Walmart (NYSE:WMT) is navigating a dynamic environment marked by both opportunities and challenges. Recent highlights include a notable increase in eCommerce sales and strategic alliances, juxtaposed against a high valuation and slower revenue growth forecast. In the discussion that follows, we will delve into Walmart's financial health, operational inefficiencies, strategic growth initiatives, and external threats to provide a comprehensive overview of the company's current business situation.

Strengths: Core Advantages Driving Sustained Success For Walmart

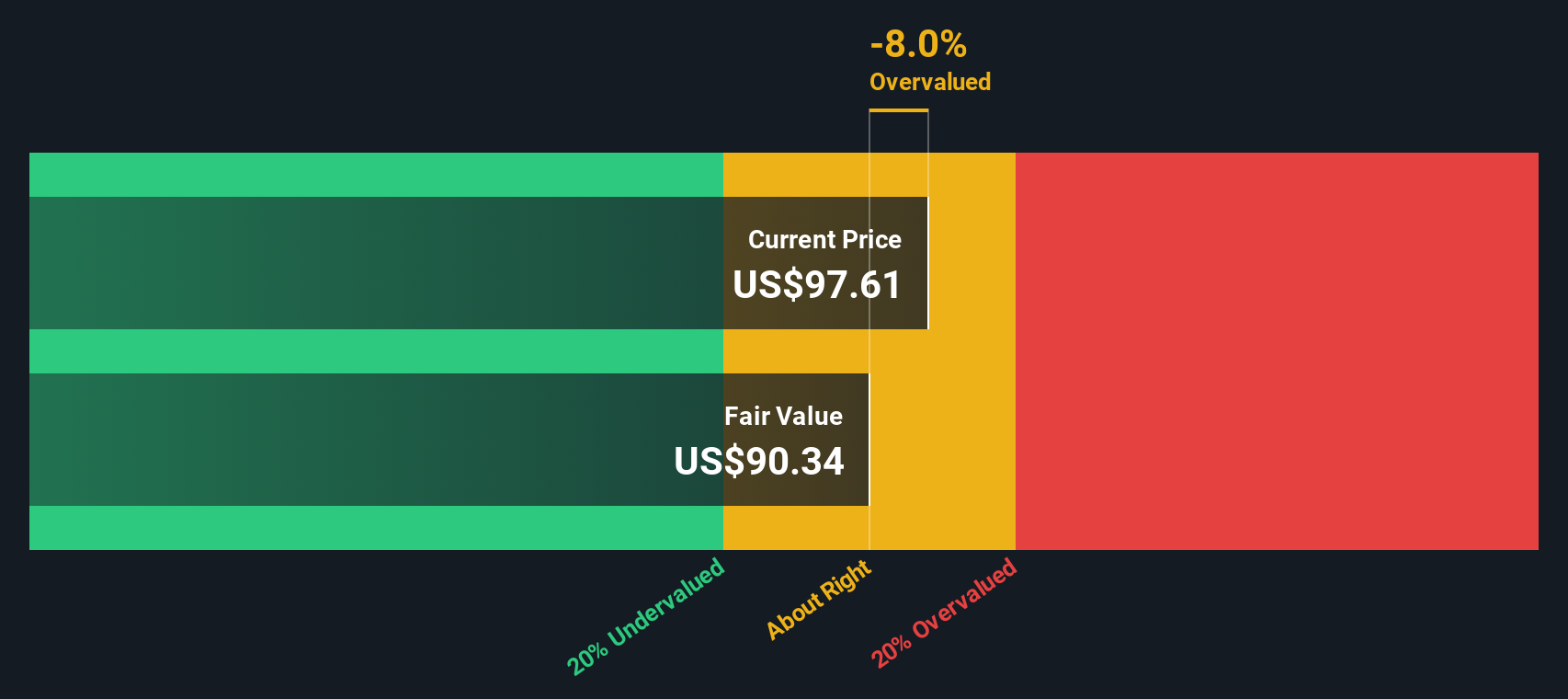

Walmart's financial health is robust, with a notable increase in earnings and revenue. For instance, the company reported second-quarter revenue of $169.34 billion, up from $161.63 billion a year ago. This growth is complemented by strong sales and profit growth, as highlighted by CEO Doug McMillon, who stated, "We had another good quarter with strong sales growth and even stronger profit growth exceeding our expectations." Moreover, Walmart's eCommerce sales grew by 21%, demonstrating its successful digital strategy. The company's dividend payments have been reliable and steadily increasing over the past decade, with a payout ratio of 41.2%, indicating sustainable dividends. Furthermore, Walmart's experienced management team and board of directors, with average tenures of 4.3 and 8.3 years respectively, contribute significantly to its strategic goals. Despite a high Price-To-Earnings Ratio of 40.3x, Walmart is trading below its estimated fair value of $86.63, suggesting it may be undervalued.

Weaknesses: Critical Issues Affecting Walmart's Performance and Areas For Growth

Walmart faces several financial challenges, including its expensive valuation compared to peers and the industry. With a Price-To-Earnings Ratio of 40.3x, it is significantly higher than the peer average of 26.3x and the US Consumer Retailing industry average of 22x. Additionally, the company's earnings growth, although improved at 10.8% over the past year, still lags behind the broader US market's expected growth rate of 15.2% per year. CFO John Rainey mentioned increased marketing and higher variable pay expenses, which have led to expense deleverage across segments. Furthermore, Walmart's revenue growth forecast of 4% per year is slower than the US market's 8.7% per year, indicating potential areas for improvement in accelerating growth.

Opportunities: Potential Strategies for Leveraging Growth and Competitive Advantage

