- United States

- /

- Oil and Gas

- /

- NYSE:PRT

Don't Race Out To Buy PermRock Royalty Trust (NYSE:PRT) Just Because It's Going Ex-Dividend

PermRock Royalty Trust (NYSE:PRT) is about to trade ex-dividend in the next three days. If you purchase the stock on or after the 27th of November, you won't be eligible to receive this dividend, when it is paid on the 14th of December.

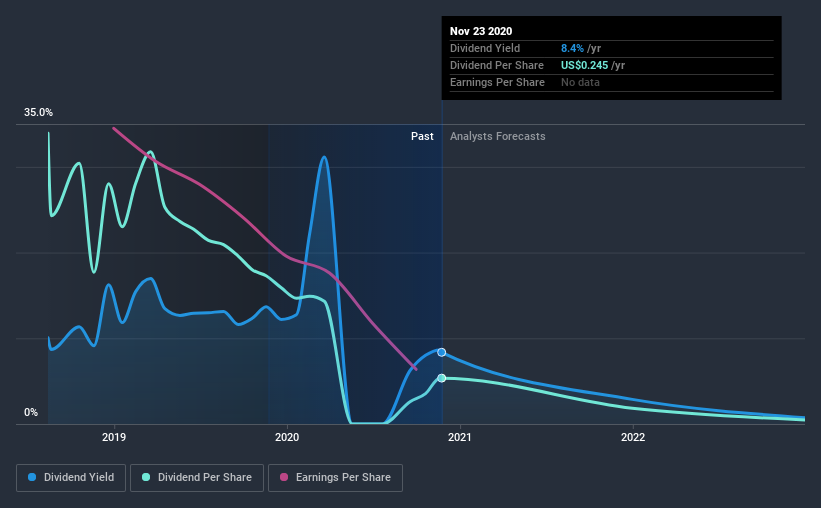

PermRock Royalty Trust's next dividend payment will be US$0.02 per share, on the back of last year when the company paid a total of US$0.12 to shareholders. Based on the last year's worth of payments, PermRock Royalty Trust has a trailing yield of 8.4% on the current stock price of $2.925. If you buy this business for its dividend, you should have an idea of whether PermRock Royalty Trust's dividend is reliable and sustainable. So we need to check whether the dividend payments are covered, and if earnings are growing.

View our latest analysis for PermRock Royalty Trust

Dividends are typically paid out of company income, so if a company pays out more than it earned, its dividend is usually at a higher risk of being cut. Last year PermRock Royalty Trust paid out 100% of its profits as dividends to shareholders, suggesting the dividend is not well covered by earnings.

Click here to see the company's payout ratio, plus analyst estimates of its future dividends.

Have Earnings And Dividends Been Growing?

Businesses with shrinking earnings are tricky from a dividend perspective. If business enters a downturn and the dividend is cut, the company could see its value fall precipitously. From this perspective, we're disturbed to see earnings per share plunged 29% over the last 12 months, and we'd wonder if the company has had some kind of major event that has skewed the calculation.

Another key way to measure a company's dividend prospects is by measuring its historical rate of dividend growth. PermRock Royalty Trust's dividend payments per share have declined at 60% per year on average over the past two years, which is uninspiring. It's never nice to see earnings and dividends falling, but at least management has cut the dividend rather than potentially risk the company's health in an attempt to maintain it.

Final Takeaway

Is PermRock Royalty Trust an attractive dividend stock, or better left on the shelf? Not only are earnings per share shrinking, but PermRock Royalty Trust is paying out a disconcertingly high percentage of its profit as dividends. It's not that we hate the business, but we feel that these characeristics are not desirable for investors seeking a reliable dividend stock to own for the long term. This is not an overtly appealing combination of characteristics, and we're just not that interested in this company's dividend.

With that being said, if you're still considering PermRock Royalty Trust as an investment, you'll find it beneficial to know what risks this stock is facing. To that end, you should learn about the 6 warning signs we've spotted with PermRock Royalty Trust (including 1 which shouldn't be ignored).

We wouldn't recommend just buying the first dividend stock you see, though. Here's a list of interesting dividend stocks with a greater than 2% yield and an upcoming dividend.

If you decide to trade PermRock Royalty Trust, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NYSE:PRT

Flawless balance sheet and fair value.

Market Insights

Community Narratives