- United States

- /

- Diversified Financial

- /

- NYSE:WU

Western Union (NYSE:WU) Reports Strong Q3 Earnings Growth and Revises 2024 Revenue Guidance

Reviewed by Simply Wall St

Western Union (NYSE:WU) recently announced its Q3 2024 earnings, showcasing a significant increase in net income to $264.8 million, up from $171 million the previous year, despite a slight decline in sales. The company revised its 2024 earnings guidance, projecting revenues between $4.13 billion and $4.20 billion, reflecting cautious optimism with ongoing financial pressures. Key areas covered in the company report include financial health, growth avenues through digital transformation, and regulatory challenges.

See the full analysis report here for a deeper understanding of Western Union.

Core Advantages Driving Sustained Success for Western Union

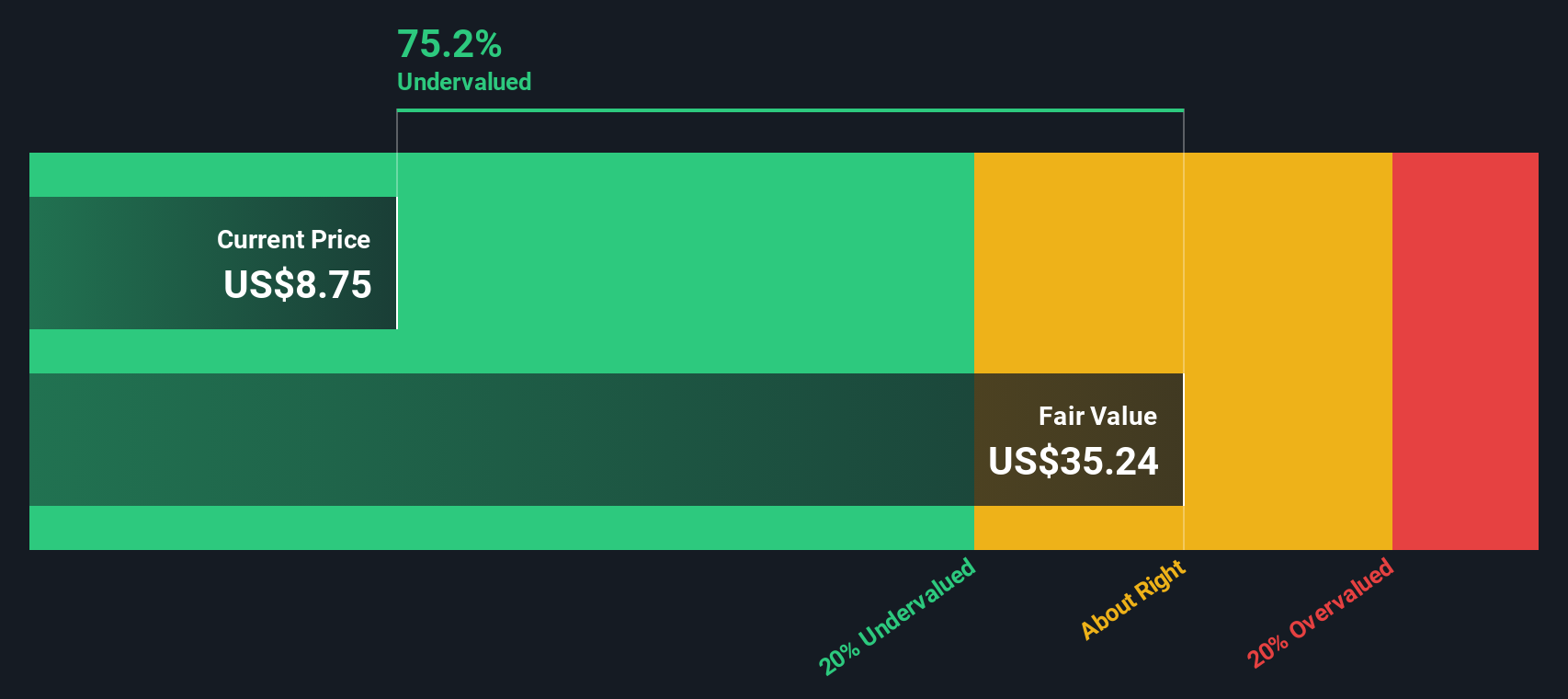

Western Union's financial health is underscored by a return on equity of 103.49%, which, despite being influenced by debt levels, indicates strong profitability. The company has consistently provided stable dividends over the past decade, boasting a yield of 8.67% with a low payout ratio of 48.1%, ensuring dividends are well-covered by earnings. Recent earnings results highlight a net income increase to $264.8 million for Q3 2024, up from $171 million the previous year, showcasing effective cost management. Additionally, the company is trading at $10.84, significantly below the SWS fair value of $30.68, suggesting strong market positioning. Learn about Western Union's dividend strategy and how it impacts shareholder returns and financial stability.

Vulnerabilities Impacting Western Union

Challenges arise with a forecasted earnings decline of 4.6% annually over the next three years, compounded by a 9.7% earnings drop in the past year. Over the last five years, earnings have decreased by 7.5% annually, reflecting ongoing financial pressures. The company's net debt to equity ratio stands at 228.1%, raising concerns about financial leverage. Nevertheless, Western Union has revised its 2024 earnings guidance, expecting revenues between $4.13 billion and $4.20 billion, indicating cautious optimism. Explore the current health of Western Union and how it reflects on its financial stability and growth potential.

Growth Avenues Awaiting Western Union

Western Union is poised for growth through digital transformation, evidenced by a strategic partnership with Khipu that enhances digital transaction capabilities. This integration simplifies the remittance process, aligning with market trends favoring digital solutions. The company's commitment to innovation is further illustrated by its exploration of fintech partnerships, aiming to diversify service offerings and capture new customer segments. Such initiatives are expected to drive revenue growth, albeit at a modest 1.1% annually. See what the latest analyst reports say about Western Union's future prospects and potential market movements.

Regulatory Challenges Facing Western Union

Economic headwinds pose a risk to Western Union, with potential downturns impacting consumer spending and transaction volumes. Regulatory changes across jurisdictions add complexity, requiring careful navigation to ensure compliance. The competitive environment remains intense, demanding continuous innovation to maintain market share. Despite these threats, Western Union's strategic focus on digital services and operational efficiency positions it to tackle these challenges effectively. To gain deeper insights into Western Union's historical performance, explore our detailed analysis of past performance.

Conclusion

Western Union demonstrates a strong financial foundation with a high return on equity and a history of stable dividends, indicating its ability to generate profits effectively. However, challenges such as projected earnings declines and high debt levels persist. The company's strategic focus on digital transformation and partnerships positions it for future growth. The current trading price of $10.84, significantly lower than the estimated fair value of $30.68, suggests that the market may not fully recognize the potential benefits of its digital initiatives and cost management strategies. This discrepancy presents an opportunity for investors, as the company's strategic efforts could lead to improved financial performance and market recognition over time.

Next Steps

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

Valuation is complex, but we're here to simplify it.

Discover if Western Union might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About NYSE:WU

6 star dividend payer and undervalued.