Walmart has several opportunities to enhance its market position and capitalize on emerging trends. The company is expanding its Marketplace items and sellers by around 60%, as noted by CFO John Rainey, which could drive significant growth in the eCommerce segment. Technological advancements, including leveraging generative AI, are expected to improve customer and associate experiences, as highlighted by Doug McMillon. Additionally, Walmart's strategic alliances and new product offerings, such as the collaboration with Chuck E. Cheese and the introduction of private brand products, provide avenues for revenue diversification and market expansion. The company's focus on operational efficiency and sustainability initiatives, like the innovative depackaging services, further strengthen its competitive edge.

Threats: Key Risks and Challenges That Could Impact Walmart's Success

Walmart faces several external threats that could impact its long-term success. Economic uncertainty and geopolitical volatility, as mentioned by John Rainey, create a challenging operating environment. The competitive landscape in the retail sector is intense, with pressures to maintain everyday low prices without compromising margins. Additionally, significant insider selling over the past three months raises concerns about insider confidence in the company's future performance. Changes in consumer behavior, with customers becoming more discerning and value-conscious, could also affect Walmart's sales and profitability. Despite these challenges, the company's strategic initiatives and strong market position provide a buffer against potential risks.

Conclusion

Walmart's strong financial health, evidenced by significant revenue and earnings growth, and a successful digital strategy, positions it well for sustained success. Despite challenges such as higher expenses and slower revenue growth compared to the broader market, Walmart's strategic initiatives in eCommerce expansion and technological advancements offer promising avenues for future growth. External threats like economic uncertainty and competitive pressures remain, but Walmart's strategic focus and market position provide resilience. Notably, the company is trading below its estimated fair value of $86.63, suggesting potential for future appreciation despite its high Price-To-Earnings Ratio, indicating that the market may not fully recognize its long-term growth potential.

Turning Ideas Into Actions

Are you invested in Walmart already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Valuation is complex, but we're here to simplify it.

Discover if Walmart might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Simply Wall St analyst Simply Wall St and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

About NYSE:WMT

Walmart

Engages in the operation of retail and wholesale stores and clubs, eCommerce websites, and mobile applications worldwide.