Advertisement

When markets get on shaky legs, it is not surprising to see money look for a safe haven. Restaurant chains like Yum! Brands, Inc. (NYSE: YUM), which operates some of the most known quick service restaurant franchises globally, could arguably belong to that category – given their target segment. Yet, their decline in 2022 has led a broad market so far.

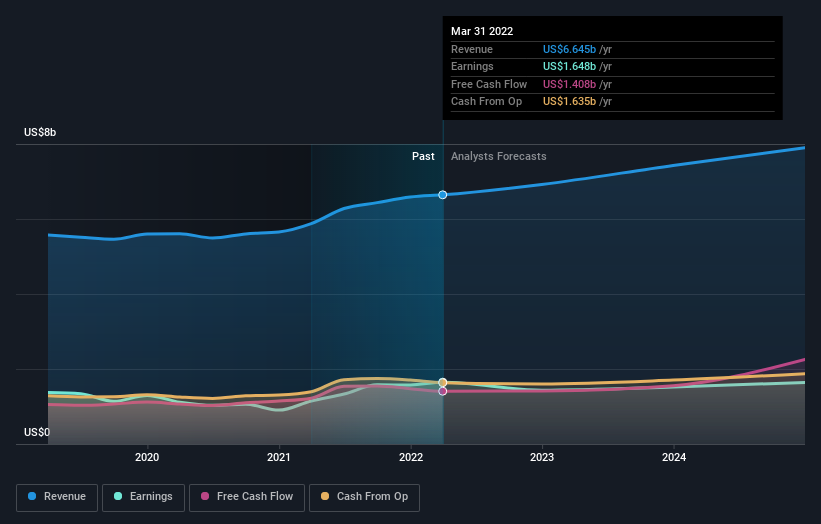

View our latest analysis for Yum! Brands

First-quarter 2022 results:

- EPS: US$1.38 (up from US$1.08 in 1Q 2021).

- Revenue: US$1.55b (up 4.1% from 1Q 2021).

- Net income: US$399.0m (up 22% from 1Q 2021).

- Profit margin: 26% (up from 22% in 1Q 2021). The increase in margin was primarily driven by higher revenue.

Revenue missed analyst estimates by 2.8%. Earnings per share (EPS) exceeded analyst estimates by 26%.

Other highlights:

- Russian impact on business: 2%

- Q1 net location additions: 628

- Q1 share buybacks: US$407m

Over the next year, revenue is forecast to grow 6.0%, compared to a 94% growth forecast for the industry in the US. Over the last 3 years, on average, earnings per share have increased by 10% per year, but its share price has only increased by 3% per year, which means it is significantly lagging behind earnings growth.

Latest Developments

A leading middle-market investment bank Baird recently went bullish on the restaurant sector. Their analyst David Tarantino noted that: “many restaurant business models contain attributes that should be considered attractive in the current market backdrop.” In particular, this concerns lower volatility and lower sensitivity to inflation compared to other consumer discretionary segments.

Furthermore, digital growth stands out as Y/Y growth topped 15% in the latest earnings results, accounting for over 40% of total transactions. Finally, while pulling out from Russia will negatively influence full-year operating profits, in 2021, that market accounted for just 2% of total sales.

Who Currently Owns Yum! Brands?

Yum! Brands has a market capitalization of US$33b, so it's too big to fly under the radar. We'd expect to see both institutions and retail investors owning a portion of the company.

Our analysis of the company's ownership below shows that institutions are noticeable on the share registry.

What Does The Institutional Ownership Tell Us About Yum! Brands?

Many institutions measure their performance against an index that approximates the local market. So they usually pay more attention to companies that are included in major indices. Yum! Brands already has institutions on the share registry, and they own a significant stake in the company. This can indicate that the company has a certain degree of credibility in the investment community. However, it is best to be wary of relying on the supposed validation that comes with institutional investors. They, too, get it wrong sometimes.

When multiple institutions own a stock, there's always a risk of being in a 'crowded trade.' Numerous parties may compete to sell stock fast when such a trade goes wrong. This risk is higher in a company without a history of growth, so we have to be mindful of Yum! Brands' historical earnings and revenue as depicted below.

Institutional investors own over 50% of the company, so together, they can probably strongly influence board decisions. Yum! Brands is not owned by hedge funds. T. Rowe Price Group, Inc. is currently the largest shareholder, with 12% of shares outstanding. The second and third largest shareholders hold about 8.5% and 7.9% of the stock.

The shareholder registry shows that the top 11 shareholders control 51% of the ownership, meaning that no single shareholder has a majority interest in the ownership.

While studying institutional ownership for a company can add value to your research, it is also a good practice to research analyst recommendations to get a deeper understanding of a stock's expected performance. Quite a few analysts cover the stock, so you could easily look into forecast growth.

Insider and General Public Ownership Of Yum! Brands

Insider ownership is positive when it signals leadership thinking like the company's actual owners. However, high insider ownership can also give immense power to a small group within the company. This can be negative in some circumstances. Our information suggests that Yum! Brands, Inc. insiders own under 1% of the company. It is a large company, so it would be surprising to see insiders own a large proportion of the company. Though their holding amounts to less than 1%, we can see that board members collectively own US$34m worth of shares (at current prices). It is good to see board members owning shares, but it might be worth checking if those insiders have been buying.

Meanwhile, the general public owns a 19% stake in the company and can't easily be ignored. While this size of ownership may not be enough to sway a policy decision in their favor, they can still collectively impact company policies.

Next Steps:

Like many franchising businesses Yum! Brands has been impacted by the recent geopolitical turmoil, although sustained growth might compensate for those losses already this year. Adding over 600 net locations in a troublesome environment of Q1 speaks for itself and adds to the economies of scale that make this segment so attractive as an inflationary hedge.

It's always worth thinking about the different groups who own shares in a company. But to understand Yum! Brands better, we need to consider many other factors. Consider, for instance, the ever-present investment risk. We've identified 3 warning signs with Yum! Brands (at least 2 which are significant) and understanding them should be part of your investment process.

Ultimately the future is most important. You can access this free report on analyst forecasts for the company.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the previous date of the month the financial statement is dated. This may not be consistent with full-year annual report figures.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Stjepan Kalinic and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Stjepan Kalinic

Stjepan is a writer and an analyst covering equity markets. As a former multi-asset analyst, he prefers to look beyond the surface and uncover ideas that might not be on retail investors' radar. You can find his research all over the internet, including Simply Wall St News, Yahoo Finance, Benzinga, Vincent, and Barron's.

About NYSE:YUM

Yum! Brands

Develops, operates, and franchises quick service restaurants worldwide.

Average dividend payer with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|65.7% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|14.9% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|35.4% undervalued

DA

Community Contributor

Product Refresh And Global Expansion Will Empower Future Market Leadership

Fair Value US$202.60|21.0% undervalued

AN

Based on Analyst Price Targets