Advertisement

- United States

- /

- Consumer Services

- /

- NYSE:HRB

These Metrics Don't Make H&R Block (NYSE:HRB) Look Too Strong

What financial metrics can indicate to us that a company is maturing or even in decline? More often than not, we'll see a declining return on capital employed (ROCE) and a declining amount of capital employed. This indicates the company is producing less profit from its investments and its total assets are decreasing. And from a first read, things don't look too good at H&R Block (NYSE:HRB), so let's see why.

Understanding Return On Capital Employed (ROCE)

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. The formula for this calculation on H&R Block is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.28 = US$569m ÷ (US$2.6b - US$553m) (Based on the trailing twelve months to October 2020).

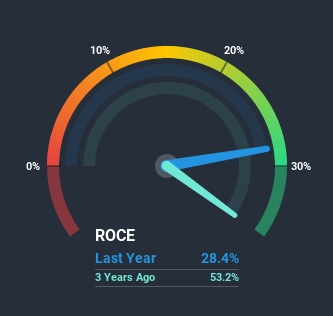

So, H&R Block has an ROCE of 28%. That's a fantastic return and not only that, it outpaces the average of 7.4% earned by companies in a similar industry.

See our latest analysis for H&R Block

In the above chart we have measured H&R Block's prior ROCE against its prior performance, but the future is arguably more important. If you'd like to see what analysts are forecasting going forward, you should check out our free report for H&R Block.

What Can We Tell From H&R Block's ROCE Trend?

In terms of H&R Block's historical ROCE movements, the trend doesn't inspire confidence. To be more specific, the ROCE was 42% five years ago, but since then it has dropped noticeably. Meanwhile, capital employed in the business has stayed roughly the flat over the period. This combination can be indicative of a mature business that still has areas to deploy capital, but the returns received aren't as high due potentially to new competition or smaller margins. So because these trends aren't typically conducive to creating a multi-bagger, we wouldn't hold our breath on H&R Block becoming one if things continue as they have.

The Bottom Line On H&R Block's ROCE

In summary, it's unfortunate that H&R Block is generating lower returns from the same amount of capital. Investors haven't taken kindly to these developments, since the stock has declined 42% from where it was five years ago. With underlying trends that aren't great in these areas, we'd consider looking elsewhere.

One final note, you should learn about the 5 warning signs we've spotted with H&R Block (including 1 which is potentially serious) .

If you'd like to see other companies earning high returns, check out our free list of companies earning high returns with solid balance sheets here.

If you decide to trade H&R Block, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if H&R Block might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About NYSE:HRB

H&R Block

Through its subsidiaries, provides assisted and do-it-yourself (DIY) tax return preparation services in the United States, Canada, and Australia.

Undervalued established dividend payer.

Similar Companies

Market Insights

Advertisement

Community Narratives

Quality at a Premium. A time to watch, not to buy?

Fair Value US$154.56|29.0% undervalued

DA

Community Contributor

GRAB: The Super-App at the Heart of Southeast Asia’s Digital Boom

Fair Value US$8.20|22.6% undervalued

BL

Community Contributor

Verve Group to Surge with 51.61% Revenue Growth

Fair Value €6.00|60.1% undervalued

ME

Community Contributor