Expedia Group (EXPE) shares have seen some shifts recently, offering investors a chance to reassess how the company is positioned in the evolving online travel sector. With stock performance trending higher this year, there is growing interest in what might come next.

Expedia Group’s solid upward momentum in 2024 continues to catch attention, especially after this year’s 29.5% year-to-date share price return. While the past week was choppy, longer-term, total shareholder returns of 35% over the last year and nearly 140% in three years highlight persistent confidence in the business and its growth potential.

With Expedia trading near its highs and showing strong growth, the key question is whether all that future potential is already reflected in the price, or if there is still room for investors to capitalize on further upside.

Advertisement

Most Popular Narrative: 9.4% Undervalued

Expedia Group’s most-followed valuation narrative values the shares at $264.91, around 9% above the last close of $240. This sets the stage for a forward-looking debate about just what is fueling the company's market momentum.

Ongoing shift in consumer preference toward digital and mobile channels, paired with increased adoption of AI-powered search and personalization on Expedia's platforms, is driving higher conversion rates and improved retention. This should support sustained revenue growth and margin expansion. Unified global technology platform and greater automation (including AI-powered developer tools and personalized insurance products) are already producing faster feature delivery, improved customer experience, and reduced operating costs. These developments are expected to further expand EBITDA margins and benefit earnings over the next several years.

Want to see what sets this valuation apart? There is a bold set of growth projections behind that number and a profit profile reminiscent of industry disruptors. The biggest upside surprise hides in their future margin game and the scale of ongoing tech investments. Curious how the numbers play out? Dive in to uncover the critical financial leaps this narrative is betting on.

However, persistent weakness in U.S. travel demand or tougher competition from rival platforms could quickly undermine Expedia’s momentum and challenge these optimistic forecasts.

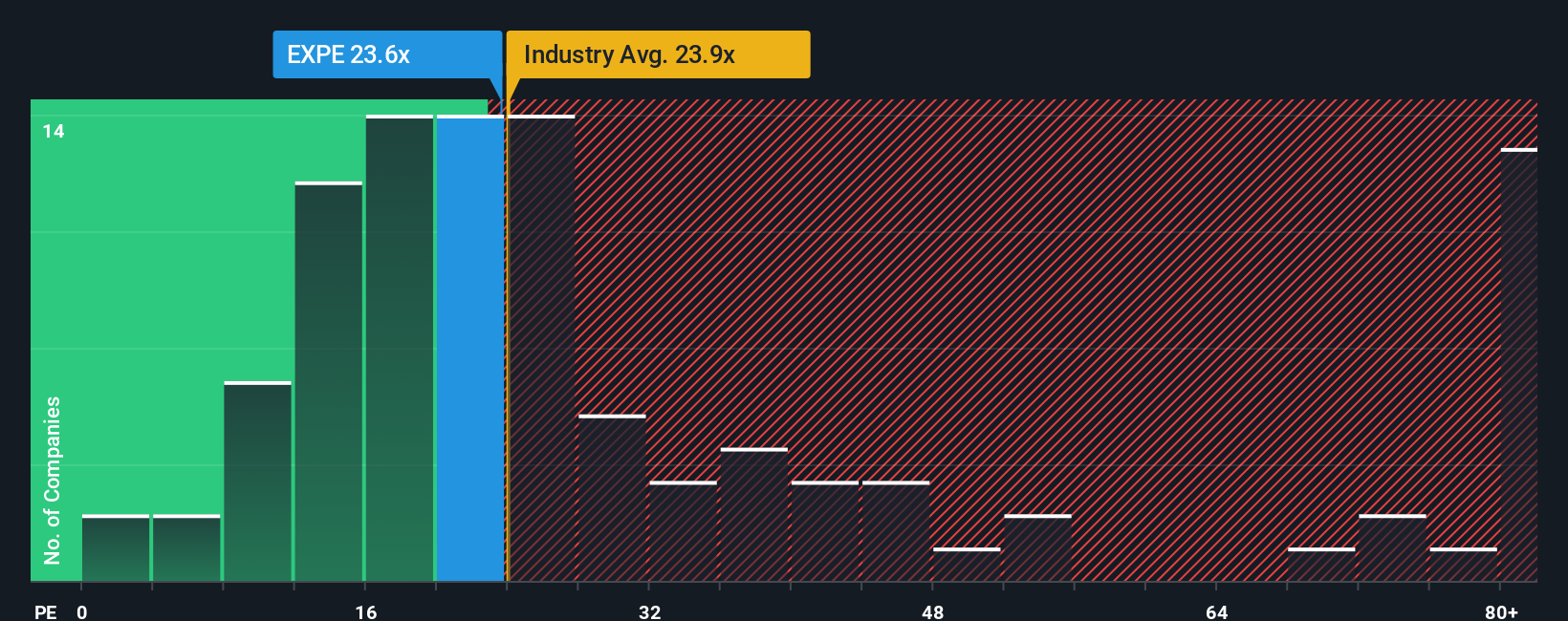

Looking at Expedia’s valuation through the lens of its price-to-earnings ratio, the shares trade at 21.2x, slightly above the US Hospitality industry average of 20.8x but well below peers averaging 29.1x. Compared to our fair ratio estimate of 29.6x, there is room for the market to reconsider its stance. Does this suggest overlooked upside, or premium risk?

If this perspective doesn't quite resonate, or you want to chart your own course, you can quickly craft your own data-driven narrative. Do it your way with Do it your way.

A good starting point is our analysis highlighting 3 key rewards investors are optimistic about regarding Expedia Group.

Looking for more investment ideas?

Smart investors know new opportunities are just a click away. Don’t let the next breakout stock or hidden value slip through your fingers. Explore these handpicked ideas now.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Expedia Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.