Advertisement

- United States

- /

- Oil and Gas

- /

- NYSE:KRP

Does Kimbell Royalty Partners (KRP) Face a Shifting Competitive Landscape as Larger Rivals Advance?

Simply Wall St

Reviewed by Sasha Jovanovic

- Earlier this week, KeyBanc downgraded Kimbell Royalty Partners, LP from 'Overweight' to 'Sector Weight' due to a volatile oil price environment and limited growth prospects in the Permian basin.

- This downgrade highlights increasing pressure on smaller mineral rights companies as they compete with larger, better-capitalized peers in the acquisition market.

- We’ll explore how concerns about competition from larger players may influence the investment outlook for Kimbell Royalty Partners.

We've found 15 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

Kimbell Royalty Partners Investment Narrative Recap

To be a shareholder of Kimbell Royalty Partners right now, you need to believe in the long-term value of diversified oil and gas royalty interests, supported by ongoing production and disciplined acquisitions. The recent downgrade by KeyBanc emphasizes increased competition and limited growth in the Permian, which poses a risk to near-term M&A-driven growth but does not materially shift the main short-term catalyst: successfully executing acquisitions to offset natural production declines. The biggest risk remains the ability to acquire high-yielding mineral interests as competition from larger entities intensifies. A key announcement tying into this risk is Kimbell’s recent dividend decline, with the Q3 cash distribution falling to $0.35 per unit as the partnership directed 25% of available cash to debt repayment. This move follows consecutive quarterly dividend reductions this year and correlates with the current pressure on acquisition economics and distributable cash flow, an area investors are watching closely amid weaker energy pricing. But the real concern that investors should keep front of mind is the growing difficulty of finding attractively priced, high-quality mineral interests as...

Read the full narrative on Kimbell Royalty Partners (it's free!)

Kimbell Royalty Partners' outlook anticipates $379.9 million in revenue and $80.8 million in earnings by 2028. This forecast is based on a 6.7% annual revenue growth rate and an increase in earnings from -$0.5 million today to $80.8 million, representing an $81.3 million improvement.

Uncover how Kimbell Royalty Partners' forecasts yield a $17.20 fair value, a 38% upside to its current price.

Exploring Other Perspectives

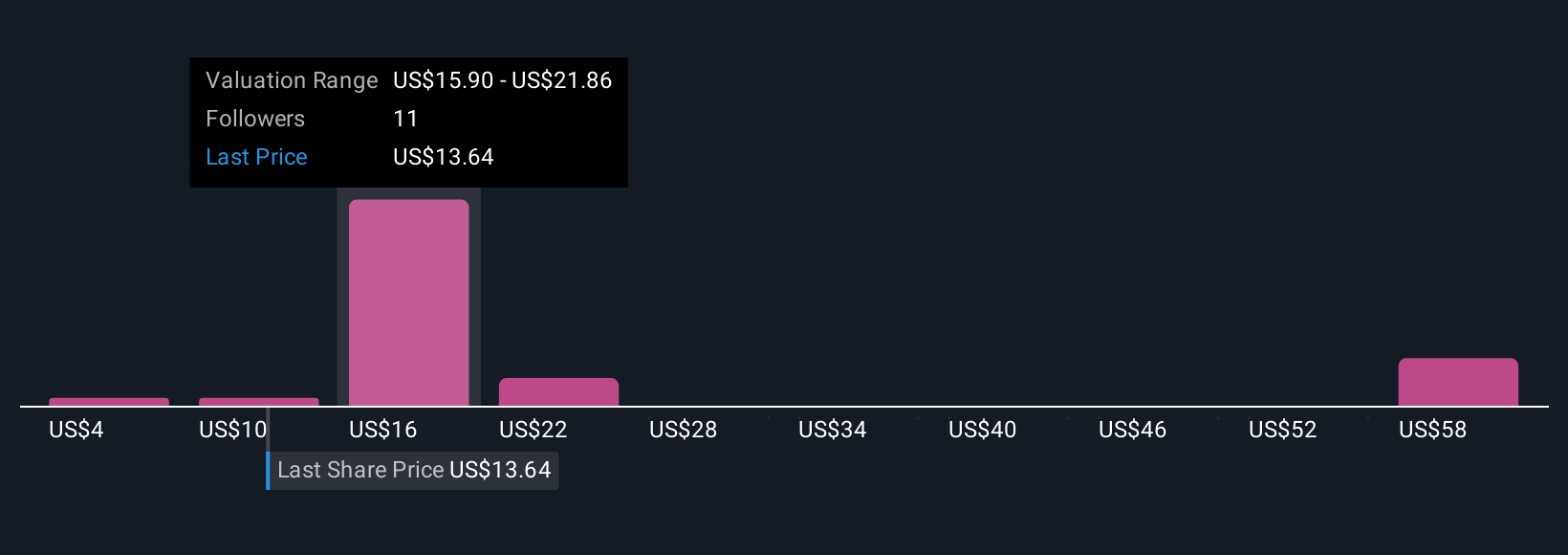

Simply Wall St Community user estimates for Kimbell Royalty Partners’ fair value span widely from US$4 to nearly US$60 across six perspectives. In light of increasingly competitive M&A conditions, you can see how opinions on the path ahead may differ, consider exploring several viewpoints to inform your own outlook.

Explore 6 other fair value estimates on Kimbell Royalty Partners - why the stock might be worth over 4x more than the current price!

Build Your Own Kimbell Royalty Partners Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Kimbell Royalty Partners research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

- Our free Kimbell Royalty Partners research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Kimbell Royalty Partners' overall financial health at a glance.

Want Some Alternatives?

Every day counts. These free picks are already gaining attention. See them before the crowd does:

- AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Kimbell Royalty Partners might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:KRP

Kimbell Royalty Partners

Owns and acquires mineral and royalty interests in oil and natural gas properties in the United States.

Moderate growth potential with mediocre balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

138 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

931 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative