Advertisement

- United States

- /

- Diversified Financial

- /

- NasdaqGS:PYPL

Despite delivering investors losses of 44% over the past 3 years, PayPal Holdings (NASDAQ:PYPL) has been growing its earnings

PayPal Holdings, Inc. (NASDAQ:PYPL) shareholders should be happy to see the share price up 13% in the last quarter. But that doesn't help the fact that the three year return is less impressive. In fact, the share price is down 44% in the last three years, falling well short of the market return.

While the last three years has been tough for PayPal Holdings shareholders, this past week has shown signs of promise. So let's look at the longer term fundamentals and see if they've been the driver of the negative returns.

Check out our latest analysis for PayPal Holdings

To quote Buffett, 'Ships will sail around the world but the Flat Earth Society will flourish. There will continue to be wide discrepancies between price and value in the marketplace...' One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

Although the share price is down over three years, PayPal Holdings actually managed to grow EPS by 1.7% per year in that time. Given the share price reaction, one might suspect that EPS is not a good guide to the business performance during the period (perhaps due to a one-off loss or gain). Alternatively, growth expectations may have been unreasonable in the past.

It's pretty reasonable to suspect the market was previously to bullish on the stock, and has since moderated expectations. But it's possible a look at other metrics will be enlightening.

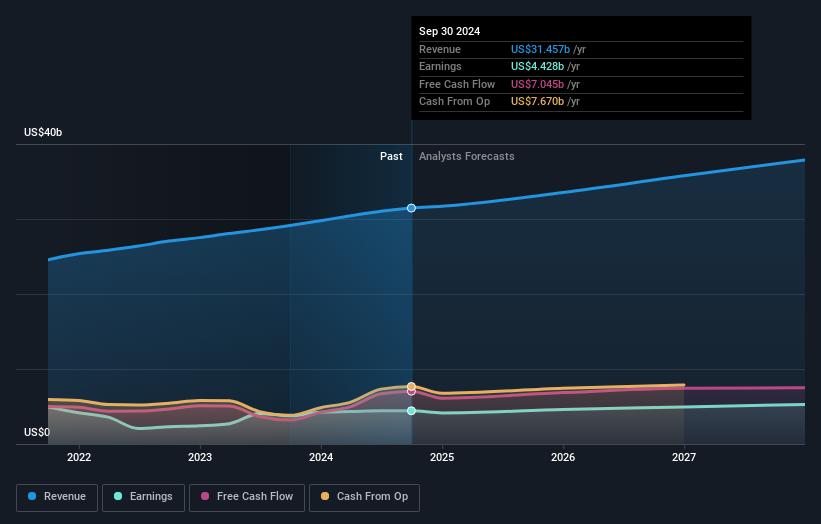

We note that, in three years, revenue has actually grown at a 8.1% annual rate, so that doesn't seem to be a reason to sell shares. This analysis is just perfunctory, but it might be worth researching PayPal Holdings more closely, as sometimes stocks fall unfairly. This could present an opportunity.

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

PayPal Holdings is a well known stock, with plenty of analyst coverage, suggesting some visibility into future growth. If you are thinking of buying or selling PayPal Holdings stock, you should check out this free report showing analyst consensus estimates for future profits.

A Different Perspective

It's good to see that PayPal Holdings has rewarded shareholders with a total shareholder return of 39% in the last twelve months. Notably the five-year annualised TSR loss of 4% per year compares very unfavourably with the recent share price performance. This makes us a little wary, but the business might have turned around its fortunes. If you would like to research PayPal Holdings in more detail then you might want to take a look at whether insiders have been buying or selling shares in the company.

We will like PayPal Holdings better if we see some big insider buys. While we wait, check out this free list of undervalued stocks (mostly small caps) with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NasdaqGS:PYPL

PayPal Holdings

Operates a technology platform that enables digital payments for merchants and consumers worldwide.

Excellent balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

Pinterest will surge as advertising innovations ignite revenue growth

Fair Value US$42.63|27.1% undervalued

BR

Community Contributor

Brambles' Revenue Set to Climb 14% with Profit Margins Following

Fair Value AU$21.90|4.9% overvalued

RO

Community Contributor

Challenging Future for STG as Organic Sales Decline by 8.8%

Fair Value DKK 116.13|26.8% undervalued

KA

Community Contributor