Advertisement

- United States

- /

- Oil and Gas

- /

- NasdaqGS:CLNE

Investors Appear Satisfied With Clean Energy Fuels Corp.'s (NASDAQ:CLNE) Prospects As Shares Rocket 26%

Clean Energy Fuels Corp. (NASDAQ:CLNE) shares have continued their recent momentum with a 26% gain in the last month alone. Unfortunately, the gains of the last month did little to right the losses of the last year with the stock still down 16% over that time.

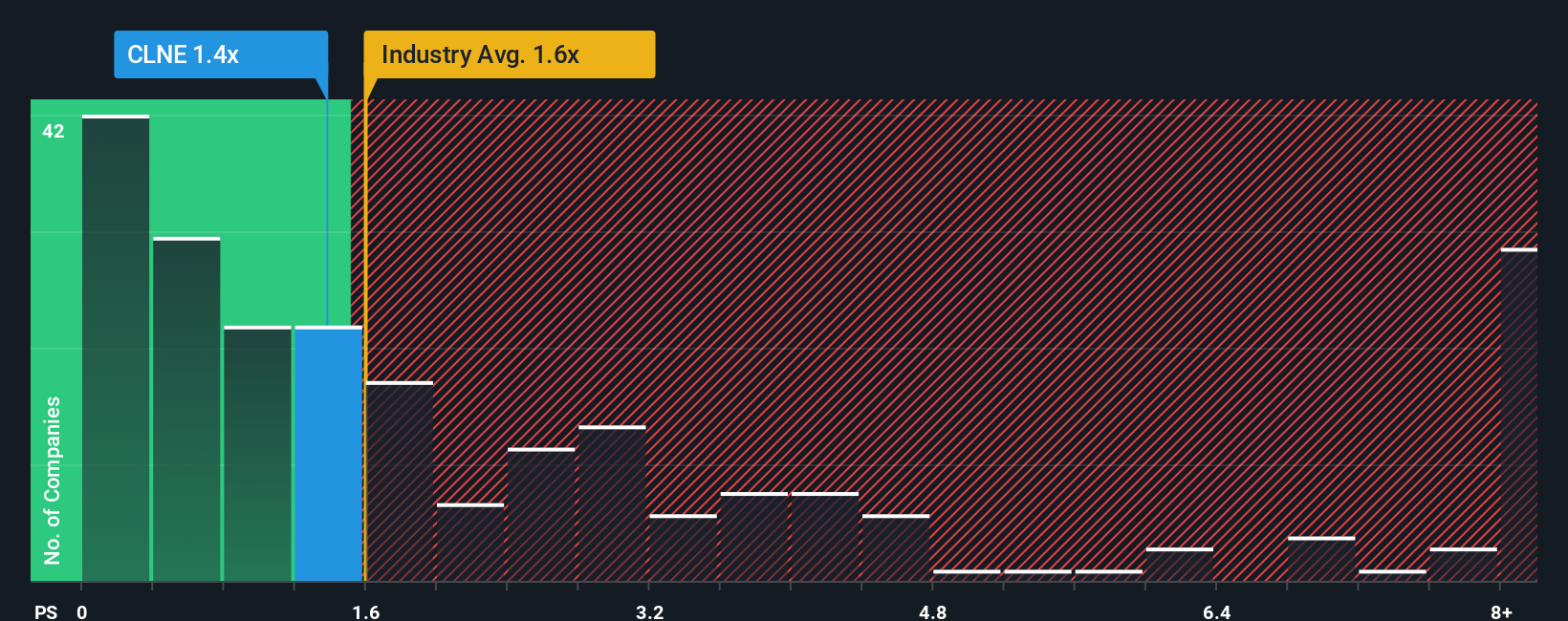

Although its price has surged higher, there still wouldn't be many who think Clean Energy Fuels' price-to-sales (or "P/S") ratio of 1.4x is worth a mention when the median P/S in the United States' Oil and Gas industry is similar at about 1.6x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

View our latest analysis for Clean Energy Fuels

What Does Clean Energy Fuels' P/S Mean For Shareholders?

There hasn't been much to differentiate Clean Energy Fuels' and the industry's revenue growth lately. It seems that many are expecting the mediocre revenue performance to persist, which has held the P/S ratio back. If you like the company, you'd be hoping this can at least be maintained so that you could pick up some stock while it's not quite in favour.

Keen to find out how analysts think Clean Energy Fuels' future stacks up against the industry? In that case, our free report is a great place to start.How Is Clean Energy Fuels' Revenue Growth Trending?

Clean Energy Fuels' P/S ratio would be typical for a company that's only expected to deliver moderate growth, and importantly, perform in line with the industry.

If we review the last year of revenue growth, the company posted a worthy increase of 4.1%. The latest three year period has also seen a 17% overall rise in revenue, aided somewhat by its short-term performance. Accordingly, shareholders would have probably been satisfied with the medium-term rates of revenue growth.

Shifting to the future, estimates from the six analysts covering the company suggest revenue should grow by 4.1% per annum over the next three years. With the industry predicted to deliver 4.0% growth each year, the company is positioned for a comparable revenue result.

With this information, we can see why Clean Energy Fuels is trading at a fairly similar P/S to the industry. It seems most investors are expecting to see average future growth and are only willing to pay a moderate amount for the stock.

The Bottom Line On Clean Energy Fuels' P/S

Its shares have lifted substantially and now Clean Energy Fuels' P/S is back within range of the industry median. While the price-to-sales ratio shouldn't be the defining factor in whether you buy a stock or not, it's quite a capable barometer of revenue expectations.

We've seen that Clean Energy Fuels maintains an adequate P/S seeing as its revenue growth figures match the rest of the industry. Right now shareholders are comfortable with the P/S as they are quite confident future revenue won't throw up any surprises. Unless these conditions change, they will continue to support the share price at these levels.

Before you settle on your opinion, we've discovered 2 warning signs for Clean Energy Fuels that you should be aware of.

It's important to make sure you look for a great company, not just the first idea you come across. So if growing profitability aligns with your idea of a great company, take a peek at this free list of interesting companies with strong recent earnings growth (and a low P/E).

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:CLNE

Clean Energy Fuels

Offers natural gas as alternative fuels for vehicle fleets and related fueling solutions in the United States and Canada.

Excellent balance sheet and fair value.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|48.7% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|6.4% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|19.4% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|51.6% overvalued

RO

Community Contributor