Advertisement

- United States

- /

- Diversified Financial

- /

- NYSE:MA

Mastercard (NYSE:MA) Strengthens Market Position with Safaricom Alliance Despite Valuation Concerns

Simply Wall St

Reviewed by Simply Wall St

Mastercard (NYSE:MA) is currently experiencing a mix of growth opportunities and financial challenges. The company has reported a 13% increase in net revenues and strategic partnerships that enhance its global payment infrastructure, yet it faces concerns over high debt levels and slower earnings growth forecasts. In the discussion that follows, we will explore Mastercard's unique capabilities, internal limitations, future market prospects, and external threats to provide a comprehensive overview of the company's current business situation.

Get an in-depth perspective on Mastercard's performance by reading our analysis here.

Unique Capabilities Enhancing Mastercard's Market Position

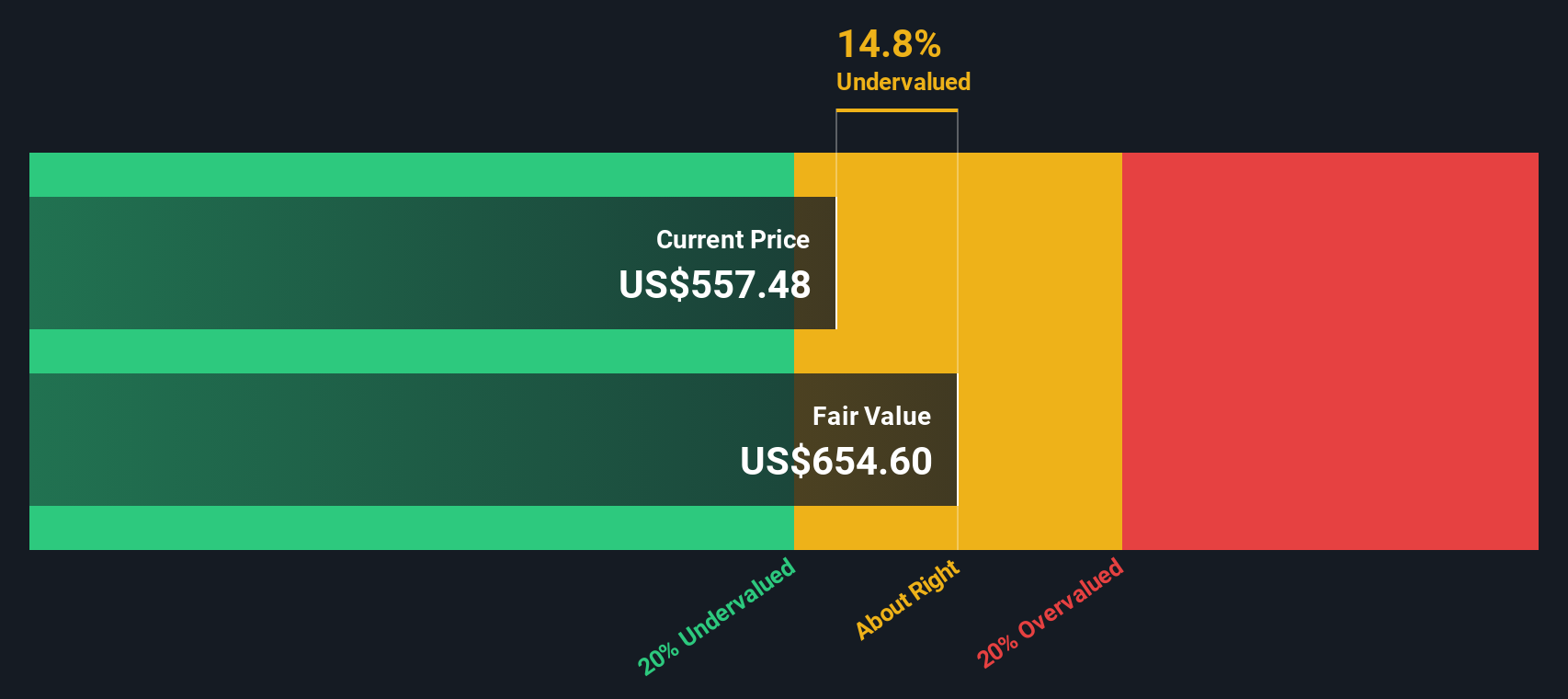

Mastercard has demonstrated strong financial performance with a 13% increase in net revenues and a 24% rise in adjusted net income year-over-year, as highlighted by CEO Michael Miebach. The company's diversified business model and healthy consumer spending have been pivotal in driving this momentum. Moreover, the strategic alliances, such as the recent partnership with Safaricom, are enhancing Mastercard's global payment infrastructure, offering seamless and scalable payment solutions. The company's management team, with its experienced leadership, continues to position Mastercard well for future growth, despite the macroeconomic challenges. However, the company's valuation presents a mixed picture. While trading slightly below its estimated fair value, Mastercard's Price-To-Earnings Ratio of 37x is significantly higher than both the industry average of 16x and peer average of 34.1x, suggesting a potential overvaluation.

Internal Limitations Hindering Mastercard's Growth

The company's financial health is overshadowed by a high debt-to-equity ratio of 208.6%, which could pose risks if not managed effectively. Operating expenses have increased by 10%, and a one-time restructuring charge is expected in the third quarter, as noted by CFO Sachin Mehra. Additionally, Mastercard's earnings growth forecast of 11.9% per year is slower than the US market average of 15.3%, indicating potential challenges in maintaining its competitive edge. The reliance on higher-risk external borrowing, without customer deposits, further underscores the financial vulnerabilities that Mastercard faces.

Future Prospects for Mastercard in the Market

Mastercard's strategic initiatives, such as expanding into high-growth markets and enhancing digital payment solutions, present significant opportunities. The company's focus on emerging markets like Africa, Latin America, and Asia Pacific aligns with the global shift towards digital payments. Product-related announcements, such as the Payment Passkey Service, are set to enhance online shopping security and convenience, potentially reducing fraud and increasing transaction approval rates. These efforts, coupled with strategic alliances like the one with Rellevate, position Mastercard to capitalize on the growing demand for digital financial services and drive financial inclusion.

External Factors Threatening Mastercard

Mastercard faces several external challenges, including intense competition in the US and European payment markets. Legal issues, such as the recent class action settlement involving ATM surcharges, add to the company's risks. The evolving digital environment, with increasing vulnerabilities and sophisticated fraud techniques, poses additional threats. Moreover, the mixed macroeconomic environment and signs of moderating labor market growth could impact consumer spending, a key driver of Mastercard's revenue. These factors, combined with the competitive pressures, necessitate a strategic approach to sustain growth and market share.

To gain deeper insights into Mastercard's historical performance, explore our detailed analysis of past performance.To dive deeper into how Mastercard's valuation metrics are shaping its market position, check out our detailed analysis of Mastercard's Valuation.

Conclusion

Mastercard's strong financial performance, highlighted by a 13% increase in net revenues and a 24% rise in adjusted net income, underscores its ability to leverage a diversified business model and strategic alliances to enhance its market position. However, the company's high debt-to-equity ratio and slower earnings growth forecast compared to the US market suggest potential financial vulnerabilities and competitive challenges. Despite trading slightly below its estimated fair value, Mastercard's Price-To-Earnings Ratio of 37x, which is significantly higher than the industry average of 16x and peer average of 34.1x, raises concerns about its current market valuation. As Mastercard continues to expand into high-growth markets and enhance digital payment solutions, it must navigate intense competition and external threats to sustain growth and capitalize on emerging opportunities.

Next Steps

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About NYSE:MA

Mastercard

A technology company, provides transaction processing and other payment-related products and services in the United States and internationally.

Solid track record with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Weekly Picks

WO

woodworthfund on MGP Ingredients ·

THE KINGDOM OF BROWN GOODS: WHY MGPI IS BEING CRUSHED BY INVENTORY & PRIMED FOR RESURRECTION

Fair Value:US$4039.0% undervalued

15 followersusers have followed this narrative

0 commentsusers have commented on this narrative

3 likesusers have liked this narrative

DO

Double_Bubbler on Vertical Aerospace ·

Why Vertical Aerospace (NYSE: EVTL) is Worth Possibly Over 13x its Current Price

Fair Value:US$6087.9% undervalued

19 followersusers have followed this narrative

1 commentusers have commented on this narrative

13 likesusers have liked this narrative

TI

TickerTickle on Oracle ·

The Quiet Giant That Became AI’s Power Grid

Fair Value:US$389.8143.2% undervalued

31 followersusers have followed this narrative

2 commentsusers have commented on this narrative

7 likesusers have liked this narrative

Recently Updated Narratives

LE

lexdrew1 on GE Vernova ·

GE Vernova revenue will grow by 13% with a future PE of 64.7x

Fair Value:US$824.5724.2% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

GI

Gil263 on Butterfly Network ·

A buy recommendation

Fair Value:US$1.872.2% overvalued

2 followersusers have followed this narrative

1 commentusers have commented on this narrative

0 likesusers have liked this narrative

OP

OpenHorizons on Channel Vas Investments ·

Growing between 25-50% for the next 3-5 years

Fair Value:R12.1157.3% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

118 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3926.1% undervalued

963 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8685.8% undervalued

76 followersusers have followed this narrative

8 commentsusers have commented on this narrative

21 likesusers have liked this narrative