Advertisement

- United States

- /

- Food and Staples Retail

- /

- NYSE:TGT

Is Target Now a Potential Opportunity After its 2024 Share Price Slump?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Target is quietly turning into a value opportunity after a rough stretch in the market? Let us walk through whether today’s price really stacks up against the company’s fundamentals.

- Despite a sharp drawdown, with the stock still down 34.1% year to date and 27.4% over the last year, recent moves have been more muted, with a 0.7% gain over the past week and a 1.1% slip across the last 30 days as investors reassess the risk reward trade off.

- Sentiment around Target has been shaped by ongoing headlines about shifting consumer spending patterns and the company’s efforts to refine its merchandising mix in a more cautious retail environment. At the same time, updates on store remodels, digital fulfillment investments, and inventory discipline have kept the long term story in focus for investors trying to gauge whether the worst of the reset is already priced in.

- Right now, Target scores a 5/6 on our valuation checks, suggesting it screens as undervalued on most of the key metrics we track. Next, we will unpack those methods in detail, while saving an even more insightful way to think about valuation for the end of the article.

Find out why Target's -27.4% return over the last year is lagging behind its peers.

Approach 1: Target Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow, or DCF, estimates what a business is worth by projecting the cash it can generate in the future and then discounting those cash flows back to today in dollar terms.

For Target, the model used is a 2 Stage Free Cash Flow to Equity approach. The company generated around $2.9 billion in free cash flow over the last twelve months, and analysts expect free cash flow to fluctuate but gradually grow over time, reaching about $2.8 billion by 2030. Estimates for the first several years are taken from analysts, while the outer year projections are extrapolated by Simply Wall St based on a slowing long term growth profile.

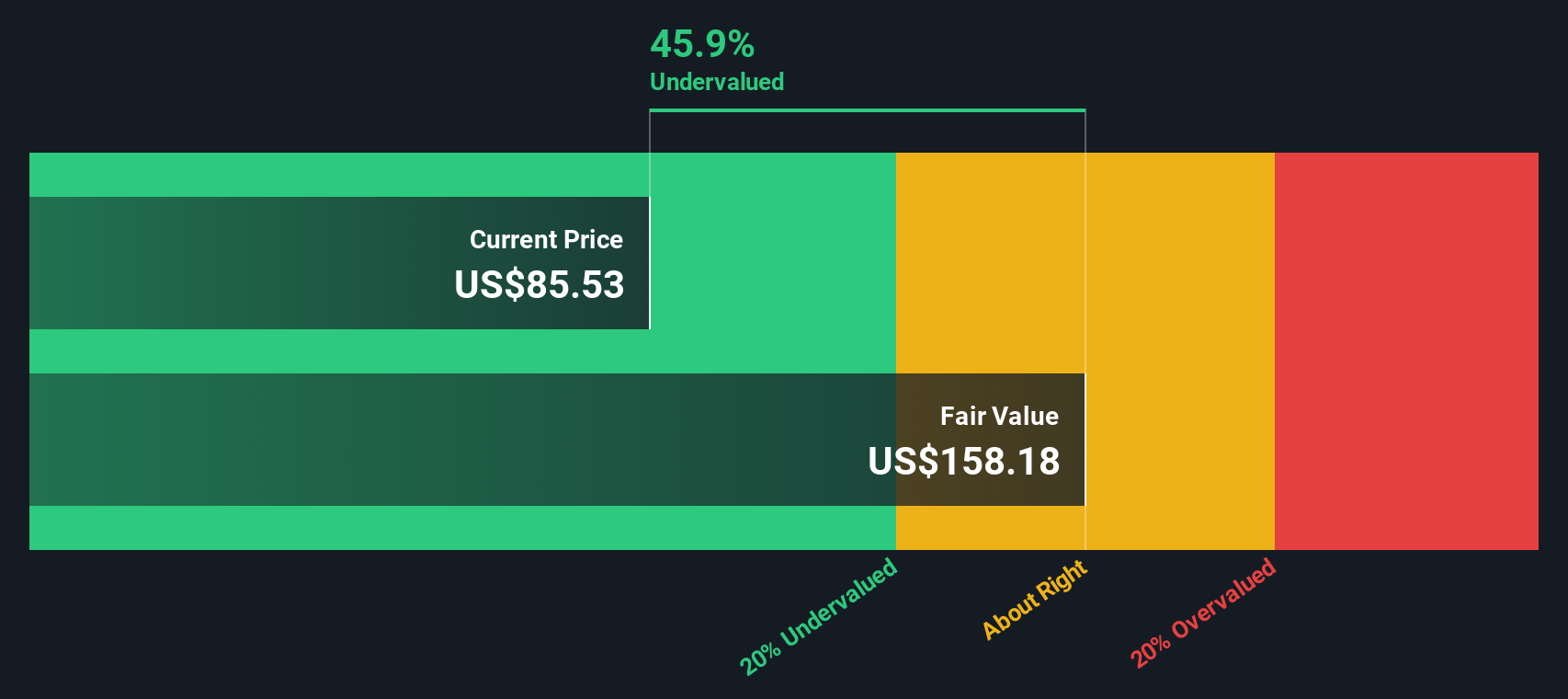

When all of these projected cash flows are discounted back, the intrinsic value for Target is calculated at roughly $133.63 per share. Compared with the current share price, this suggests the stock is about 32.3% undervalued on a cash flow basis, which may indicate that the market is pricing in a more pessimistic outlook than the model.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Target is undervalued by 32.3%. Track this in your watchlist or portfolio, or discover 925 more undervalued stocks based on cash flows.

Approach 2: Target Price vs Earnings

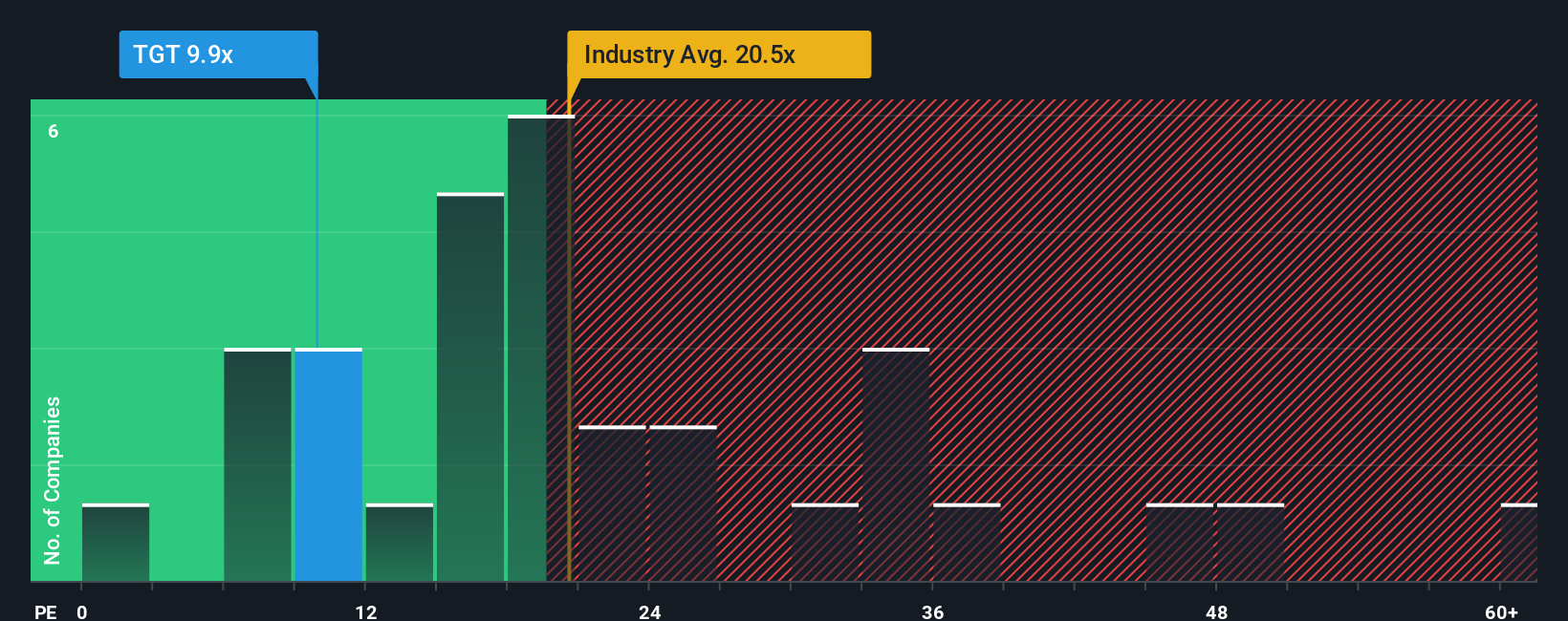

For profitable, established retailers like Target, the price to earnings, or PE, ratio is a practical way to gauge value because it directly links what investors pay today to the profits the business is already generating.

