Advertisement

- United States

- /

- Consumer Finance

- /

- NYSE:LC

LendingClub (LC) Is Down 5.0% After Authorizing $100 Million Share Buyback and Wellington Stake Increase

Simply Wall St

Reviewed by Sasha Jovanovic

- LendingClub Corporation announced in early November 2025 that it had authorized a share repurchase program of up to US$100 million, effective until December 31, 2026.

- An interesting aspect of this development is Wellington Management Group LLP's substantial increase in its stake, suggesting strong institutional interest following the buyback authorization.

- We'll explore how the new share repurchase program may influence LendingClub's earnings outlook and investor sentiment moving forward.

These 13 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

LendingClub Investment Narrative Recap

To be a LendingClub shareholder today is to believe in the company’s ability to ride ongoing demand for digital-first lending, leveraging innovation in data and AI-driven risk models. While the US$100 million share repurchase program grabs headlines, its short-term impact on the main catalyst, continued product adoption and origination growth, may be modest, with competition and credit cycle risks looming as the larger concerns for near-term earnings volatility.

Of all recent announcements, the buyback program stands out as most relevant to investor sentiment, especially paired with Wellington Management Group’s expanded stake. This institutional involvement and commitment of capital could offer some reassurance amid ongoing sector risks, though it does not change the company’s dependence on the personal loans segment, nor its exposure to shifting consumer credit trends.

However, it's important to balance this optimism against the possibility that rising competition and new fintech entrants could amplify margin pressure and create challenges that investors should be aware of if...

Read the full narrative on LendingClub (it's free!)

LendingClub's outlook sees revenues of $1.3 billion and earnings of $269.5 million by 2028. This reflects a 0.5% annual revenue decline and a $195.5 million increase in earnings from the current $74.0 million.

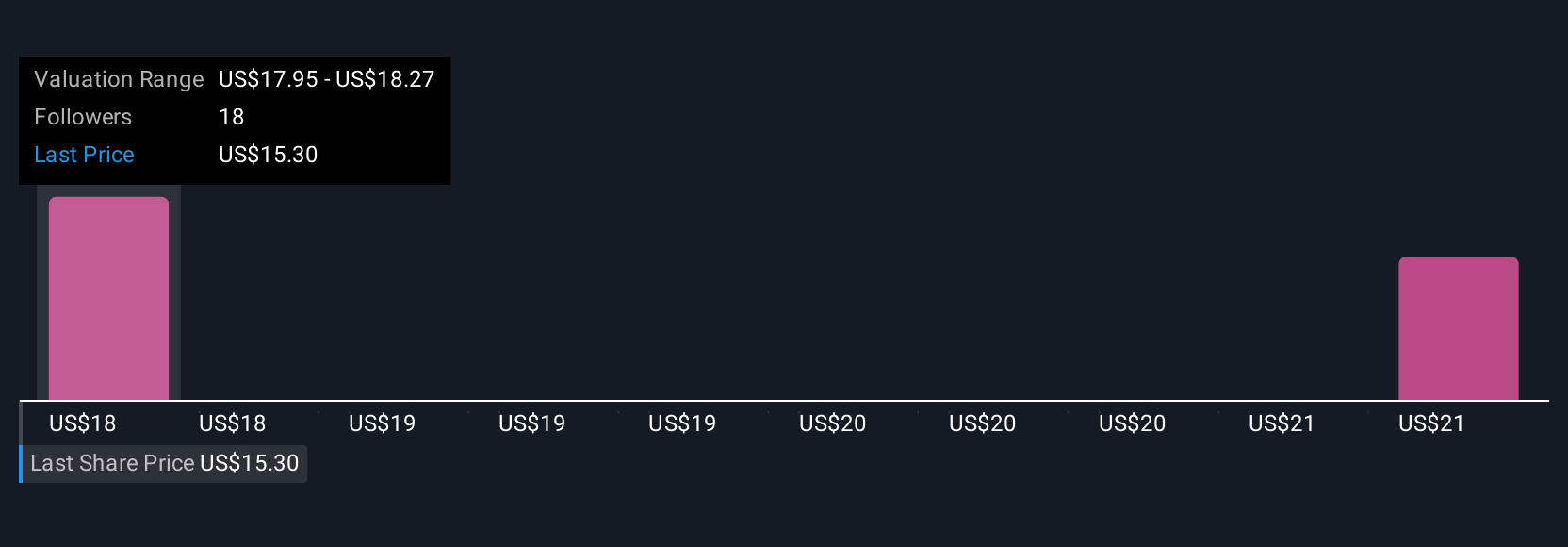

Uncover how LendingClub's forecasts yield a $21.91 fair value, a 27% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members offered two fair value estimates for LendingClub, ranging from US$21.91 to US$28.55 per share. As product innovation remains a key catalyst, your outlook could differ widely based on assumptions around future growth and market share, compare your view on these drivers with multiple perspectives.

Explore 2 other fair value estimates on LendingClub - why the stock might be worth as much as 66% more than the current price!

Build Your Own LendingClub Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your LendingClub research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

- Our free LendingClub research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate LendingClub's overall financial health at a glance.

Seeking Other Investments?

Early movers are already taking notice. See the stocks they're targeting before they've flown the coop:

- Uncover the next big thing with financially sound penny stocks that balance risk and reward.

- Rare earth metals are the new gold rush. Find out which 37 stocks are leading the charge.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:LC

LendingClub

Operates as a bank holding company, that provides range of financial products and services in the United States.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor