Advertisement

- United States

- /

- Capital Markets

- /

- NYSE:HLI

Will Houlihan Lokey's (HLI) New London Hire Signal a Shift in European Growth Ambitions?

Simply Wall St

Reviewed by Sasha Jovanovic

- On November 12, 2025, Houlihan Lokey announced the appointment of Neil Price as Managing Director in its Financial Sponsors Group, based in London, to expand client relationships in the U.K. and across Europe.

- This hire marks another step in Houlihan Lokey’s ongoing expansion of its European sponsor advisory business, following the recent addition of Martin Rezaie in Germany.

- We'll examine how Neil Price’s addition could impact Houlihan Lokey’s efforts to strengthen sponsor coverage and international growth plans.

AI is about to change healthcare. These 30 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

Houlihan Lokey Investment Narrative Recap

To believe in Houlihan Lokey, you need to trust that ongoing demand for advisory expertise and cross-border deal flow will drive consistent revenue growth, while successful senior-level hires like Neil Price help deepen client networks. Although building out European sponsor coverage is positive, the main catalyst for near-term performance remains a rebound in global M&A volumes; the biggest risk is persistent underperformance in EMEA deal activity, which this appointment may only partly address.

Of the recent announcements, the November 10th appointment of Seran Ahmetrasit as Head of Infrastructure Debt Advisory in Europe stands out as particularly relevant. This move, alongside Neil Price’s hire, illustrates Houlihan Lokey’s continued focus on expanding sector expertise and relationships in European markets, key to capturing opportunities if deal growth accelerates.

However, if deal volumes in EMEA stay muted, even the most experienced hires may not be enough to...

Read the full narrative on Houlihan Lokey (it's free!)

Houlihan Lokey's narrative projects $3.5 billion in revenue and $654.6 million in earnings by 2028. This requires 12.5% yearly revenue growth and a $246.3 million earnings increase from current earnings of $408.3 million.

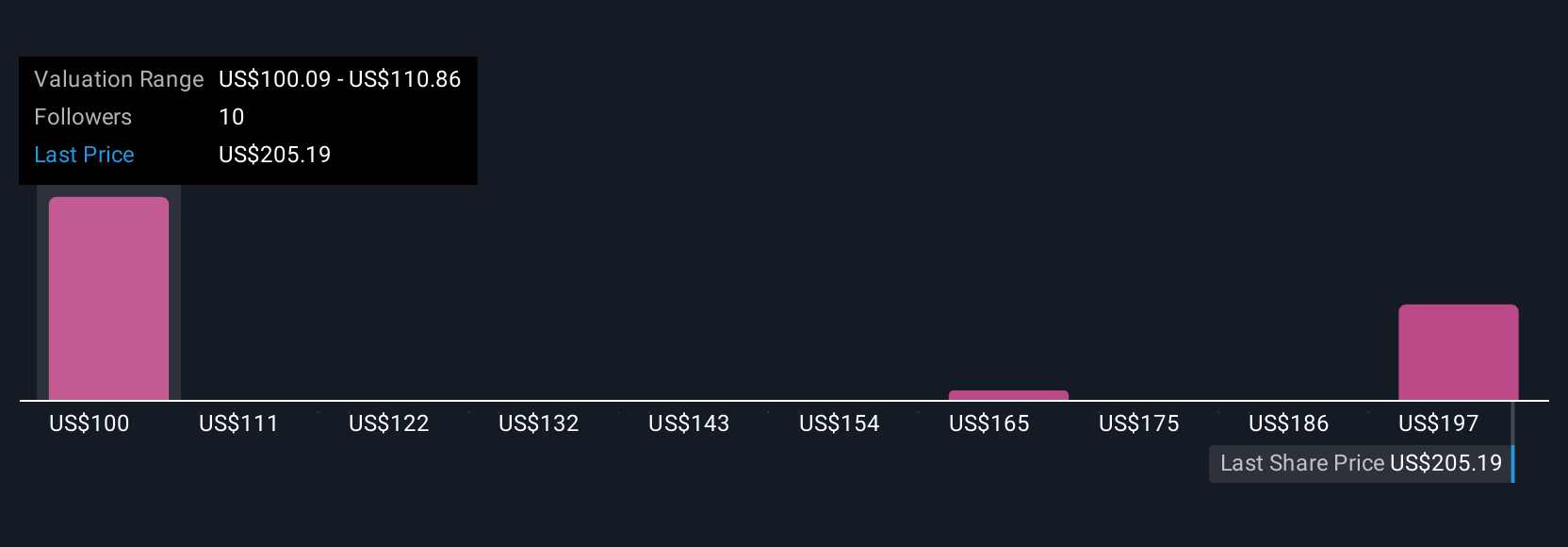

Uncover how Houlihan Lokey's forecasts yield a $210.86 fair value, a 22% upside to its current price.

Exploring Other Perspectives

Simply Wall St Community members produced three fair value estimates for Houlihan Lokey, ranging from US$99.05 to US$210.86, highlighting sharply different views. With recent senior hiring, the risk that underperformance in EMEA could limit earnings growth remains a theme worth watching as you compare these perspectives.

Explore 3 other fair value estimates on Houlihan Lokey - why the stock might be worth as much as 22% more than the current price!

Build Your Own Houlihan Lokey Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Houlihan Lokey research is our analysis highlighting 3 key rewards that could impact your investment decision.

- Our free Houlihan Lokey research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Houlihan Lokey's overall financial health at a glance.

Ready To Venture Into Other Investment Styles?

Right now could be the best entry point. These picks are fresh from our daily scans. Don't delay:

- Find companies with promising cash flow potential yet trading below their fair value.

- We've found 14 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- Trump has pledged to "unleash" American oil and gas and these 22 US stocks have developments that are poised to benefit.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Houlihan Lokey might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HLI

Houlihan Lokey

An investment banking company, provides merger and acquisition (M&A), capital market, financial restructurings and liability management, and financial and valuation advisory services worldwide.

Flawless balance sheet with solid track record and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.6% undervalued

TI

Community Contributor

Recently Updated Narratives

MA

MarkoVT on COVER ·

Q3 Outlook modestly optimistic

Fair Value:JP¥1.65k2.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

BL

BlackGoat on Alphabet ·

Alphabet: The Under-appreciated Compounder Hiding in Plain Sight

Fair Value:US$324.481.3% undervalued

80 followersusers have followed this narrative

3 commentsusers have commented on this narrative

1 likeusers have liked this narrative

BE

Bejgal on MINISO Group Holding ·

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value:US$26.6926.7% undervalued

46 followersusers have followed this narrative

3 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

91 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

927 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative