- United States

- /

- Oil and Gas

- /

- NYSE:SFL

Investors Shouldn't Be Too Comfortable With SFL's (NYSE:SFL) Earnings

Last week's profit announcement from SFL Corporation Ltd. (NYSE:SFL) was underwhelming for investors, despite headline numbers being robust. Our analysis uncovered some concerning factors that we believe the market might be paying attention to.

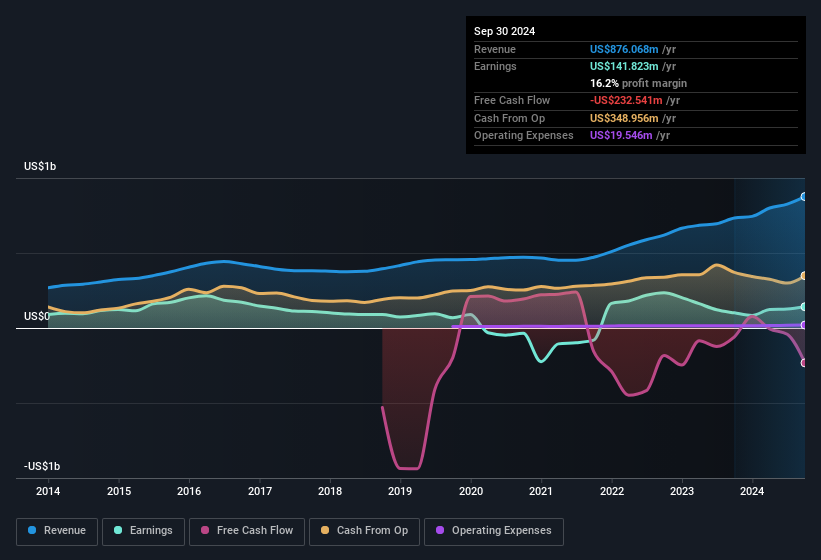

View our latest analysis for SFL

To understand the value of a company's earnings growth, it is imperative to consider any dilution of shareholders' interests. In fact, SFL increased the number of shares on issue by 6.6% over the last twelve months by issuing new shares. Therefore, each share now receives a smaller portion of profit. To celebrate net income while ignoring dilution is like rejoicing because you have a single slice of a larger pizza, but ignoring the fact that the pizza is now cut into many more slices. You can see a chart of SFL's EPS by clicking here.

A Look At The Impact Of SFL's Dilution On Its Earnings Per Share (EPS)

Three years ago, SFL lost money. The good news is that profit was up 40% in the last twelve months. On the other hand, earnings per share are only up 40% over the same period. And so, you can see quite clearly that dilution is influencing shareholder earnings.

Changes in the share price do tend to reflect changes in earnings per share, in the long run. So SFL shareholders will want to see that EPS figure continue to increase. But on the other hand, we'd be far less excited to learn profit (but not EPS) was improving. For that reason, you could say that EPS is more important that net income in the long run, assuming the goal is to assess whether a company's share price might grow.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On SFL's Profit Performance

SFL shareholders should keep in mind how many new shares it is issuing, because, dilution clearly has the power to severely impact shareholder returns. Because of this, we think that it may be that SFL's statutory profits are better than its underlying earnings power. But at least holders can take some solace from the 40% EPS growth in the last year. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. Every company has risks, and we've spotted 4 warning signs for SFL (of which 3 can't be ignored!) you should know about.

This note has only looked at a single factor that sheds light on the nature of SFL's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks with high insider ownership.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:SFL

SFL

A maritime and offshore asset owning and chartering company, engages in the ownership, operation, and chartering out of vessels and offshore related assets on medium and long-term charters.

Undervalued with solid track record.