Advertisement

- United States

- /

- Capital Markets

- /

- NYSE:CNS

Assessing Cohen & Steers After a 37% Share Price Drop This Year

Simply Wall St

Reviewed by Bailey Pemberton

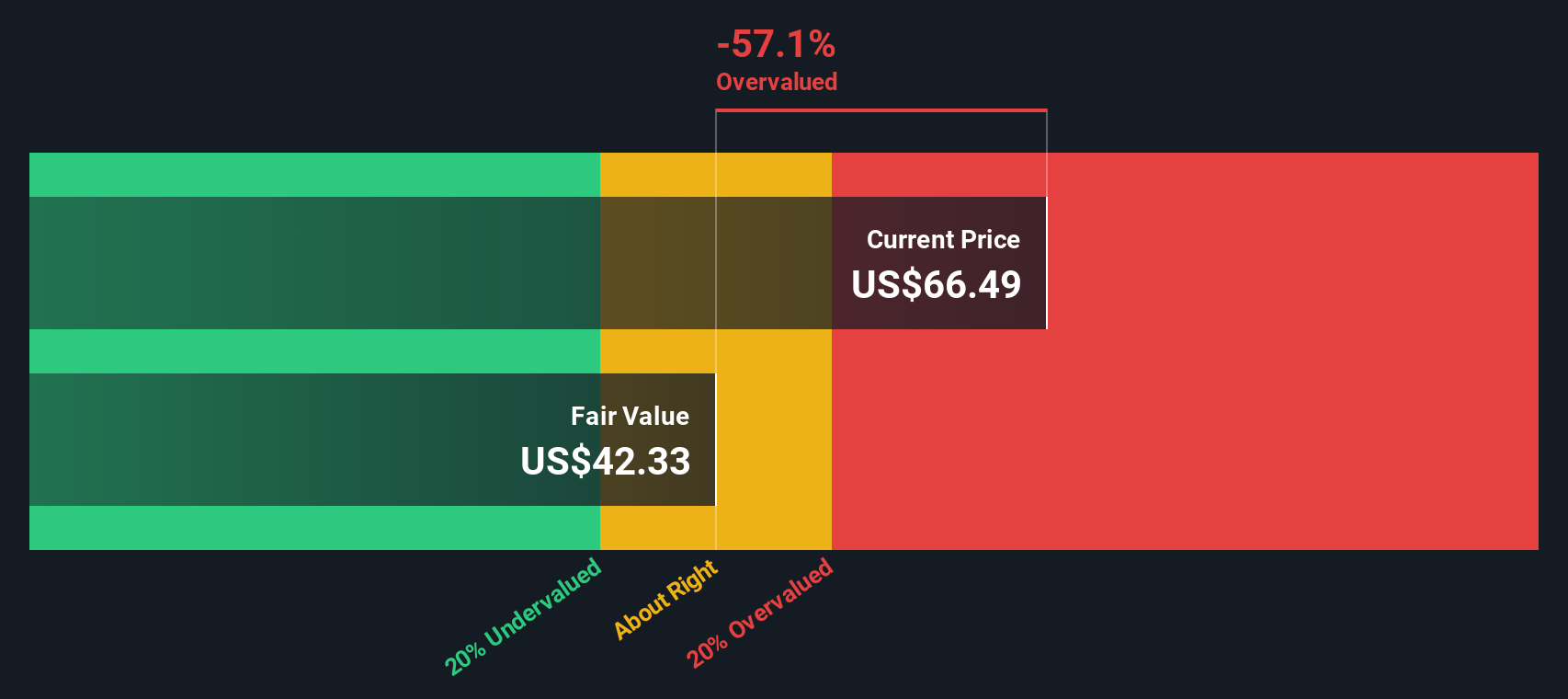

- Wondering if now is the right time to buy, sell, or hold Cohen & Steers? You are not alone. Many investors are watching its valuation after recent moves.

- Over the past year, Cohen & Steers' share price has taken a hit, dropping 37.1%, with a year-to-date slide of 30.2%. There has been a modest 3.9% bounce in the past week, but recent volatility hints at shifting sentiment.

- Much of this movement is influenced by broader shifts in market confidence and sector sentiment, as investors weigh economic signals and changing risk appetites. Financial sector news around interest rates and asset management trends have added both challenges and opportunities for companies like Cohen & Steers.

- According to our valuation checks, Cohen & Steers scores just 1 out of 6 for being undervalued. We will dive into the various valuation methods investors use, but stick around. There is a smarter way to assess value that you will want to see at the end of this article.

Cohen & Steers scores just 1/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: Cohen & Steers Excess Returns Analysis

The Excess Returns model evaluates a company’s ability to generate profits above its cost of equity. This approach focuses on how efficiently Cohen & Steers turns its invested capital into shareholder value. It highlights the difference between what the business earns and what equity holders require as a return for their investment.

For Cohen & Steers, the key metrics are:

- Book Value: $10.79 per share

- Stable EPS: $2.35 per share (Source: Median Return on Equity from the past 5 years.)

- Cost of Equity: $0.64 per share

- Excess Return: $1.72 per share

- Average Return on Equity: 30.34%

- Stable Book Value: $7.76 per share (Source: Median Book Value from the past 5 years.)

By estimating the future profitability and taking into account the company’s cost of equity, the model calculates an intrinsic value per share of $42.61. Currently, the stock trades at a substantial premium to this estimate, making it 49.6% overvalued according to this valuation approach.

The implication is clear. Even after accounting for robust returns on equity, the current market price appears expensive using this method.

Result: OVERVALUED

Our Excess Returns analysis suggests Cohen & Steers may be overvalued by 49.6%. Discover 923 undervalued stocks or create your own screener to find better value opportunities.

