Advertisement

- United States

- /

- Hospitality

- /

- NYSE:ARMK

Earnings Update: Here's Why Analysts Just Lifted Their Aramark (NYSE:ARMK) Price Target To US$35.14

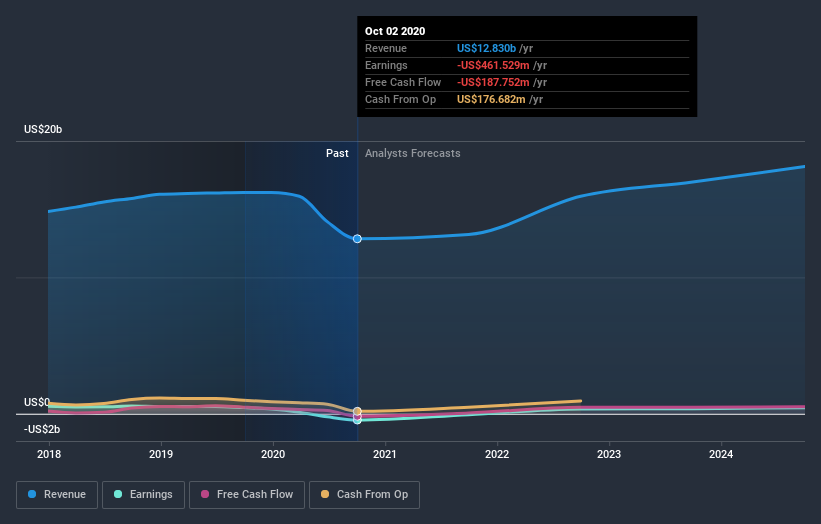

Investors in Aramark (NYSE:ARMK) had a good week, as its shares rose 3.1% to close at US$33.97 following the release of its annual results. It was a pretty bad result overall; while revenues were in line with expectations at US$13b, statutory losses exploded to US$1.83 per share. The analysts typically update their forecasts at each earnings report, and we can judge from their estimates whether their view of the company has changed or if there are any new concerns to be aware of. Readers will be glad to know we've aggregated the latest statutory forecasts to see whether the analysts have changed their mind on Aramark after the latest results.

View our latest analysis for Aramark

Taking into account the latest results, the current consensus from Aramark's twelve analysts is for revenues of US$13.1b in 2021, which would reflect an okay 2.4% increase on its sales over the past 12 months. Statutory losses are forecast to balloon 65% to US$0.65 per share. Before this earnings report, the analysts had been forecasting revenues of US$13.7b and earnings per share (EPS) of US$0.039 in 2021. There looks to have been a significant drop in sentiment regarding Aramark's prospects after these latest results, with a small dip in revenues and the analysts now forecasting a loss instead of a profit.

The analysts lifted their price target 13% to US$35.14, implicitly signalling that lower earnings per share are not expected to have a longer-term impact on the stock's value. The consensus price target is just an average of individual analyst targets, so - it could be handy to see how wide the range of underlying estimates is. Currently, the most bullish analyst values Aramark at US$42.00 per share, while the most bearish prices it at US$24.00. There are definitely some different views on the stock, but the range of estimates is not wide enough as to imply that the situation is unforecastable, in our view.

Looking at the bigger picture now, one of the ways we can make sense of these forecasts is to see how they measure up against both past performance and industry growth estimates. It's clear from the latest estimates that Aramark's rate of growth is expected to accelerate meaningfully, with the forecast 2.4% revenue growth noticeably faster than its historical growth of 1.5%p.a. over the past five years. By contrast, our data suggests that other companies (with analyst coverage) in a similar industry are forecast to grow their revenue at 24% per year. So it's clear that despite the acceleration in growth, Aramark is expected to grow meaningfully slower than the industry average.

The Bottom Line

The biggest low-light for us was that the forecasts for Aramark dropped from profits to a loss next year. On the negative side, they also downgraded their revenue estimates, and forecasts imply revenues will perform worse than the wider industry. There was also a nice increase in the price target, with the analysts clearly feeling that the intrinsic value of the business is improving.

Keeping that in mind, we still think that the longer term trajectory of the business is much more important for investors to consider. At Simply Wall St, we have a full range of analyst estimates for Aramark going out to 2024, and you can see them free on our platform here..

You should always think about risks though. Case in point, we've spotted 3 warning signs for Aramark you should be aware of, and 1 of them is significant.

If you’re looking to trade Aramark, open an account with the lowest-cost* platform trusted by professionals, Interactive Brokers. Their clients from over 200 countries and territories trade stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

About NYSE:ARMK

Aramark

Provides food and facilities services to education, healthcare, business and industry, sports, leisure, and corrections clients in the United States and internationally.

Proven track record with moderate growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|3.6% undervalued

TI

Community Contributor