Advertisement

- United States

- /

- Capital Markets

- /

- NYSE:EVR

Assessing Evercore (EVR) Valuation After Recent Share Pullback And Mixed Earnings Multiples

Recent share performance and business snapshot

With no single event driving headlines today, Evercore (EVR) has been getting attention after a recent share pullback as investors reassess the independent advisory firm's role within diversified financials.

The stock's last close was US$319.17, with a return of about 21% over the past year and a loss of roughly 9% year to date. Over the past 3 months, the return sits near 4%, while the past month shows an approximate 13% decline.

See our latest analysis for Evercore.

Recent trading has been weak, with a 1 month share price return of roughly a 13% decline and a year to date share price return of about a 9% decline. This comes even as the 1 year total shareholder return sits near 21% and the 5 year total shareholder return is around 200%. Longer term momentum therefore still contrasts with the latest pullback as investors reassess growth prospects and risks around the current US$319.17 share price.

If this shift in sentiment has you looking beyond a single name, it could be a good time to broaden your search with our 23 top founder-led companies and see what else stands out.

With EVR trading around US$319.17 after a 13% 1-month pullback, yet still carrying a roughly 21% 1-year total return and a value score of 4, is this a reset that offers upside, or is the market already baking in future growth?

Most Popular Narrative: 9.7% Undervalued

Evercore's most followed narrative pegs fair value around $354, a step above the last close at $319.17, and builds that gap around deal making and margin power.

The ongoing globalization of capital markets and an accelerating trend in cross border M&A activity are providing an increasingly fertile environment for independent, conflict free advisors like Evercore. The firm's continued expansion into key international markets, as evidenced by new offices and hiring in EMEA (France, Spain, Italy, Dubai, UK), positions it to capture an increasing share of growing advisory fee pools and drive top line revenue over the long term.

Curious what sits behind that valuation gap? The narrative leans on a blend of deal volume assumptions, margin improvement, and a future earnings multiple that is anything but casual.

Result: Fair Value of $353.56 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, the story could change quickly if M&A activity stays subdued for longer than analysts expect, or if high compensation costs keep squeezing margins.

Find out about the key risks to this Evercore narrative.

Another angle on valuation

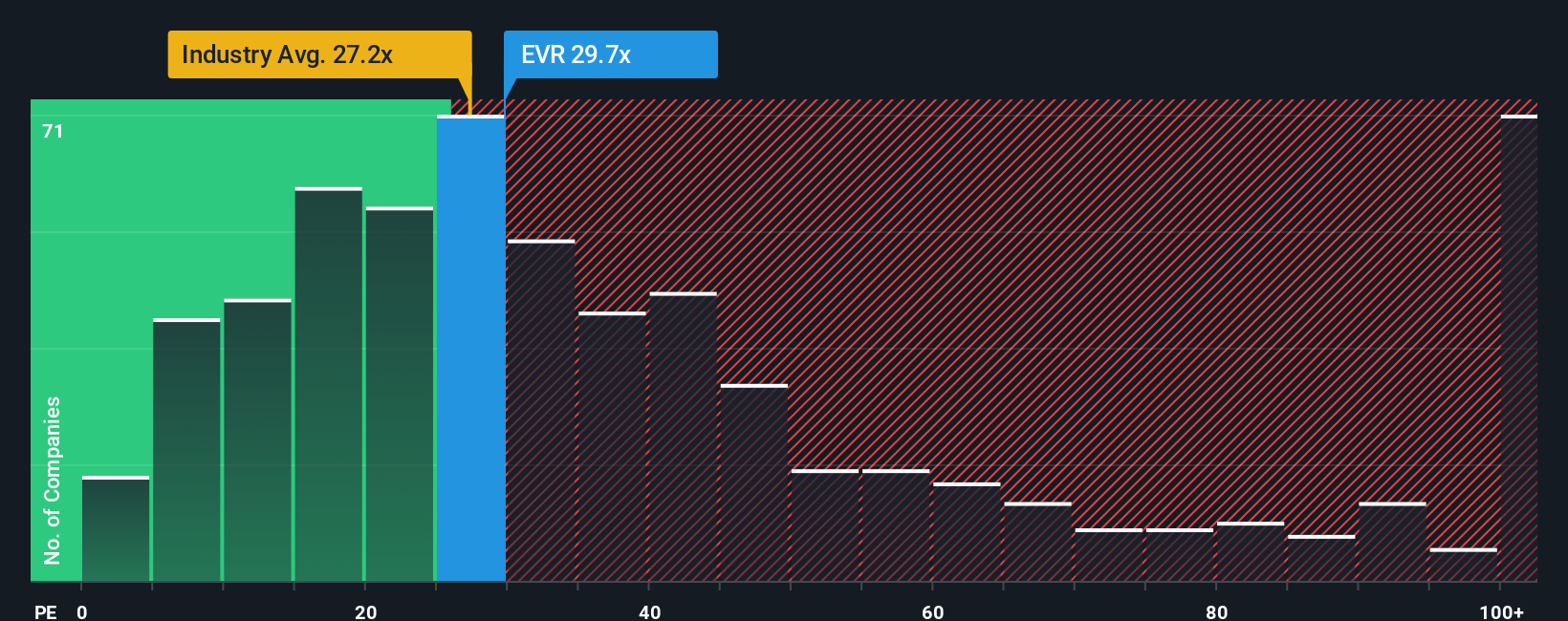

That fair value of about $354 suggests upside, but the simple P/E picture is less generous. EVR trades at 20.9x earnings, richer than its 17.4x fair ratio estimate and peer average of 18.2x, even if it sits below the broader US Capital Markets average of 22.9x. Is the market already paying up for quality here, or is this just the entry price for a strong franchise?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Evercore Narrative

If parts of this story do not quite fit your view, or you prefer to lean on your own research and assumptions, you can pull the same data, test your thesis, and build a customised Evercore narrative in just a few minutes, then Do it your way.

A great starting point for your Evercore research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Ready for more investment ideas?

If you are weighing up what to do next after looking at Evercore, now is the moment to widen your watchlist and compare fresh opportunities side by side.

- Spot potential value opportunities early by scanning our 55 high quality undervalued stocks, which is based on strong fundamentals and sensible pricing metrics.

- Prioritise resilience by checking companies with robust finances through the solid balance sheet and fundamentals stocks screener (45 results) and see which names keep their footing when conditions get tougher.

- Put your cash to work with income focused opportunities using the 16 dividend fortresses and see which companies currently offer yields above 5%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Evercore might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:EVR

Evercore

Operates as an independent investment banking firm in the Americas, Europe, Middle East, Africa, and Asia-Pacific.

Solid track record, good value and pays a dividend.

Similar Companies

Market Insights

Advertisement

Weekly Picks

VA

valuebull on Eva Live ·

Is this the AI replacing marketing professionals?

Fair Value:US$7.4342.5% undervalued

31 followersusers have followed this narrative

0 commentsusers have commented on this narrative

7 likesusers have liked this narrative

ZA

ZayaanS on Pro Medicus ·

Pro Medicus: The Market Is Confusing a Lumpy Quarter With a Broken Business

Fair Value:AU$196.7829.0% undervalued

32 followersusers have followed this narrative

6 commentsusers have commented on this narrative

19 likesusers have liked this narrative

ST

SteveGruber on Warner Bros. Discovery ·

The Rising Deal Risk That Helped Sink Netflix’s $72 Billion Bid for Warner Bros. Discovery

Fair Value:US$18.1752.7% overvalued

5 followersusers have followed this narrative

1 commentusers have commented on this narrative

3 likesusers have liked this narrative

PD

pdixit1 on Vertiv Holdings Co ·

The Infrastructure AI Cannot Be Built Without

Fair Value:US$408.6435.3% undervalued

35 followersusers have followed this narrative

3 commentsusers have commented on this narrative

17 likesusers have liked this narrative

Recently Updated Narratives

MA

MarkoVT on ANYCOLOR ·

Near zero debt, Japan centric focus provides future growth

Fair Value:JP¥6.92k40.3% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JU

JuanVargas on Promigas E.S.P ·

Promigas E.S.P looks to a promising future with 35% revenue growth

Fair Value:Col$13.26k51.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

VE

Vestra on Kratos Defense & Security Solutions ·

Kratos Defense & Security Solutions (KTOS): Scaling "Attritable" Dominance in a New Era of Aerial Conflict.

Fair Value:US$11821.6% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

KA

kabz2342 on Nu Holdings ·

Nu holdings will continue to disrupt the South American banking market

Fair Value:US$64.377.2% undervalued

51 followersusers have followed this narrative

3 commentsusers have commented on this narrative

27 likesusers have liked this narrative

AN

AnalystConsensusTarget on Microsoft ·

Analyst Commentary Highlights Microsoft AI Momentum and Upward Valuation Amid Growth and Competitive Risks

Fair Value:US$59631.3% undervalued

1305 followersusers have followed this narrative

2 commentsusers have commented on this narrative

10 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$253.0227.8% undervalued

1102 followersusers have followed this narrative

7 commentsusers have commented on this narrative

34 likesusers have liked this narrative