Value:CN¥24.481.5% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

KA

kapirey on Sinopec Shanghai Petrochemical ·

Capital expenditures remain required regardless of profitability

Fair Value:HK$0.32253.1% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

HU

Hunter_Z on Catcha Digital Berhad ·

Catcha Digital Q1 FY2026 Analysis - Acquisition-led growth is starting to convert into stronger operating earnings

Fair Value:RM 0.5451.9% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

GO

GoldenSands on QuantumScape ·

QuantumScape: A Mispriced Deep‑Tech Inflection Point With Multi‑Billion‑Dollar Optionality

Fair Value:US$8589.4% undervalued

120 followersusers have followed this narrative

2 commentsusers have commented on this narrative

34 likesusers have liked this narrative

CL

Clive_Thompson on Take-Two Interactive Software ·

Take-Two Interactive: The Calm Before the Storm NASDAQ: TTWO Last Price: $242.41 Date: May 15, 2026

Fair Value:US$276.9719.1% undervalued

54 followersusers have followed this narrative

0 commentsusers have commented on this narrative

13 likesusers have liked this narrative

NI

niteco on Honeywell International ·

Honeywell - The Demand-Side of the AI Infrastructure

Fair Value:US$320.1925.7% undervalued

43 followersusers have followed this narrative

0 commentsusers have commented on this narrative

17 likesusers have liked this narrative

Trending Discussion

AU

Aurelius on Greatland Resources ·

Your estimates may prove conservative, which is no bad thing. Telfer's scale remains underappreciate...

0

|0