In general, companies with stronger growth prospects and lower perceived risk can justify a higher PE multiple, while slower growth or elevated uncertainty usually calls for a lower, more conservative multiple. Target currently trades on a PE of about 10.9x, which is well below both the Consumer Retailing industry average of roughly 20.0x and the broader peer group average of around 27.9x.

Simply Wall St’s Fair Ratio framework goes a step further by estimating what a reasonable PE should be for Target, given its specific mix of earnings growth, profit margins, industry positioning, market cap and risk profile. This tailored Fair Ratio for Target is 19.3x, which may be more informative than relying solely on broad industry or peer comparisons that may not share the same fundamentals. With the current PE at 10.9x versus a Fair Ratio of 19.3x, the shares appear attractively priced on an earnings basis.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1441 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your Target Narrative

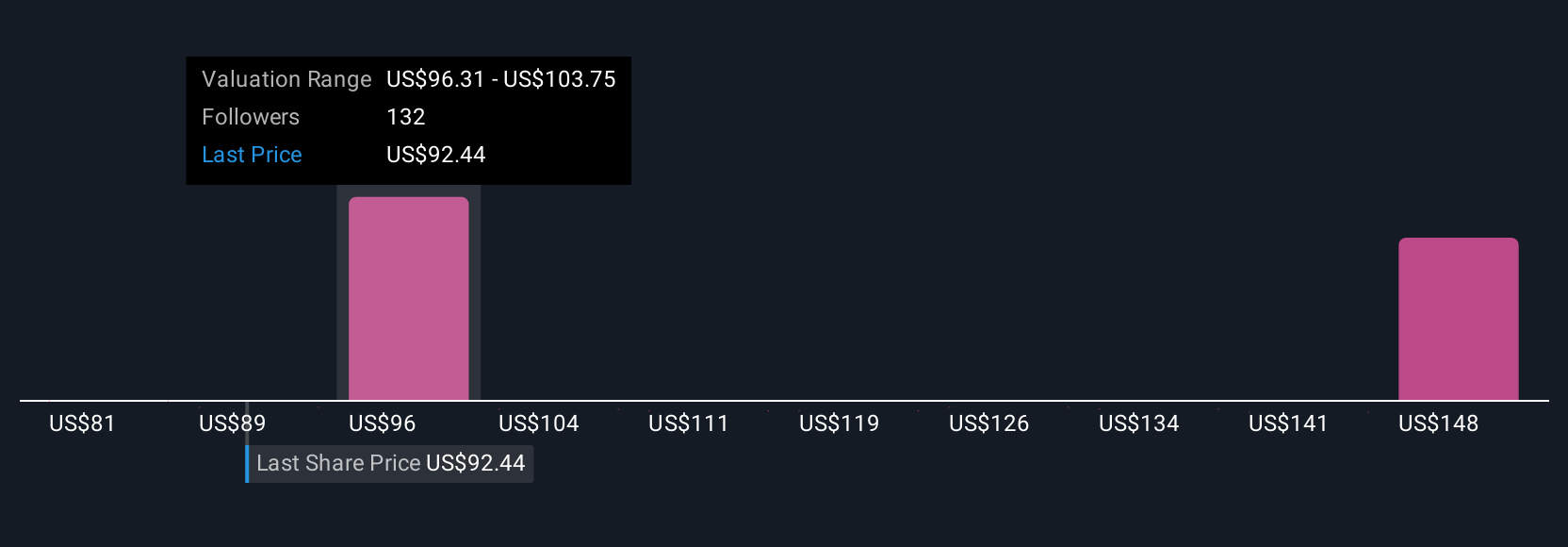

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, a simple tool on Simply Wall St’s Community page that lets you connect your view of a company’s story with the numbers by expressing your assumptions for revenue, earnings and margins. It then turns those inputs into a forward forecast and a Fair Value you can compare with today’s share price to help you decide whether to buy, hold or sell. The platform continuously updates those Narratives as new news or earnings arrive. For Target, one investor might build a cautious Narrative around weak discretionary spending and margin pressure that supports a lower fair value near 82 dollars. Another might create a more optimistic Narrative that emphasizes digital growth, private label strength and efficiency gains, supporting a higher fair value closer to 135 dollars. This spread in live, dynamic Narratives helps you see where your own view fits and how your decision could change as the story and data evolve.

Do you think there's more to the story for Target? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Target might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:TGT

6 star dividend payer and undervalued.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

24 followersusers have followed this narrative

6 commentsusers have commented on this narrative

7 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1919.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5200.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Applied Digital ·

Staggered by dilution; positions for growth

Fair Value:US$35.4520.9% undervalued

5 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.5% undervalued

949 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.1% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative