- United States

- /

- Hospitality

- /

- NYSE:MSC

Studio City International Holdings Limited's (NYSE:MSC) P/S Is Still On The Mark Following 28% Share Price Bounce

The Studio City International Holdings Limited (NYSE:MSC) share price has done very well over the last month, posting an excellent gain of 28%. The last 30 days bring the annual gain to a very sharp 56%.

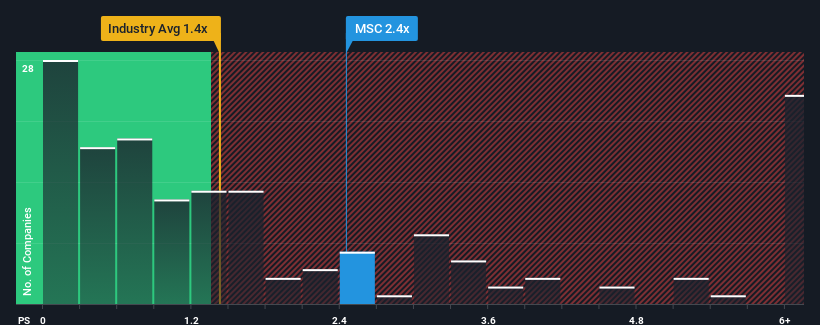

After such a large jump in price, you could be forgiven for thinking Studio City International Holdings is a stock not worth researching with a price-to-sales ratios (or "P/S") of 2.4x, considering almost half the companies in the United States' Hospitality industry have P/S ratios below 1.4x. However, the P/S might be high for a reason and it requires further investigation to determine if it's justified.

See our latest analysis for Studio City International Holdings

What Does Studio City International Holdings' Recent Performance Look Like?

Studio City International Holdings certainly has been doing a great job lately as it's been growing its revenue at a really rapid pace. Perhaps the market is expecting future revenue performance to outperform the wider market, which has seemingly got people interested in the stock. You'd really hope so, otherwise you're paying a pretty hefty price for no particular reason.

We don't have analyst forecasts, but you can see how recent trends are setting up the company for the future by checking out our free report on Studio City International Holdings' earnings, revenue and cash flow.Is There Enough Revenue Growth Forecasted For Studio City International Holdings?

There's an inherent assumption that a company should outperform the industry for P/S ratios like Studio City International Holdings' to be considered reasonable.

Retrospectively, the last year delivered an explosive gain to the company's top line. The amazing performance means it was also able to deliver huge revenue growth over the last three years. So we can start by confirming that the company has done a tremendous job of growing revenue over that time.

This is in contrast to the rest of the industry, which is expected to grow by 13% over the next year, materially lower than the company's recent medium-term annualised growth rates.

With this in consideration, it's not hard to understand why Studio City International Holdings' P/S is high relative to its industry peers. It seems most investors are expecting this strong growth to continue and are willing to pay more for the stock.

What We Can Learn From Studio City International Holdings' P/S?

The large bounce in Studio City International Holdings' shares has lifted the company's P/S handsomely. We'd say the price-to-sales ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

As we suspected, our examination of Studio City International Holdings revealed its three-year revenue trends are contributing to its high P/S, given they look better than current industry expectations. At this stage investors feel the potential continued revenue growth in the future is great enough to warrant an inflated P/S. Unless the recent medium-term conditions change, they will continue to provide strong support to the share price.

And what about other risks? Every company has them, and we've spotted 3 warning signs for Studio City International Holdings (of which 2 can't be ignored!) you should know about.

If these risks are making you reconsider your opinion on Studio City International Holdings, explore our interactive list of high quality stocks to get an idea of what else is out there.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:MSC

Studio City International Holdings

Provides provision of services pursuant to a casino contract and the hospitality business in Macau.

Imperfect balance sheet and overvalued.

Similar Companies

Market Insights

Community Narratives