Advertisement

- United States

- /

- Diversified Financial

- /

- NasdaqGS:PYPL

Is PayPal Attractively Priced After 2024 Share Slump And Strong Excess Returns Outlook?

Simply Wall St

Reviewed by Bailey Pemberton

- If you are wondering whether PayPal Holdings is a bargain or a value trap at around $61 a share, you are not alone. This stock has become a classic case of expectations resetting faster than the narrative.

- Despite being a household name in digital payments, the stock is down 28.9% year to date and 31.1% over the last year. This has shifted how the market is pricing its growth and risk.

- Recent headlines have focused on PayPal's efforts to streamline its product lineup and sharpen its competitive edge in online checkout and digital wallets, while also pushing into newer initiatives like branded rewards and checkout experiences for merchants. These strategic moves help explain why some investors see the current share price as a reset, while others worry that competition from players like Apple and Block is compressing its long term growth story.

- On our checks, PayPal scores a solid 5/6 valuation score, suggesting the market may be undervaluing its cash flows and earnings power. However, traditional metrics only tell part of the story, so next we will unpack the different valuation approaches, before finishing with a more complete way to think about what PayPal is really worth.

Find out why PayPal Holdings's -31.1% return over the last year is lagging behind its peers.

Approach 1: PayPal Holdings Excess Returns Analysis

The Excess Returns model looks at how much value a company creates above the minimum return that equity investors demand. Instead of focusing on simple earnings multiples, it measures how efficiently PayPal turns its equity base into sustainable profits.

For PayPal, the starting Book Value is $21.46 per share, with a Stable EPS of $6.23 per share, based on weighted future Return on Equity estimates from 10 analysts. The implied Cost of Equity is $1.97 per share, so PayPal is expected to generate an Excess Return of $4.25 per share. That gap reflects an average Return on Equity of 24.45%, above the level investors require.

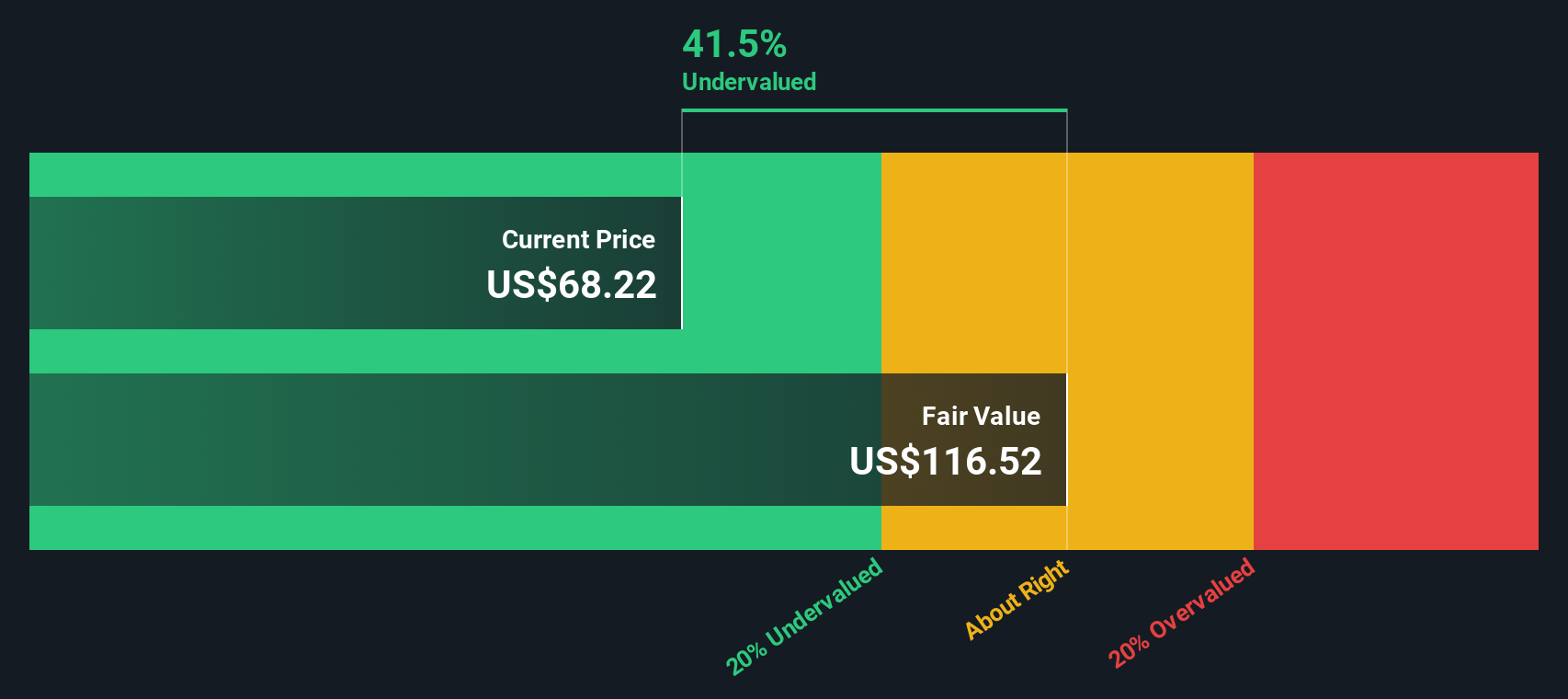

The model also assumes a Stable Book Value of $25.47 per share, drawn from estimates by 8 analysts, which supports continued reinvestment at high returns. Combining these inputs, the Excess Returns valuation points to an intrinsic value of about $120.32 per share, implying the stock is roughly 49.1% undervalued versus the current price around $61.

Result: UNDERVALUED

Our Excess Returns analysis suggests PayPal Holdings is undervalued by 49.1%. Track this in your watchlist or portfolio, or discover 919 more undervalued stocks based on cash flows.

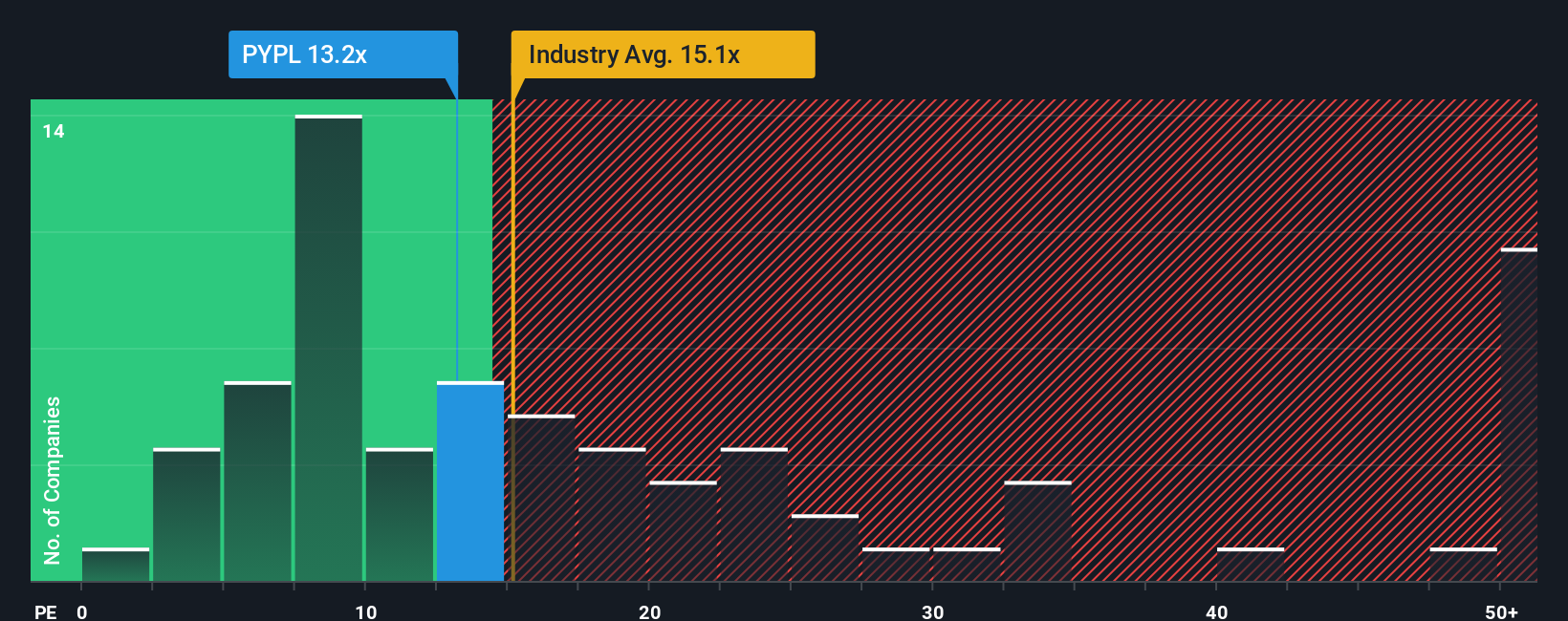

Approach 2: PayPal Holdings Price vs Earnings

For profitable, mature businesses like PayPal, the Price to Earnings (PE) ratio is often the cleanest way to gauge how much investors are willing to pay for each dollar of current earnings. It ties the valuation directly to the bottom line, which makes it especially useful when earnings are relatively stable and growing.

What counts as a fair PE depends on how fast earnings are expected to grow and how risky those earnings are. Higher growth and stronger competitive positioning can justify a higher multiple, while more uncertainty usually pulls it down. PayPal currently trades on about 11.65x earnings, below both the Diversified Financial industry average of roughly 13.74x and the broader peer group average of around 58.48x. This suggests the market is applying a discount.

Simply Wall St estimates a Fair Ratio of 17.97x for PayPal. This proprietary metric goes beyond simple peer or industry comparisons by adjusting for the company’s earnings growth profile, margins, risk factors, industry, and market cap. On that basis, PayPal’s current 11.65x multiple sits well below its Fair Ratio. This indicates the shares appear undervalued on an earnings basis.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1441 companies where insiders are betting big on explosive growth.

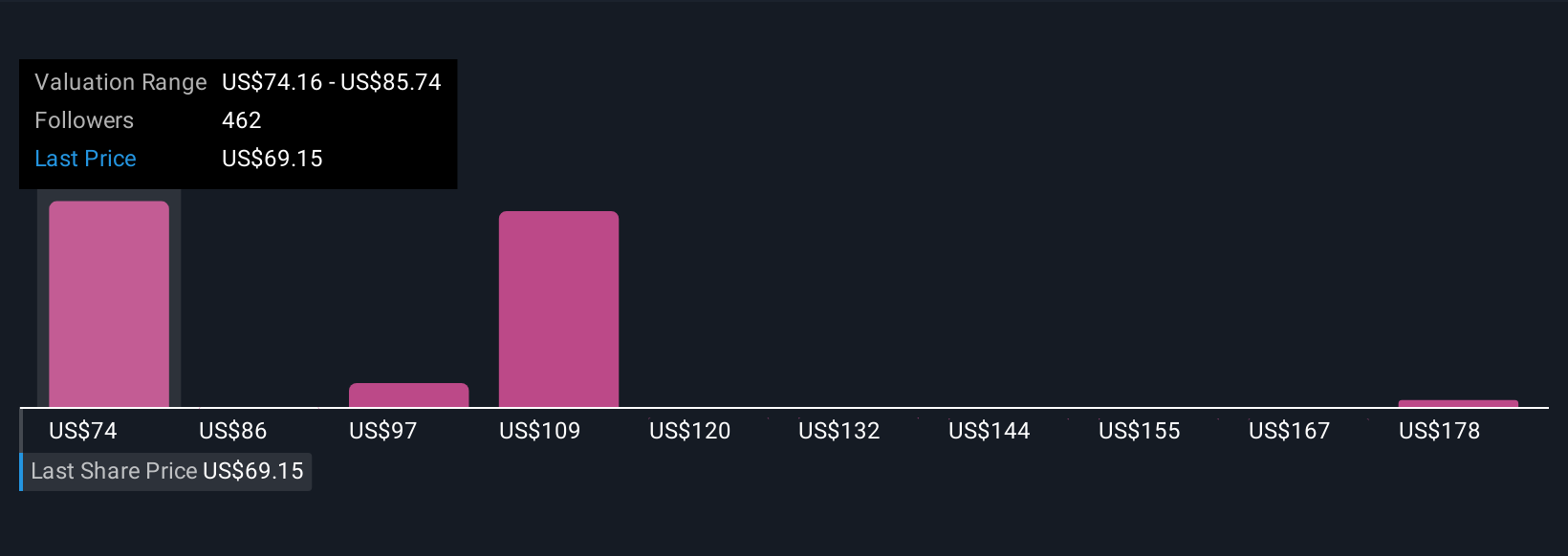

Upgrade Your Decision Making: Choose your PayPal Holdings Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let us introduce you to Narratives, which are simple stories that capture your view of a company and link it to a set of numbers like future revenue, earnings, margins, and a resulting fair value estimate. On Simply Wall St, Narratives live in the Community page and turn your perspective into a structured financial forecast, then compare that forecast-based Fair Value to today’s share Price so you can quickly see if a stock looks buyable, hold worthy, or ready to trim. Because Narratives are updated dynamically when new information comes in, such as PayPal’s earnings, product launches, or regulatory news, they stay aligned with the real world instead of going stale in a spreadsheet. For PayPal, for example, one investor Narrative might lean bullish with stronger growth, higher margins, and a fair value around $133 per share, while a more cautious Narrative might assume slower growth and a fair value closer to $82, and seeing where your own view sits between those live examples can help you decide on your next steps.

Do you think there's more to the story for PayPal Holdings? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:PYPL

PayPal Holdings

Operates a technology platform that enables digital payments for merchants and consumers worldwide.

Outstanding track record and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.4% undervalued

39 followersusers have followed this narrative

6 commentsusers have commented on this narrative

11 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$123.8% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$244.5% overvalued

6 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

FU

FundamentallySarcastic on Credit Corp Group ·

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Fair Value:AU$12.6411.8% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1918.1% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5190.0% overvalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.5% undervalued

114 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.3% undervalued

952 followersusers have followed this narrative

6 commentsusers have commented on this narrative

25 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3406.0% undervalued

147 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative