Advertisement

- United States

- /

- Hospitality

- /

- NYSE:MCD

Is McDonald’s Stock at a Tipping Point After Menu Innovation Push?

Simply Wall St

Reviewed by Bailey Pemberton

- Ever wondered if McDonald's is still a good value for your investment dollar, or if it's already priced for perfection? Let's take a closer look at what the numbers are saying right now.

- The stock price has seen some movement lately, with a gain of 1.7% over the last month and a slight dip of 2.2% in the past week. Over the longer term, it is up 3.8% year-to-date and has a 5.5% return over the last year.

- Recent news highlights McDonald's strategic push into new markets and its efforts to innovate the menu, which have both caught investor attention. From revamping core offerings to expanding delivery partnerships, these moves are shaping how the market views its future potential.

- On the valuation front, McDonald's scores 2 out of 6 on undervalue checks. This suggests there are some red flags but also a few opportunities. Next, we will break down how this score stacks up under different valuation lenses and explore a thoughtful way to interpret these numbers as you continue reading.

McDonald's scores just 2/6 on our valuation checks. See what other red flags we found in the full valuation breakdown.

Approach 1: McDonald's Discounted Cash Flow (DCF) Analysis

The Discounted Cash Flow (DCF) model estimates a company’s value by forecasting its future cash flows and then discounting those amounts back to today’s value. For McDonald's, this involves projecting how much cash the business will generate in the years ahead and then adjusting those figures to account for the time value of money. This approach aims to find the company's intrinsic worth based on actual cash generation rather than pure earnings or sales numbers.

Currently, McDonald’s is generating $7.78 billion in Free Cash Flow (FCF). Analyst estimates provide insight up to 2028, at which point McDonald’s FCF is projected to reach $10.65 billion. Looking further ahead, Simply Wall St extrapolates these growth rates, with FCF in 2035 projected at $14.43 billion. All cash flows are reported in US dollars.

According to the latest DCF analysis, the model estimates McDonald’s fair value at $261.63 per share. Comparing this figure to the current market price shows the stock is trading about 16.0% above its calculated intrinsic value. This observation indicates the shares are currently overvalued based on projected cash flows.

Result: OVERVALUED

Our Discounted Cash Flow (DCF) analysis suggests McDonald's may be overvalued by 16.0%. Discover 927 undervalued stocks or create your own screener to find better value opportunities.

