- United States

- /

- Hospitality

- /

- NYSE:SHAK

Shake Shack (SHAK) Valuation Check After Analyst Upgrades, Strategy Shift and Executive Change

Reviewed by Simply Wall St

Shake Shack (SHAK) is back in focus after a wave of analyst attention, ranging from JPMorgan’s upgrade to fresh commentary on its shift toward a faster quick service style model and its sensitivity to beef prices.

See our latest analysis for Shake Shack.

The share price has slid to about $83.53, with a notably weak year to date share price return. However, the three year total shareholder return remains strongly positive, suggesting long term momentum and conviction are not fully broken.

If the Shake Shack story has you rethinking growth and quality, it could be worth scanning fast growing stocks with high insider ownership for other under the radar names showing strong alignment between insiders and shareholders.

With shares down sharply this year but still trading well below average analyst targets, the real question is whether Shake Shack is quietly undervalued or if the market has already priced in its next leg of growth.

Most Popular Narrative: 27% Undervalued

With the most followed narrative putting Shake Shack's fair value well above the recent close, the spotlight shifts squarely to its long term earnings power.

Analysts are assuming Shake Shack's revenue will grow by 14.8% annually over the next 3 years.

Analysts assume that profit margins will increase from 1.5% today to 5.4% in 3 years time.

Want to see what justifies that steep jump in profitability, and why a premium future earnings multiple still features in this model driven outlook? Read on.

Result: Fair Value of $114.36 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, softer traffic trends and rising beef costs could squeeze margins and challenge the optimistic earnings ramp implied by current long term forecasts.

Find out about the key risks to this Shake Shack narrative.

Another Lens on Valuation

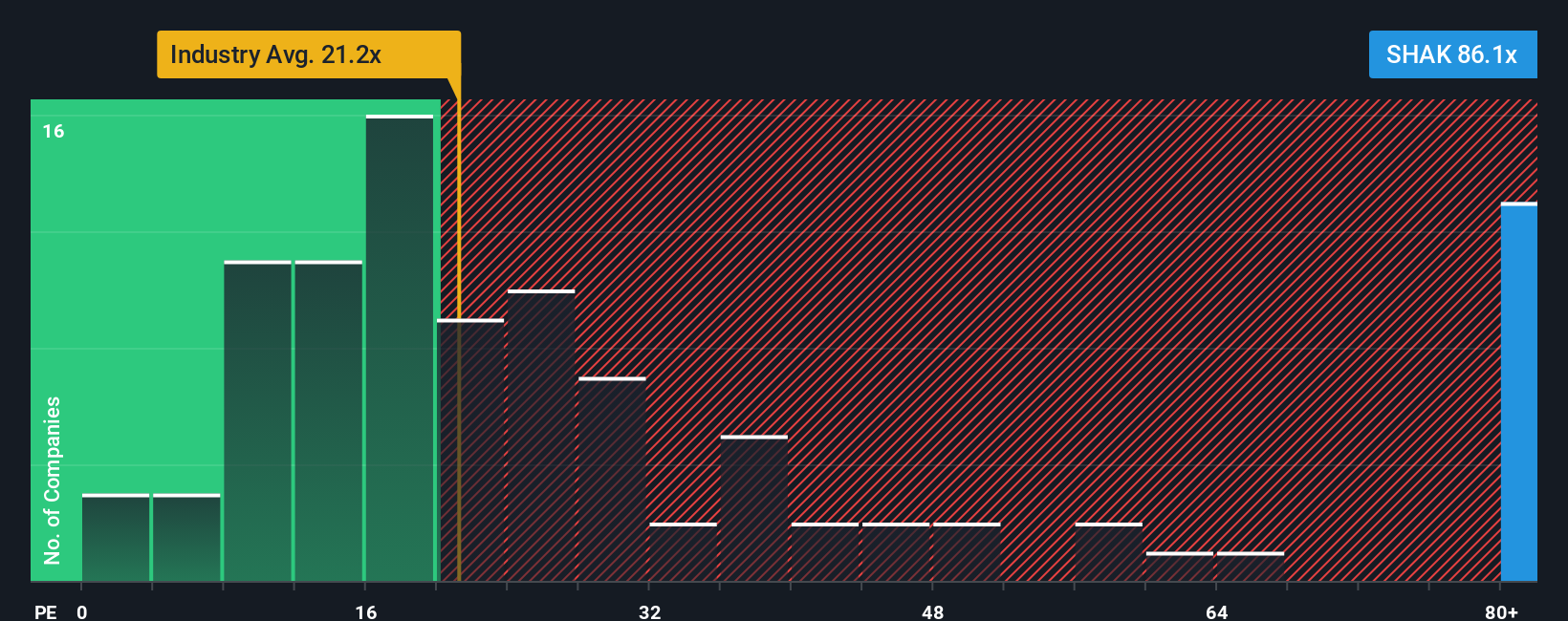

Step away from narratives and the picture looks far harsher. On a price to earnings basis, Shake Shack trades at around 78.9 times earnings, versus about 30.2 times for peers and 22 times for the wider US hospitality group. Our fair ratio sits near 26.1 times.

That gap suggests the market is already baking in years of strong execution, leaving little room for error if traffic, margins or expansion stumble. Are investors leaning too much on the long term story and not enough on today’s risks?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Shake Shack Narrative

If you would rather trust your own homework than ours, you can dig into the numbers yourself and craft a full narrative in just minutes, Do it your way.

A good starting point is our analysis highlighting 2 key rewards investors are optimistic about regarding Shake Shack.

Ready for more investment ideas?

Use the Simply Wall St Screener to quickly surface fresh opportunities that match your strategy so you are not stuck watching the same tickers everyone else is.

- Capture income potential by targeting dependable payouts and steady cash flows through these 10 dividend stocks with yields > 3% that can support long term wealth building.

- Ride powerful growth trends by focusing on innovation leaders at the intersection of medicine and machine learning with these 29 healthcare AI stocks.

- Position yourself ahead of the next wave in digital finance by reviewing these 79 cryptocurrency and blockchain stocks shaping the future of payments and blockchain infrastructure.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:SHAK

Shake Shack

Owns, operates, and licenses Shake Shack restaurants (Shacks) in the United States and internationally.

Solid track record with reasonable growth potential.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Airbnb Stock: Platform Growth in a World of Saturation and Scrutiny

Adobe Stock: AI-Fueled ARR Growth Pushes Guidance Higher, But Cost Pressures Loom

Thomson Reuters Stock: When Legal Intelligence Becomes Mission-Critical Infrastructure

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion