Advertisement

- United States

- /

- Hospitality

- /

- NasdaqGS:WYNN

Is Macau’s Gaming Revenue Rebound Altering the Investment Case for Wynn Resorts (WYNN)?

Simply Wall St

Reviewed by Sasha Jovanovic

- During October 2025, reports highlighted a strong rebound in Macau's gross gaming revenue, an important market for luxury hotel and casino operator Wynn Resorts due to the company’s substantial Macau exposure.

- This unexpected surge brought renewed optimism among analysts regarding Wynn’s upcoming third-quarter earnings and reinforced positive expectations for the firm’s business fundamentals.

- With Macau’s gaming revenue rebound as a catalyst, we'll examine how this shapes Wynn Resorts’ investment narrative and near-term outlook.

Uncover the next big thing with financially sound penny stocks that balance risk and reward.

Wynn Resorts Investment Narrative Recap

To be a shareholder in Wynn Resorts, you must have confidence in the resilience of global luxury gaming demand and management’s ability to capture growth from Macau and new regions, while effectively managing regulatory and cost pressures. The recent rebound in Macau’s gaming revenue meaningfully supports the key near-term catalyst, Macau market recovery, but does not eliminate ongoing geopolitical and operational risks, which remain the principal threat to business stability and profit margins.

Among recent developments, Wynn’s acquisition of the Wynn Mayfair in London stands out as a move to expand its international presence, offering potential diversification and growth beyond Macau. While promising as a catalyst, it does not reduce short-term exposure to Macau's regulatory or travel fluctuations, which remain closely tied to the company's investment case.

Yet, while optimism is growing about Macau’s recovery, investors should be aware that rising operating costs and regulatory shifts could still...

Read the full narrative on Wynn Resorts (it's free!)

Wynn Resorts' outlook anticipates $8.0 billion in revenue and $624.0 million in earnings by 2028. This is based on an expected 4.6% annual revenue growth and a $240.1 million increase in earnings from current earnings of $383.9 million.

Uncover how Wynn Resorts' forecasts yield a $134.09 fair value, a 11% upside to its current price.

Exploring Other Perspectives

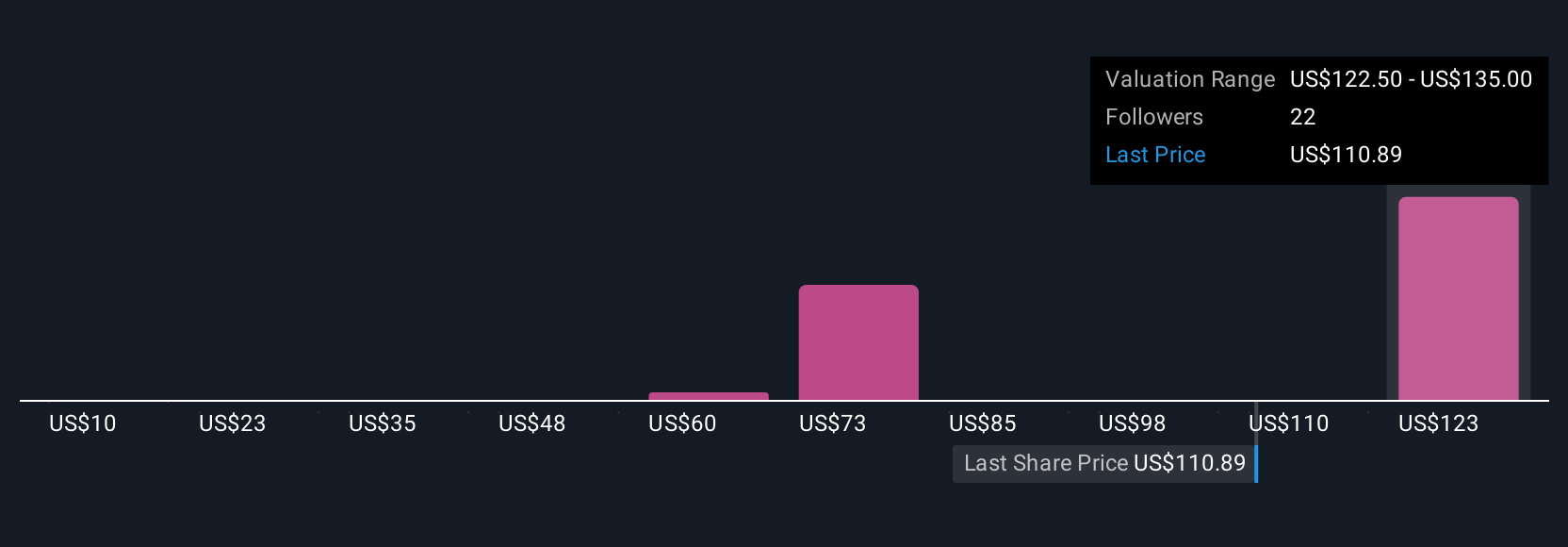

Community members at Simply Wall St produced fair value estimates for Wynn Resorts ranging from US$10 to US$135, based on nine unique analyses. Their wide range of expectations reflects the importance of factors like Macau exposure and regulatory risk as you weigh different outlooks and investment potential.

Explore 9 other fair value estimates on Wynn Resorts - why the stock might be worth less than half the current price!

Build Your Own Wynn Resorts Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Wynn Resorts research is our analysis highlighting 1 key reward and 3 important warning signs that could impact your investment decision.

- Our free Wynn Resorts research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Wynn Resorts' overall financial health at a glance.

Interested In Other Possibilities?

Don't miss your shot at the next 10-bagger. Our latest stock picks just dropped:

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 24 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- Rare earth metals are the new gold rush. Find out which 37 stocks are leading the charge.

- These 12 companies survived and thrived after COVID and have the right ingredients to survive Trump's tariffs. Discover why before your portfolio feels the trade war pinch.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Wynn Resorts might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:WYNN

Moderate growth potential with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|7.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.8% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.4% undervalued

GM

Community Contributor