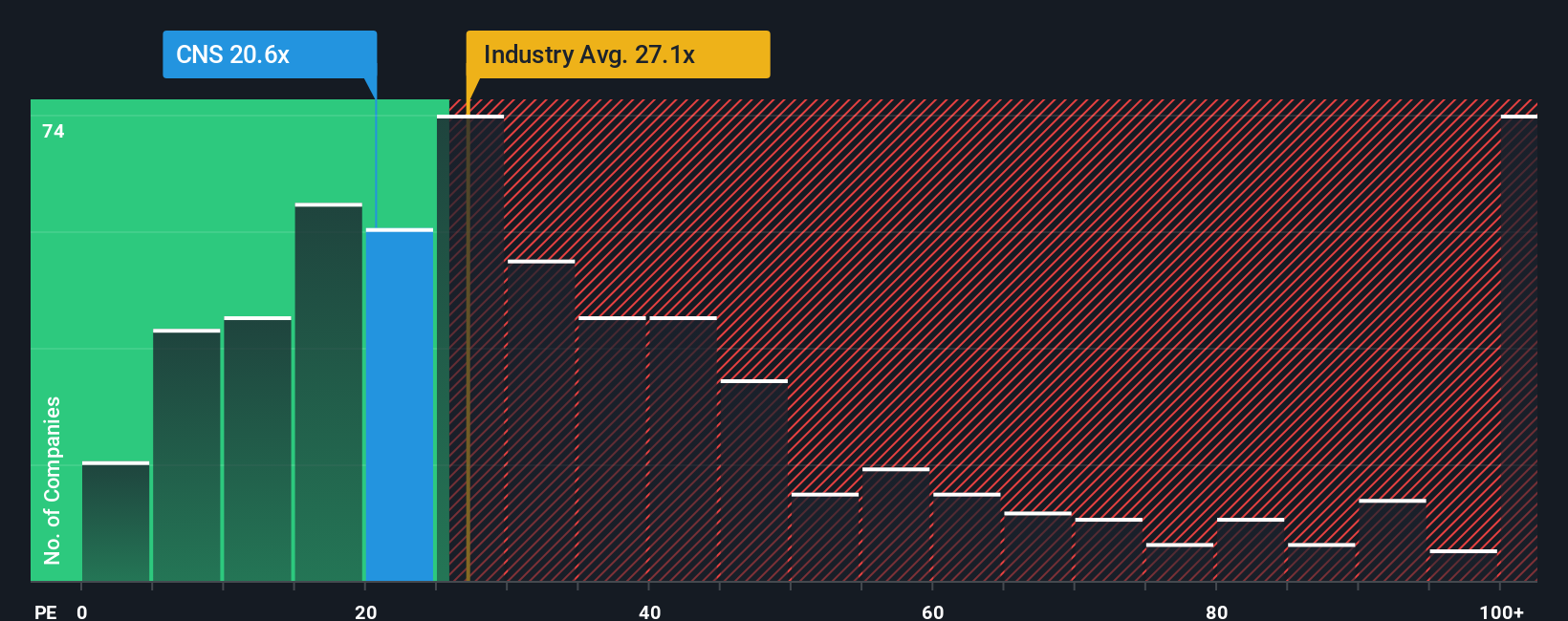

Approach 2: Cohen & Steers Price vs Earnings

The Price-to-Earnings (PE) ratio is a widely used valuation metric for profitable companies like Cohen & Steers because it connects a company’s current share price to its per-share earnings. This ratio is particularly meaningful for businesses with consistent profitability, offering investors a direct look at how much they are paying for each dollar of earnings generated.

It is important to note that a company’s “normal” or “fair” PE ratio often depends on its expected earnings growth and perceived risk. Companies with higher growth prospects or lower risk profiles can often justify a higher PE ratio, while slower growth or higher uncertainty typically means a lower one is warranted.

Cohen & Steers is currently trading on a PE of 19.8x. For context, its peer group averages a PE of 10.1x, while the capital markets industry sits higher at 23.6x. Benchmarking against these groups gives a standard reference point for valuation, but not the full picture.

This is where Simply Wall St’s proprietary “Fair Ratio” comes in, calculated at 15.0x for Cohen & Steers. This custom benchmark accounts for variables such as the company’s earnings growth, profit margin, risk, industry and market cap. It is better tailored than a simple comparison to peers or industry averages. It provides a holistic assessment that reflects where this particular stock should trade, given its unique characteristics.

When we compare Cohen & Steers’ actual PE of 19.8x to its Fair Ratio of 15.0x, the stock screens as overvalued on this metric. The gap suggests the market is currently pricing in more growth or less risk than may be justified by the fundamentals.

Result: OVERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1439 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Cohen & Steers Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let’s introduce you to Narratives. A Narrative is your story about a company’s future, providing the “why” behind your assumptions for fair value, projected revenue, future margins, and growth. Narratives connect the facts you know and the forecasts you believe in, turning them into a unique fair value that you can compare to today’s price.

On Simply Wall St’s Community page, Narratives make it easy for anyone to express their view and instantly see how different scenarios impact whether a stock looks cheap or expensive. This tool is used by millions of investors. When prices shift or new news or earnings are released, these Narratives update dynamically to keep your investment thesis relevant and data-driven.

Narratives help you decide if it is time to buy, sell, or hold by comparing each fair value estimate, grounded in your own outlook, against the current share price. For example, some investors are optimistic for Cohen & Steers and see fair value as high as $80 due to expanding active ETFs and global business lines. Others are more cautious, assigning a fair value closer to $66 because of margin pressure and risks from passive investing trends.

Do you think there's more to the story for Cohen & Steers? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:CNS

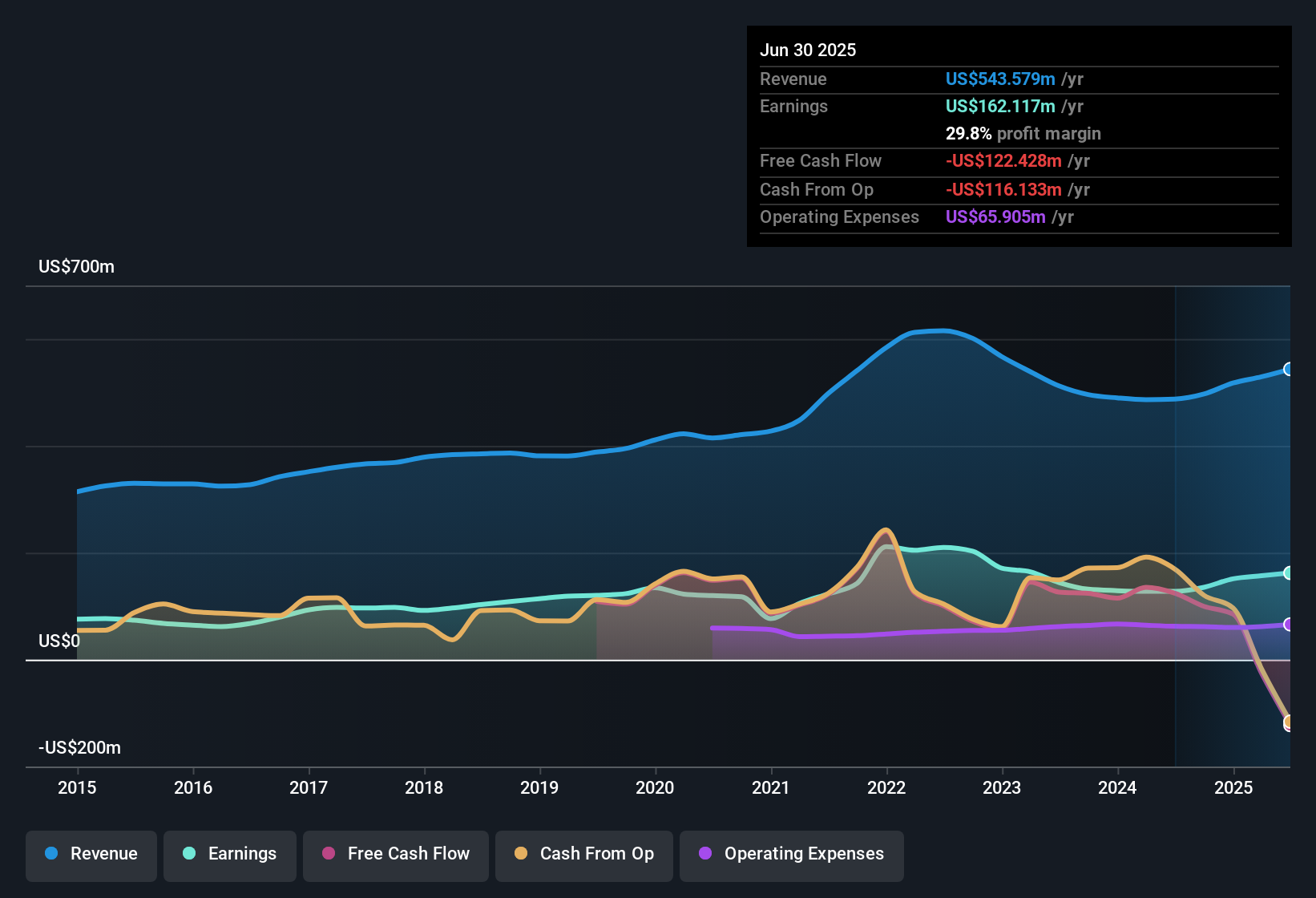

Flawless balance sheet with solid track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on ANYCOLOR ·

Near zero debt, Japan centric focus provides future growth

Fair Value:JP¥7.61k15.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative