Advertisement

- United States

- /

- Hospitality

- /

- NasdaqGS:DPZ

A Look at Domino’s Pizza (DPZ) Valuation After Strong Q3 Earnings and International Rebound

Simply Wall St

Reviewed by Simply Wall St

Domino's Pizza (DPZ) topped analyst expectations for third quarter earnings per share, showcasing healthy U.S. same-store sales growth and a return to expansion internationally. This performance highlights its effective value promotions as well as its digital strategy.

See our latest analysis for Domino's Pizza.

After a rocky stretch earlier in the year, Domino’s shares have begun to regain ground, reflecting renewed confidence as the company delivers on digital growth and bold value offerings. The stock’s 1-year total shareholder return of 2.0% trails some broader benchmarks, but a three-year total return of 37.6% signals that long-term investors have been rewarded for their patience. Even as short-term momentum has cooled, recent buybacks and a maintained dividend point to an ongoing commitment to shareholders amid a challenging market.

If Domino’s resurgence has you thinking about what’s next in the market, it might be the perfect moment to broaden your outlook and discover fast growing stocks with high insider ownership

But with Domino’s shares climbing off their lows and analysts forecasting further gains, the real question is whether the recent upside is just the beginning of a larger rebound or if future growth is already reflected in current prices.

Most Popular Narrative: 15% Undervalued

The narrative consensus puts Domino’s fair value at $502 per share, which is comfortably above the recent close of $424.82. This sets up a debate over whether analysts are underestimating Domino’s digital and delivery tailwinds or if the market is pricing in risk.

The recent full national rollout on DoorDash, building on last year's Uber Eats integration, is expected to be a multiyear growth driver. This allows Domino's to tap into a broader, digitally native customer base and meet rising consumer preference for at-home dining and off-premise consumption. These factors could drive higher delivery segment revenues and increased market share.

Curious what growth assumptions power that bold fair value? There is a jaw-dropping projection for Domino’s future profits and a profit multiple that rivals market leaders. Unlock the secrets behind these bullish figures to find out what is fueling the optimism and decide if you agree with the most popular market narrative.

Result: Fair Value of $502 (UNDERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, slowing global pizza demand and tougher year-over-year comparisons could easily derail Domino’s momentum and challenge these upbeat projections.

Find out about the key risks to this Domino's Pizza narrative.

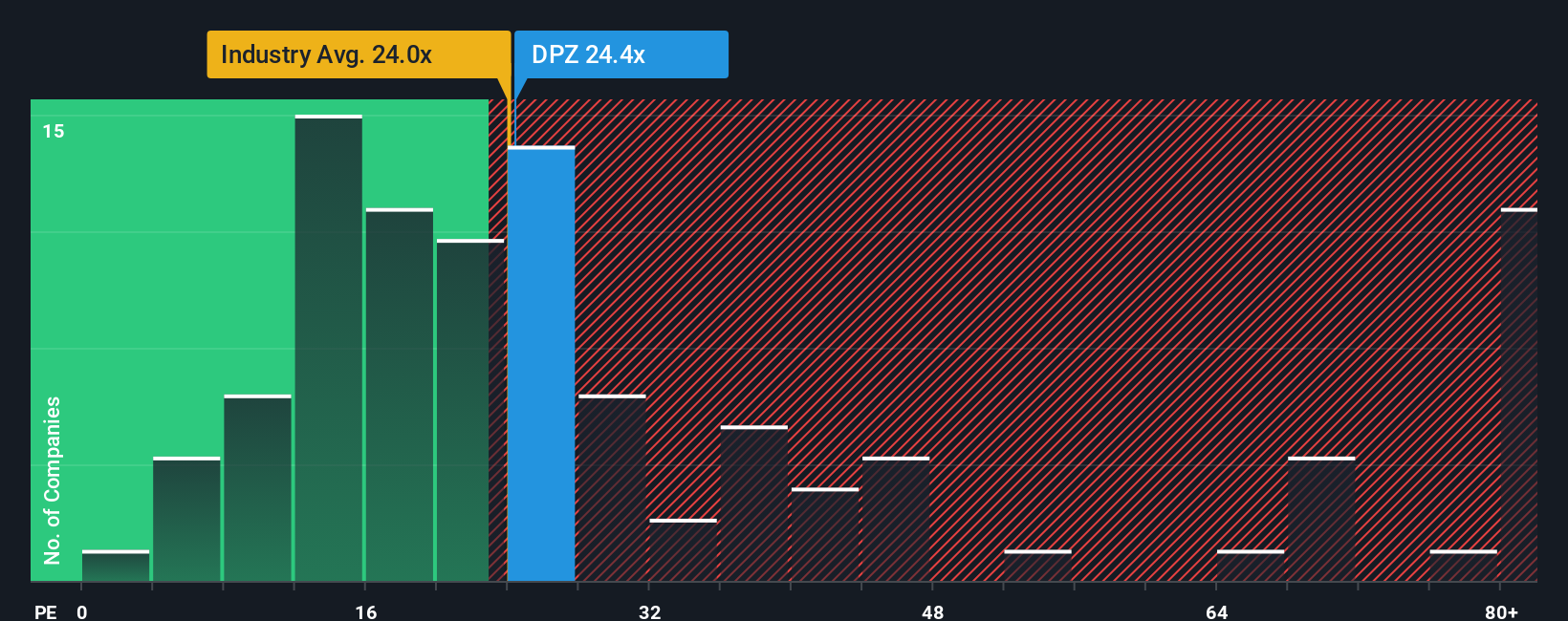

Another View: Market Multiples Tell a Different Story

While some see value in Domino’s long-term narrative, the market’s go-to benchmark, price-to-earnings, suggests a premium. Domino’s trades at 24.3 times earnings, slightly higher than the peer average of 23.4x and the industry at 24.2x, and above the fair ratio of 22.6x. This signals a risk that the market’s enthusiasm might already be fully priced in. Is growth strong enough to maintain this rich valuation, or could investor expectations reset?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Domino's Pizza Narrative

If you want to dig deeper or see things from another angle, you can shape your own Domino’s story in just a few minutes. Do it your way

A great starting point for your Domino's Pizza research is our analysis highlighting 3 key rewards and 2 important warning signs that could impact your investment decision.

Looking for More Compelling Investment Ideas?

Don’t wait for opportunity to come to you. Use the Simply Wall Street Screener now to pinpoint fresh stocks and bold market trends you may be missing.

- Capitalize on those hidden gems delivering high potential while staying under Wall Street’s radar by checking out these 875 undervalued stocks based on cash flows right now.

- Boost your portfolio’s income with reliable picks that offer consistent yields. See these 17 dividend stocks with yields > 3% to access the leaders in strong dividends.

- Ride the next tech wave and join forward-thinkers already backing these 26 AI penny stocks driving innovation in artificial intelligence and machine learning.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DPZ

Domino's Pizza

Operates as a pizza company in the United States and internationally.

Established dividend payer with questionable track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.5% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.8% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|26.5% undervalued

GM

Community Contributor