Advertisement

- United States

- /

- Energy Services

- /

- NasdaqGS:BKR

A Look at Baker Hughes's Valuation After Landmark Tangguh LNG Service Deal with bp

Kshitija Bhandaru

Reviewed by Simply Wall St

Baker Hughes (BKR) just landed a comprehensive 90-month service agreement with bp for the Tangguh LNG plant in Indonesia, and this is the sort of deal that grabs investors' attention. The agreement extends their partnership with bp and puts Baker Hughes in charge of spare parts, repairs, and field engineering for high-stakes turbomachinery at a major energy hub in the Asia-Pacific region. For investors watching the company’s moves in LNG and critical equipment services, this news could signal another step in expanding Baker Hughes' role as a strategic solutions provider in rapidly growing markets.

Looking back over the past year, Baker Hughes' stock has climbed 31%. Stronger momentum has been evident over the past three months, as shares surged nearly 20%. While the latest month brought some volatility, longer-term investors have seen significant returns, especially with a three-year gain above 90%. The company has built up its backlog through multiple service contract awards and continues to emphasize its foothold in the Asia-Pacific, as seen in recent deals supporting bp’s Tangguh UCC Project and service expansions across the region.

With shares on a steady upward swing and recent service agreements adding to the pipeline, the question is whether Baker Hughes offers value at current prices or if markets have already factored in its growth ambitions. What do you think? Is there still an opportunity here, or is the stock already pricing in all the good news?

