- United States

- /

- Oil and Gas

- /

- NYSE:HESM

Hess Midstream's (NYSE:HESM) Upcoming Dividend Will Be Larger Than Last Year's

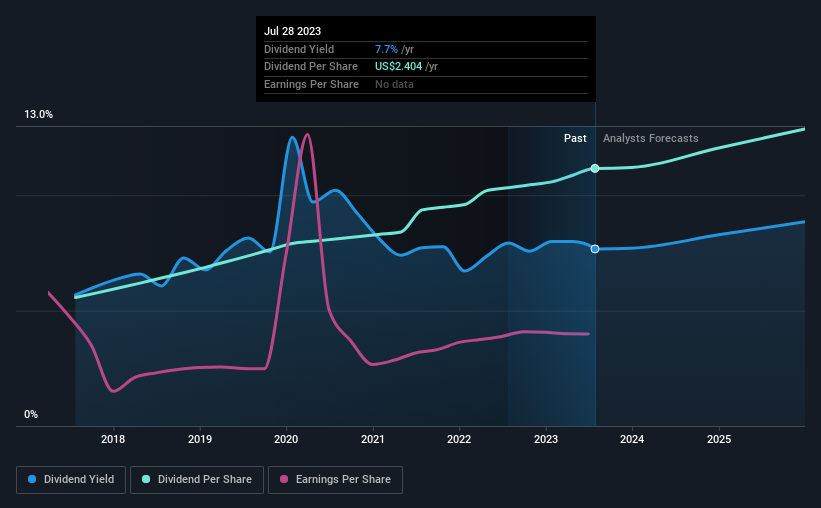

Hess Midstream LP's (NYSE:HESM) dividend will be increasing from last year's payment of the same period to $0.6011 on 14th of August. This will take the dividend yield to an attractive 7.7%, providing a nice boost to shareholder returns.

Check out our latest analysis for Hess Midstream

Hess Midstream Is Paying Out More Than It Is Earning

Impressive dividend yields are good, but this doesn't matter much if the payments can't be sustained. Based on the last payment, Hess Midstream's profits didn't cover the dividend, but the company was generating enough cash instead. Generally, we think cash is more important than accounting measures of profit, so with the cash flows easily covering the dividend, we don't think there is much reason to worry.

Over the next year, EPS is forecast to expand by 54.9%. However, if the dividend continues along recent trends, it could start putting pressure on the balance sheet with the payout ratio reaching 139% over the next year.

Hess Midstream Is Still Building Its Track Record

Even though the company has been paying a consistent dividend for a while, we would like to see a few more years before we feel comfortable relying on it. Since 2017, the annual payment back then was $1.20, compared to the most recent full-year payment of $2.4. This works out to be a compound annual growth rate (CAGR) of approximately 12% a year over that time. We're not overly excited about the relatively short history of dividend payments, however the dividend is growing at a nice rate and we might take a closer look.

The Dividend's Growth Prospects Are Limited

Investors could be attracted to the stock based on the quality of its payment history. Earnings have grown at around 2.5% a year for the past five years, which isn't massive but still better than seeing them shrink. So the company has struggled to grow its EPS yet it's still paying out 116% of its earnings. Limited recent earnings growth and a high payout ratio makes it hard for us to envision strong future dividend growth, unless the company should have substantial pricing power or some form of competitive advantage.

An additional note is that the company has been raising capital by issuing stock equal to 58% of shares outstanding in the last 12 months. Trying to grow the dividend when issuing new shares reminds us of the ancient Greek tale of Sisyphus - perpetually pushing a boulder uphill. Companies that consistently issue new shares are often suboptimal from a dividend perspective.

Our Thoughts On Hess Midstream's Dividend

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. In the past, the payments have been unstable, but over the short term the dividend could be reliable, with the company generating enough cash to cover it. We don't think Hess Midstream is a great stock to add to your portfolio if income is your focus.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Case in point: We've spotted 4 warning signs for Hess Midstream (of which 2 make us uncomfortable!) you should know about. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if Hess Midstream might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:HESM

Hess Midstream

Owns, develops, operates, and acquires midstream assets and provide fee-based services to Hess and third-party customers in the United States.

Solid track record with reasonable growth potential.