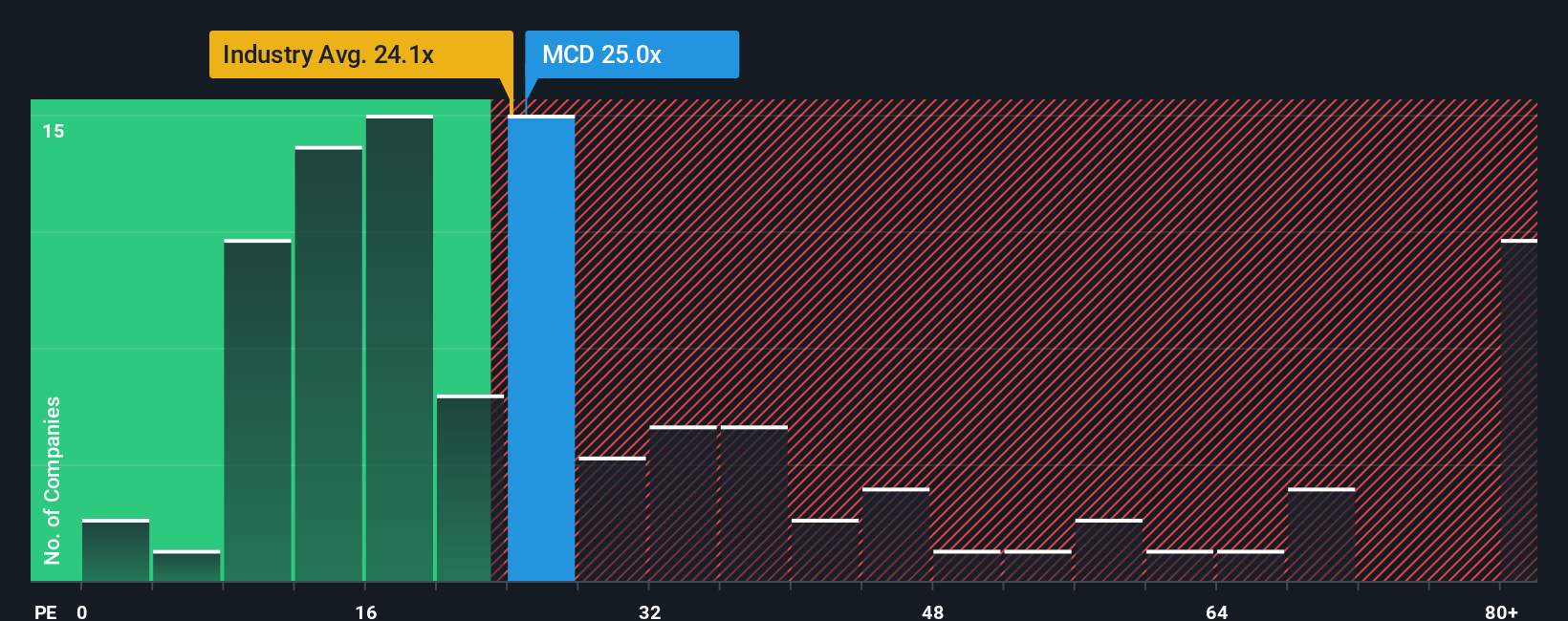

Approach 2: McDonald's Price vs Earnings

For profitable companies like McDonald's, the Price-to-Earnings (PE) ratio is a time-tested method to assess valuation. The PE ratio tells us how much investors are willing to pay for each dollar of earnings, and it is especially useful for stable, mature businesses that generate consistent profits. A "normal" or "fair" PE ratio is shaped by growth expectations and perceived risks. Companies expected to grow faster or with less risk typically command higher PE ratios, while slower-growing or riskier companies have lower ones.

Currently, McDonald's trades at a PE ratio of 25.7x. When compared to the Hospitality industry average PE of 21.3x and the peer average of 53.3x, McDonald's sits above most of its industry but well below its peers. On its own, this could suggest McDonald's is a bit more expensive than the typical hospitality company, but not exceedingly so among its direct competitors.

Simply Wall St introduces the "Fair Ratio," in this case, 30.5x, which reflects what an appropriate PE ratio should be for McDonald's after factoring in its unique earnings growth, market cap, profit margins, and business risks. Unlike a simple comparison to peers or the industry, the Fair Ratio is more tailored, accounting for the company's specific opportunities and challenges. This makes it a more relevant metric for judging whether the current valuation makes sense.

With McDonald's PE ratio of 25.7x sitting slightly below its Fair Ratio of 30.5x, the valuation appears to be about right for its profile, suggesting the stock price aligns well with what investors might expect given growth and risk levels.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1442 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your McDonald's Narrative

Earlier we mentioned that there is an even better way to understand valuation, so let's introduce you to Narratives. A Narrative is simply the story you believe about McDonald's business: the context, outlook, and assumptions that ultimately shape your estimate of its future revenue, earnings, margins, and “fair value.” Narratives connect the big picture of what is happening at McDonald's, such as new growth markets, digital transformation, or economic headwinds, with a forecast and then to a share price you consider reasonable.

Narratives are an intuitive and accessible tool now available on Simply Wall St’s Community page, used by millions of investors. By clearly documenting your Narrative and comparing your version of fair value to the current price, you can make more informed buy or sell choices. As new information comes in, such as earnings releases or breaking news, your Narrative dynamically updates, helping you stay on top of your investment thesis.

For example, some investors view McDonald's aggressive international expansion, tech investment, and menu innovation as reasons to expect a future value of $373 per share, while others see consumer headwinds and margin risks supporting a much more conservative view closer to $260. With Narratives, investing moves from following the crowd to confidently acting on your own well-reasoned perspective.

Do you think there's more to the story for McDonald's? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:MCD

McDonald's

Owns, operates, and franchises restaurants under the McDonald’s brand in the United States and internationally.

Established dividend payer with acceptable track record.

Similar Companies

Market Insights

Advertisement

Weekly Picks

FA

FAI on Arabian Internet and Communication Services ·

Solutions by stc: 34% Upside in Saudi's Digital Transformation Leader

Fair Value:ر.س342.2335.5% undervalued

10 followersusers have followed this narrative

1 commentusers have commented on this narrative

4 likesusers have liked this narrative

RO

RobertoAllende on NVIDIA ·

The AI Infrastructure Giant Grows Into Its Valuation

Fair Value:US$345.0747.9% undervalued

28 followersusers have followed this narrative

28 commentsusers have commented on this narrative

21 likesusers have liked this narrative

Recently Updated Narratives

TA

Talos on NVIDIA ·

Not a Bubble, But the "Industrial Revolution 4.0" Engine

Fair Value:US$294.9239.0% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on Advanced Micro Devices ·

The "David vs. Goliath" AI Trade – Why Second Place is Worth Billions

Fair Value:US$416.4647.2% undervalued

2 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

TA

Talos on PayPal Holdings ·

The "Sleeping Giant" Wakes Up – Efficiency & Monetization

Fair Value:US$174.9264.2% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

111 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3928.1% undervalued

945 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.4% undervalued

146 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative