Advertisement

- United States

- /

- Food and Staples Retail

- /

- NYSE:NGVC

Here's Why Natural Grocers by Vitamin Cottage (NYSE:NGVC) Can Manage Its Debt Responsibly

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Natural Grocers by Vitamin Cottage, Inc. (NYSE:NGVC) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. When we examine debt levels, we first consider both cash and debt levels, together.

What Is Natural Grocers by Vitamin Cottage's Debt?

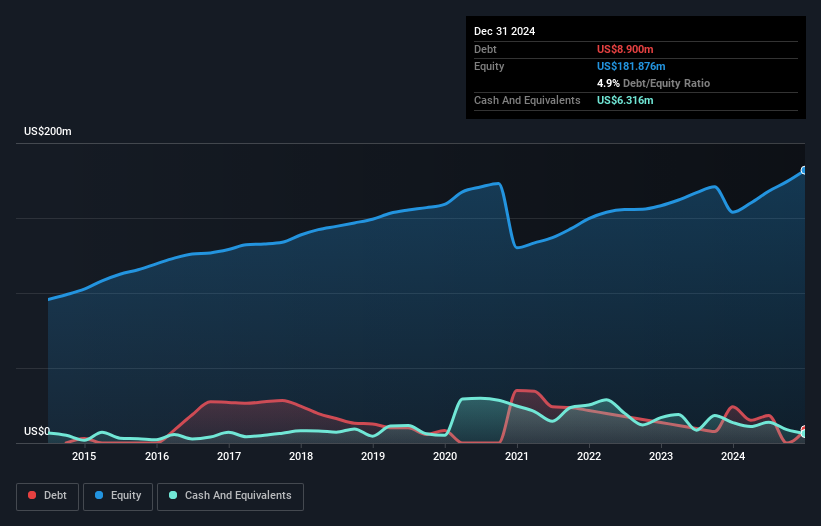

As you can see below, Natural Grocers by Vitamin Cottage had US$8.90m of debt at December 2024, down from US$24.1m a year prior. However, because it has a cash reserve of US$6.32m, its net debt is less, at about US$2.58m.

A Look At Natural Grocers by Vitamin Cottage's Liabilities

We can see from the most recent balance sheet that Natural Grocers by Vitamin Cottage had liabilities of US$150.1m falling due within a year, and liabilities of US$316.9m due beyond that. Offsetting these obligations, it had cash of US$6.32m as well as receivables valued at US$11.9m due within 12 months. So it has liabilities totalling US$448.8m more than its cash and near-term receivables, combined.

This deficit isn't so bad because Natural Grocers by Vitamin Cottage is worth US$1.04b, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. Carrying virtually no net debt, Natural Grocers by Vitamin Cottage has a very light debt load indeed.

Check out our latest analysis for Natural Grocers by Vitamin Cottage

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

With debt at a measly 0.03 times EBITDA and EBIT covering interest a whopping 12.3 times, it's clear that Natural Grocers by Vitamin Cottage is not a desperate borrower. Indeed relative to its earnings its debt load seems light as a feather. In addition to that, we're happy to report that Natural Grocers by Vitamin Cottage has boosted its EBIT by 38%, thus reducing the spectre of future debt repayments. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Natural Grocers by Vitamin Cottage will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Looking at the most recent three years, Natural Grocers by Vitamin Cottage recorded free cash flow of 48% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Our View

The good news is that Natural Grocers by Vitamin Cottage's demonstrated ability to cover its interest expense with its EBIT delights us like a fluffy puppy does a toddler. But, on a more sombre note, we are a little concerned by its level of total liabilities. When we consider the range of factors above, it looks like Natural Grocers by Vitamin Cottage is pretty sensible with its use of debt. While that brings some risk, it can also enhance returns for shareholders. We'd be motivated to research the stock further if we found out that Natural Grocers by Vitamin Cottage insiders have bought shares recently. If you would too, then you're in luck, since today we're sharing our list of reported insider transactions for free.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if Natural Grocers by Vitamin Cottage might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About NYSE:NGVC

Natural Grocers by Vitamin Cottage

Natural Grocers by Vitamin Cottage, Inc., together with its subsidiaries, retails natural and organic groceries, and dietary supplements in the United States.

Outstanding track record with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|35.7% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|20.5% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|25.2% overvalued

DA

Community Contributor