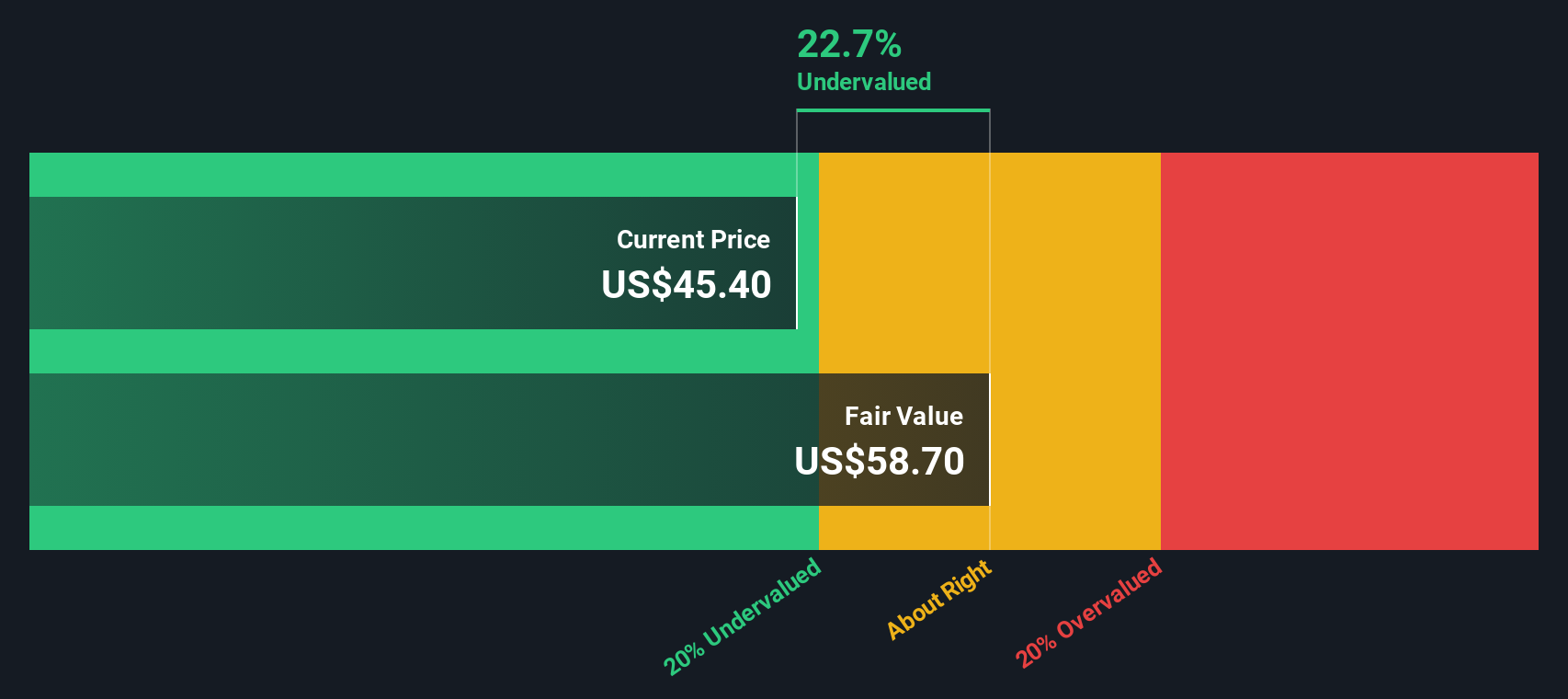

Most Popular Narrative: 10.6% Undervalued

According to community narrative, Baker Hughes is seen as undervalued by analysts, with a fair value estimate that is noticeably above its latest share price. The narrative suggests several catalysts supporting a higher valuation despite expected slowdowns in growth metrics.

Baker Hughes is actively expanding into fast-growing markets like distributed power solutions for data centers and new energy infrastructure (hydrogen, CCS, geothermal). The company is capitalizing on the robust increase in global energy demand, especially from digital infrastructure and emerging markets. These efforts are positioning the company for long-term recurring revenue growth and higher-margin opportunities.

What is fueling this projected valuation uplift? A powerful mix of expansion bets, premium market positioning, and numbers that challenge conventional sector norms. The story hinges on bold forecasts for revenue, profits, and future earnings multiples, all riding on a strategic pivot into data and energy innovation. Interested in the details behind these numbers and why the narrative projects a significantly higher value? The full analysis reveals the specific assumptions that drive this optimistic outlook. Could these be the clues to a breakout?

Result: Fair Value of $50.10 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.However, risks such as global trade tensions or renewed cost pressures could undermine Baker Hughes' margin targets. These issues may spark questions about whether growth forecasts will hold up.

Find out about the key risks to this Baker Hughes narrative.Another View: Discounted Cash Flow Model

Looking at our DCF model, the story is a bit different. This approach suggests Baker Hughes is undervalued by a significant margin, providing an alternative perspective on what the shares are really worth. Could this deeper value be what sets expectations for a surprise move?

Look into how the SWS DCF model arrives at its fair value.

Simply Wall St performs a discounted cash flow (DCF) on every stock in the world every day (check out Baker Hughes for example). We show the entire calculation in full. You can track the result in your watchlist or portfolio and be alerted when this changes, or use our stock screener to discover undervalued stocks based on their cash flows. If you save a screener we even alert you when new companies match - so you never miss a potential opportunity.

Build Your Own Baker Hughes Narrative

If you want to dive into the numbers firsthand or challenge these perspectives with your own insights, it's simple to put together your own take and see how it stacks up. Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Baker Hughes.

Looking for more investment ideas?

Sharpen your portfolio by tapping into powerful trends others might overlook. Take charge of your investing journey and seize opportunities smarter, faster, and ahead of the crowd. Don’t wait for the next big story to pass you by. Find your edge below.

- Boost your income stream with standout picks among dividend stocks with yields > 3%, featuring companies with yields over 3%, so your money works harder for you.

- Step into the frontier of technology by tracking the rapid growth of AI penny stocks, where artificial intelligence is creating tomorrow’s market leaders.

- Capitalize on value opportunities by uncovering hidden gems through undervalued stocks based on cash flows, and position yourself for potential upside before the crowd catches on.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Baker Hughes might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About NasdaqGS:BKR

Baker Hughes

Provides a portfolio of technologies and services to energy and industrial value chain worldwide.

Flawless balance sheet with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|48.7% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|6.4% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|19.4% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|51.6% overvalued

RO

Community Contributor