Advertisement

- United States

- /

- Capital Markets

- /

- NYSE:OWL

Blue Owl Capital (OWL): Valuation Check After Insider Buying, Fundraising Success and Ongoing Class Action Lawsuits

Simply Wall St

Reviewed by Simply Wall St

Blue Owl Capital (OWL) is back in the spotlight after insiders bought heavily into the stock while the firm closed a new $1.7 billion digital infrastructure fund, even as class action lawsuits swirl.

See our latest analysis for Blue Owl Capital.

Those heavy insider purchases and the $1.7 billion digital infrastructure fund are landing against a mixed backdrop, with a recent 7 day share price return of 8.27% but a year to date share price return of negative 31.16%. At the same time, the 3 year total shareholder return of 65.96% hints that long term momentum, though dented, is not broken.

If Blue Owl’s rebound has you rethinking where management conviction matters most, now is a good moment to explore fast growing stocks with high insider ownership as potential next ideas.

With shares still trading at a steep discount to analyst targets despite brisk fundraising and insider conviction, is Blue Owl quietly undervalued, or is the market already bracing for weaker earnings and slower growth ahead?

Most Popular Narrative Narrative: 24.1% Undervalued

With Blue Owl Capital last closing at $16.24 against a narrative fair value of $21.40, the story hinges on powerful growth and margin assumptions.

Significant ongoing growth in permanent capital vehicles, particularly through expansion in private credit, real assets, and evergreen/interval fund strategies, is providing stable and recurring management fee revenue and positioning Blue Owl for higher future earnings and durable margin expansion.

Curious how steady fees could still support aggressive profit expansion and a lower future earnings multiple than many peers? Explore the full narrative playbook behind this valuation.

Result: Fair Value of $21.40 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, sustained fundraising slowdowns or tougher competition squeezing fees could easily derail those ambitious growth and margin assumptions that are embedded in today’s valuation.

Find out about the key risks to this Blue Owl Capital narrative.

Another Angle on Valuation

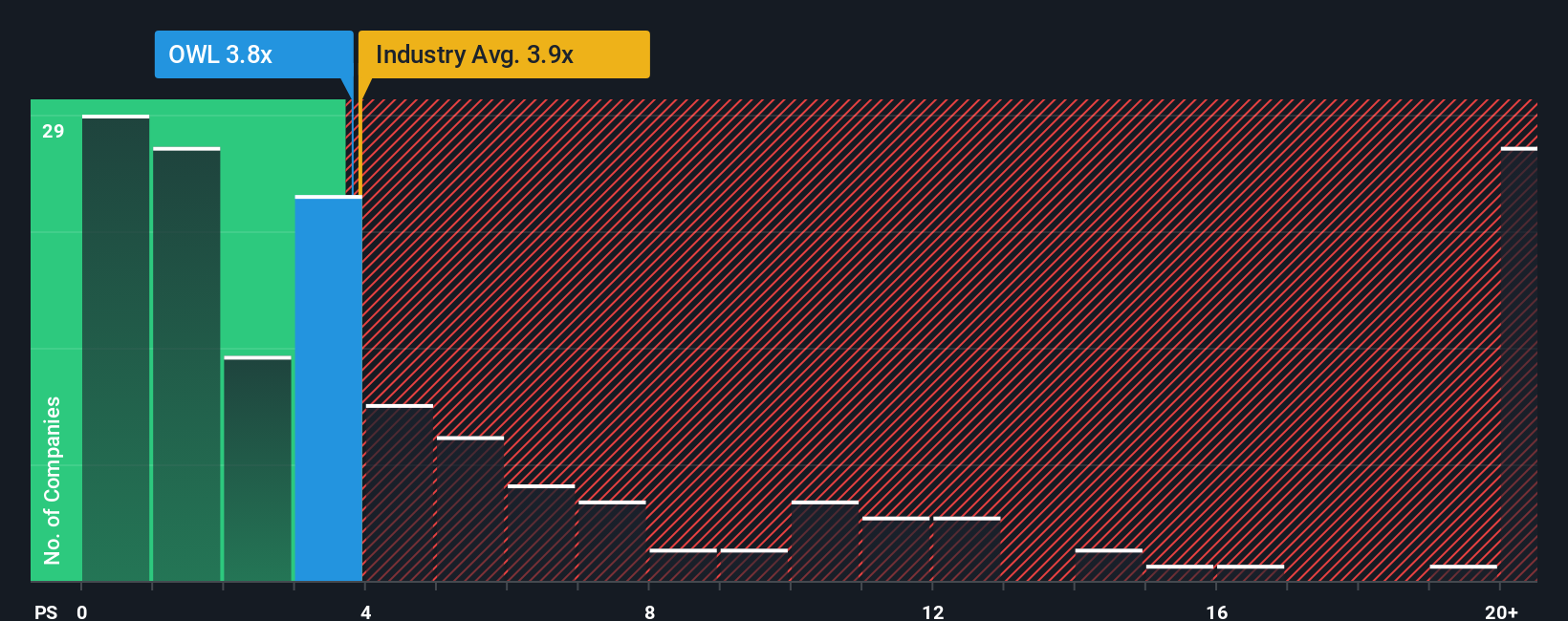

While the community fair value suggests upside, a simple price to sales lens paints Blue Owl as fully priced. The stock trades on 3.9 times sales, roughly in line with both its 3.9 times fair ratio and the 4 times industry average, leaving limited clear margin of safety.

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Blue Owl Capital Narrative

If you see the story differently or want to dig into the numbers yourself, you can build a custom view of Blue Owl in just minutes. Do it your way.

A great starting point for your Blue Owl Capital research is our analysis highlighting 1 key reward and 4 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Before you move on, explore your next opportunity by using our powerful screeners to pinpoint focused themes, strong fundamentals, and income friendly portfolios.

- Identify potential bargains early by targeting companies that our models flag as attractively priced through these 906 undervalued stocks based on cash flows.

- Find opportunities in the next wave of innovation by focusing on fast moving companies across these 26 AI penny stocks.

- Build your passive income stream by filtering for dependable payers among these 15 dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Blue Owl Capital might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:OWL

Blue Owl Capital

Operates as an alternative asset manager in the United States.

High growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$122.0% undervalued

8 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

10 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MO

mo7md on ADNOC Gas ·

ADNOC Gas future shines with a 21.4% revenue surge

Fair Value:د.إ3.728.9% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

IN

IncomeAssets on Pulse Seismic ·

Watch Pulse Seismic Outperform with 13.6% Revenue Growth in the Coming Years

Fair Value:CA$4.4727.3% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VL

Vladislav on Galleon Gold ·

Significantly undervalued gold explorer in Timmins, finally getting traction

Fair Value:CA$481.5% undervalued

7 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

116 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.2% undervalued

957 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

50 followersusers have followed this narrative

6 commentsusers have commented on this narrative

16 likesusers have liked this narrative