Advertisement

- United States

- /

- Consumer Services

- /

- NasdaqGS:FTDR

Is Analyst Optimism and Upward Estimates Changing the Investment Case for Frontdoor (FTDR)?

Simply Wall St

Reviewed by Simply Wall St

- Frontdoor recently earned a Zacks Rank #1 (Strong Buy) following a series of upward earnings estimate revisions by analysts, reflecting heightened confidence in the company’s near-term financial outlook.

- This shift in sentiment highlights growing analyst optimism driven by Frontdoor’s improving performance expectations, which could influence broader industry perceptions and investor attention.

- To assess the significance of this improving analyst outlook, let's examine how it shapes Frontdoor’s overall investment narrative and long-term prospects.

Rare earth metals are an input to most high-tech devices, military and defence systems and electric vehicles. The global race is on to secure supply of these critical minerals. Beat the pack to uncover the 28 best rare earth metal stocks of the very few that mine this essential strategic resource.

Frontdoor Investment Narrative Recap

To be a Frontdoor shareholder, you likely need to believe in the company’s ability to leverage technology, product expansion, and housing market recovery to drive recurring revenue growth. The recent Zacks Rank #1 upgrade signals analyst optimism on near-term earnings, but it does not fundamentally change the biggest short-term catalyst: a possible rebound in home warranty membership driven by the housing market; nor does it remove the central risk of persistent declines in core member count due to real estate headwinds.

Among all recent announcements, the Q2 2025 earnings results are most relevant in the context of upgraded analyst sentiment. With sales and earnings both up year-on-year and improved net margins, these results reinforce the optimism seen in rising earnings estimates, while drawing attention to Frontdoor’s execution on profitability and cost control, critical levers for sustaining momentum regardless of near-term membership trends.

However, despite a stronger earnings outlook, investors should be aware that continued declines in core home warranty member count could still...

Read the full narrative on Frontdoor (it's free!)

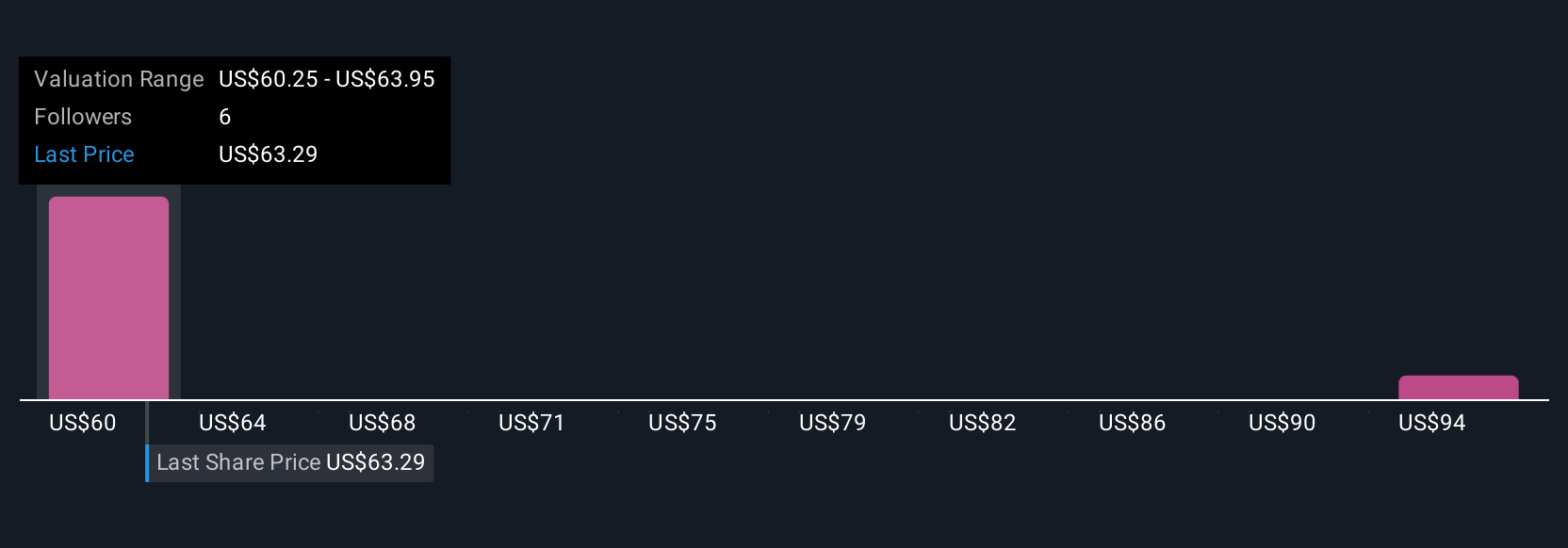

Frontdoor's narrative projects $2.4 billion revenue and $279.0 million earnings by 2028. This requires 7.2% yearly revenue growth and a $22 million earnings increase from $257.0 million.

Uncover how Frontdoor's forecasts yield a $60.25 fair value, in line with its current price.

Exploring Other Perspectives

Simply Wall St Community members provided two fair value estimates for Frontdoor ranging from US$60.25 to US$96.85. With ongoing concerns about member count declines, you may want to explore several distinct viewpoints before forming your own expectations.

Explore 2 other fair value estimates on Frontdoor - why the stock might be worth just $60.25!

Build Your Own Frontdoor Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Frontdoor research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Frontdoor research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Frontdoor's overall financial health at a glance.

No Opportunity In Frontdoor?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- AI is about to change healthcare. These 28 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

- The best AI stocks today may lie beyond giants like Nvidia and Microsoft. Find the next big opportunity with these 25 smaller AI-focused companies with strong growth potential through early-stage innovation in machine learning, automation, and data intelligence that could fund your retirement.

- The end of cancer? These 29 emerging AI stocks are developing tech that will allow early identification of life changing diseases like cancer and Alzheimer's.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:FTDR

Frontdoor

Provides home and new home structural warranties in the United States.

Good value with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Defense AI: A Robotic Response to America’s Security Gaps

Fair Value US$12.00|49.7% undervalued

MA

Community Contributor

Figma (FIG): The S&P 500’s Design Standard Turning Into an All-in-One Platform

Fair Value US$65.70|7.0% overvalued

TI

Community Contributor

Sleep Cycle's Revenue Set to Rise 10% with Strong Revenue Model

Fair Value SEK 38.04|20.3% undervalued

MA

Community Contributor

Has JB Hi-Fi Lost Its Point of Difference?

Fair Value AU$76.00|52.5% overvalued

RO

Community Contributor