American Express (AXP) recently saw its stock price edge slightly higher over the past week, gaining about 6%. Some investors are reviewing its performance to see whether the current valuation reflects the company’s growth potential and recent trends.

After a modest but steady week, American Express’s share price has gained 22% year-to-date, reflecting a strong tailwind as investors respond to the company’s healthy financial growth and a relatively robust risk profile. The momentum is building, with an impressive 21% total shareholder return over the past year and a remarkable 139% total return across three years. This highlights sustained long-term outperformance.

With American Express’s substantial gains attracting attention, the key question is whether there is still room for further upside or if the impressive growth prospects are already fully reflected in the current share price. Is there a real buying opportunity, or has the market already priced in what comes next?

Advertisement

Most Popular Narrative: 3.7% Overvalued

According to the most widely followed narrative, American Express's fair value estimate trails its last close price, keeping investors on edge as optimism meets heightened expectations.

Double-digit international growth, ongoing investments in global product innovation, and expanding merchant acceptance tap into the expanding global middle class and increased digital payment adoption. These trends are expected to raise transaction volumes and support both top-line growth and long-term earnings diversification.

Curious what powers this ambitious valuation? The narrative relies on bold global growth assumptions and impressive profit margins that position American Express in rare territory. This perspective anticipates a future multiple beyond the industry norm. Want to see exactly what drives these projections? Jump into the full narrative to unlock all the numbers and logic behind this fair value.

However, shifting consumer preferences toward digital wallets and intensifying competition in premium cards could challenge American Express’s growth outlook in the coming years.

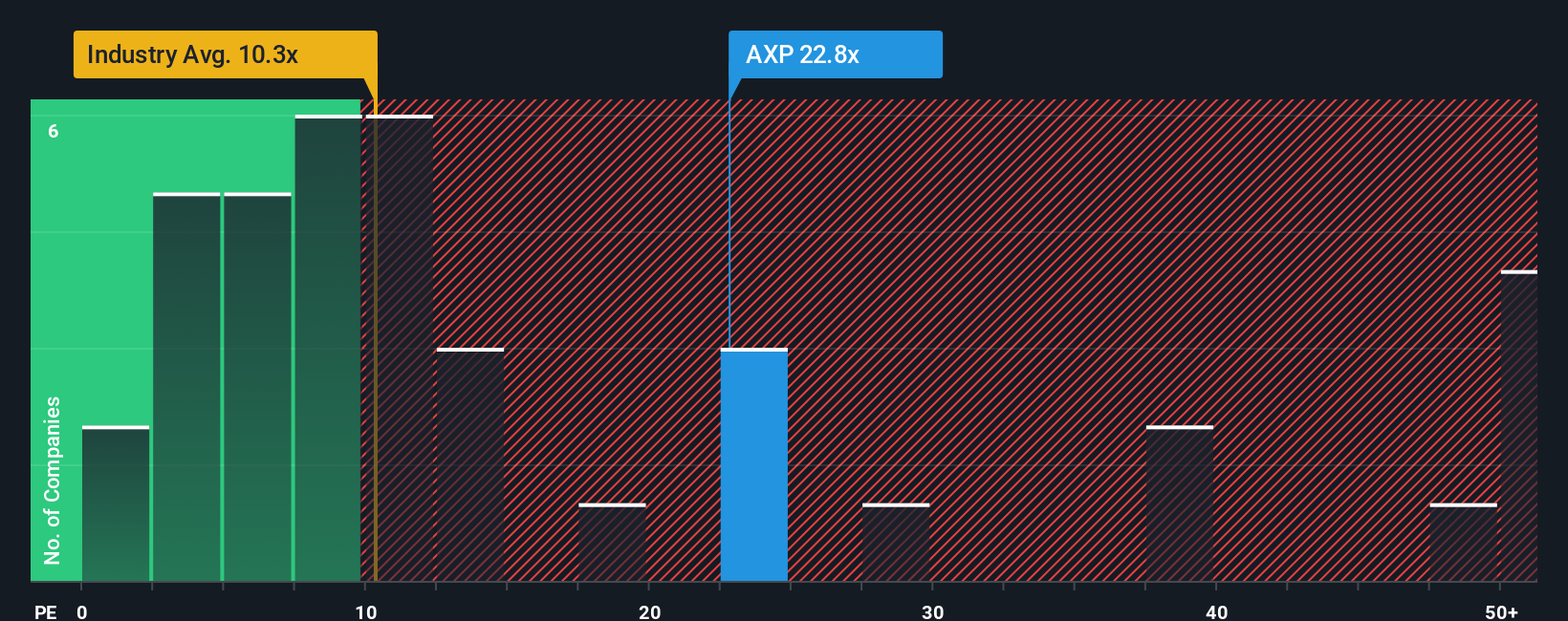

While the dominant narrative points to American Express trading above its estimated fair value, comparing its price-to-earnings ratio of 24.1x to peers and the Consumer Finance industry average of 10.2x shows a clear premium. Even when weighed against its fair ratio of 19.9x, the stock appears expensive, suggesting valuation risk if sentiment shifts. Could strong fundamentals justify this premium, or are expectations simply running too far ahead?

If you want a different take or prefer doing your own digging, it's easy to dive in and shape your own view with fresh data. Do it your way

A great starting point for your American Express research is our analysis highlighting 2 key rewards and 1 important warning sign that could impact your investment decision.

Looking for More Smart Investment Ideas?

Don’t let opportunity pass you by. Expand your horizons and seize new trends by checking out these distinctive themes on Simply Wall Street’s screener:

Stay ahead of emerging tech by backing innovation through these 25 AI penny stocks, where artificial intelligence is redefining the investment landscape.

Capitalize on game-changing advances by seeking these 27 quantum computing stocks poised to transform industries and reward forward-thinking investors.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks

Operates as integrated payments company in the United States, Europe, the Middle East and Africa, the Asia Pacific, Australia, New Zealand, Latin America, Canada, the Caribbean, and Internationally.