Advertisement

- United States

- /

- Consumer Finance

- /

- NYSE:ENVA

Persistent Small Business Optimism and Digital Lending Trends Might Change The Case For Investing In Enova International (ENVA)

Simply Wall St

Reviewed by Sasha Jovanovic

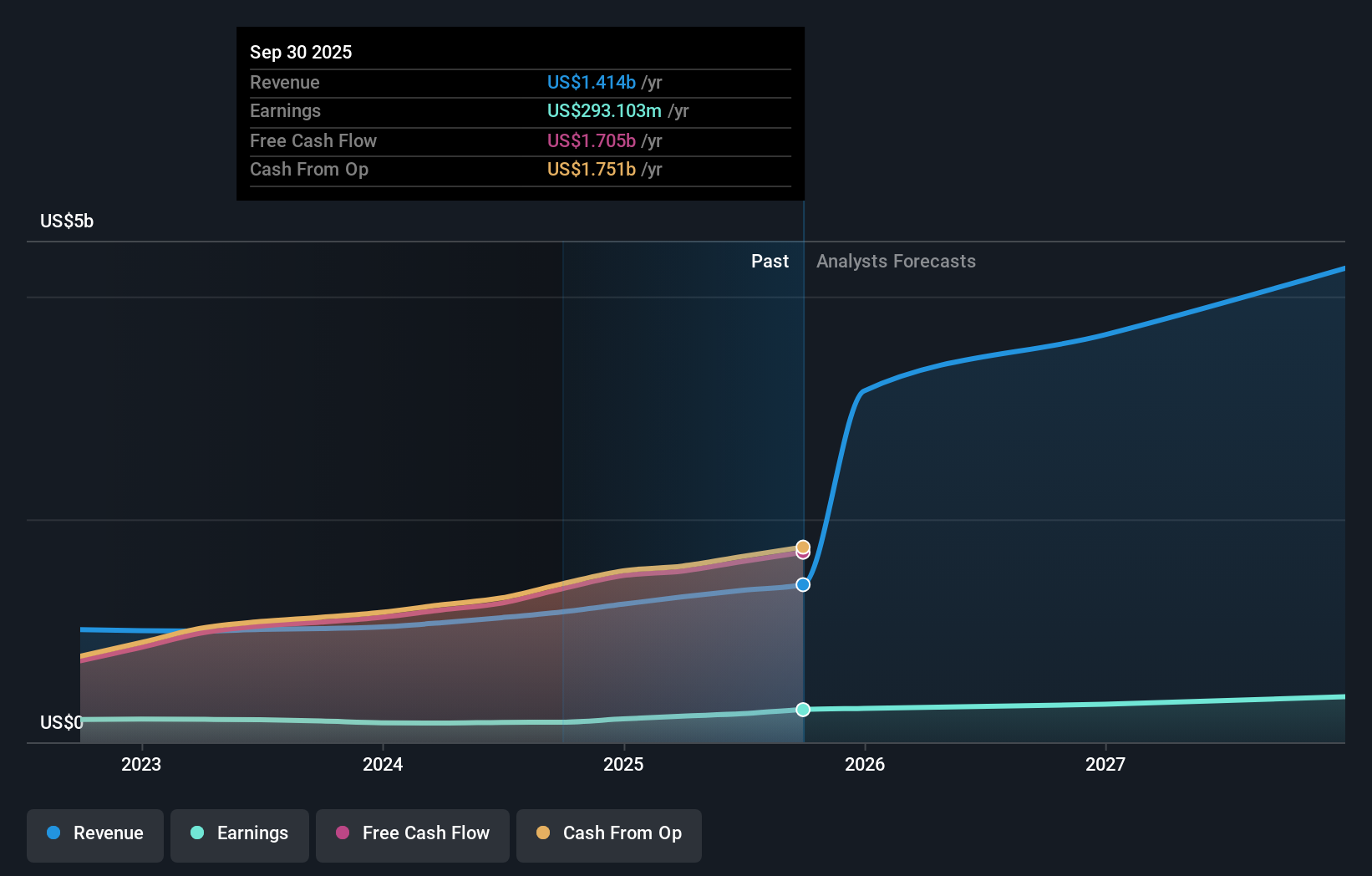

- Enova International announced that it reported its third quarter 2025 financial results after market close on October 23, 2025, accompanied by a scheduled earnings call.

- Amid persistent small business optimism and increased adoption of fintech lending, a majority of borrowers are turning to platforms like Enova’s OnDeck for working capital, highlighting shifts in client behavior toward digital financial solutions.

- We'll examine how heightened market anticipation around Enova’s Q3 earnings and slowing projected revenue growth influence its investment thesis.

These 15 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

Enova International Investment Narrative Recap

To be a shareholder in Enova International, you need confidence in the ongoing shift toward digital lending among small businesses and consumers and Enova’s ability to maintain its tech edge in underwriting. The scheduled Q3 results and earnings call reinforce market focus on near-term revenue growth, but with analysts already projecting a slowdown and the company twice missing estimates in the last two years, the most important catalyst will be Enova’s delivery on guidance, while exposure to credit quality remains the biggest risk. Overall, this earnings update does not materially change either.

The upcoming Q3 financial release is the most relevant recent event, as it brings new data against the backdrop of high small business optimism and growing fintech adoption. Enova’s position as a leading non-bank lender puts the spotlight on its ability to capture digital loan demand, but how the reported results align with anticipated growth figures may play a key role in near-term sentiment.

By contrast, investors should be aware that even as demand moves online, wide swings in loan losses can still impact...

Read the full narrative on Enova International (it's free!)

Enova International's narrative projects $5.7 billion in revenue and $426.8 million in earnings by 2028. This requires 60.7% yearly revenue growth and a $170.6 million earnings increase from the current $256.2 million.

Uncover how Enova International's forecasts yield a $131.12 fair value, a 15% upside to its current price.

Exploring Other Perspectives

The Simply Wall St Community contributed four fair value estimates for Enova International ranging from US$64.42 to US$467.73 per share. When weighing this diversity of opinion, remember that fast-growing digital adoption could fuel further earnings potential, but opinions differ greatly, explore these viewpoints closely.

Explore 4 other fair value estimates on Enova International - why the stock might be worth over 4x more than the current price!

Build Your Own Enova International Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Enova International research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Enova International research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Enova International's overall financial health at a glance.

Interested In Other Possibilities?

Our top stock finds are flying under the radar-for now. Get in early:

- Find companies with promising cash flow potential yet trading below their fair value.

- This technology could replace computers: discover 27 stocks that are working to make quantum computing a reality.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 26 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Enova International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:ENVA

Enova International

A technology and analytics company, provides online financial services in the United States, Brazil, and internationally.

Reasonable growth potential with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor