Advertisement

- United States

- /

- Food and Staples Retail

- /

- NYSE:DG

Is Dollar General’s 44% Rally Justified After Store Modernization and Rural Expansion News?

Simply Wall St

Reviewed by Bailey Pemberton

- Wondering if Dollar General stock is delivering the value smart investors are seeking? Here’s what you need to know to decide whether it makes sense for your portfolio.

- After a difficult few years, Dollar General shares have increased 44.4% over the past year and gained 43.8% year-to-date. This performance has sparked fresh conversation about growth potential and shifting risk.

- Recent news has highlighted Dollar General’s strategic investments in store modernization and rural expansion, which has fueled optimism among analysts and investors. At the same time, the company’s cost-control efforts have come into focus as key factors in the stock’s turnaround story.

- On our valuation checks, Dollar General is considered undervalued in 4 out of 6 categories, scoring a 4/6. How a stock is valued matters just as much as the final score, and we’ll explore an even deeper way to understand value by the end of this article.

Approach 1: Dollar General Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow (DCF) model estimates a company's value by projecting its future cash flows and discounting them back to today's dollars. This method helps investors understand what a business is worth based strictly on its ability to generate cash in the future.

For Dollar General, the DCF model uses the 2 Stage Free Cash Flow to Equity approach. The company's most recent twelve-month free cash flow came in at $1.56 billion. Analysts' projections suggest that annual free cash flow could reach approximately $1.83 billion by 2030, based on both analyst estimates for the first five years and longer-term extrapolations.

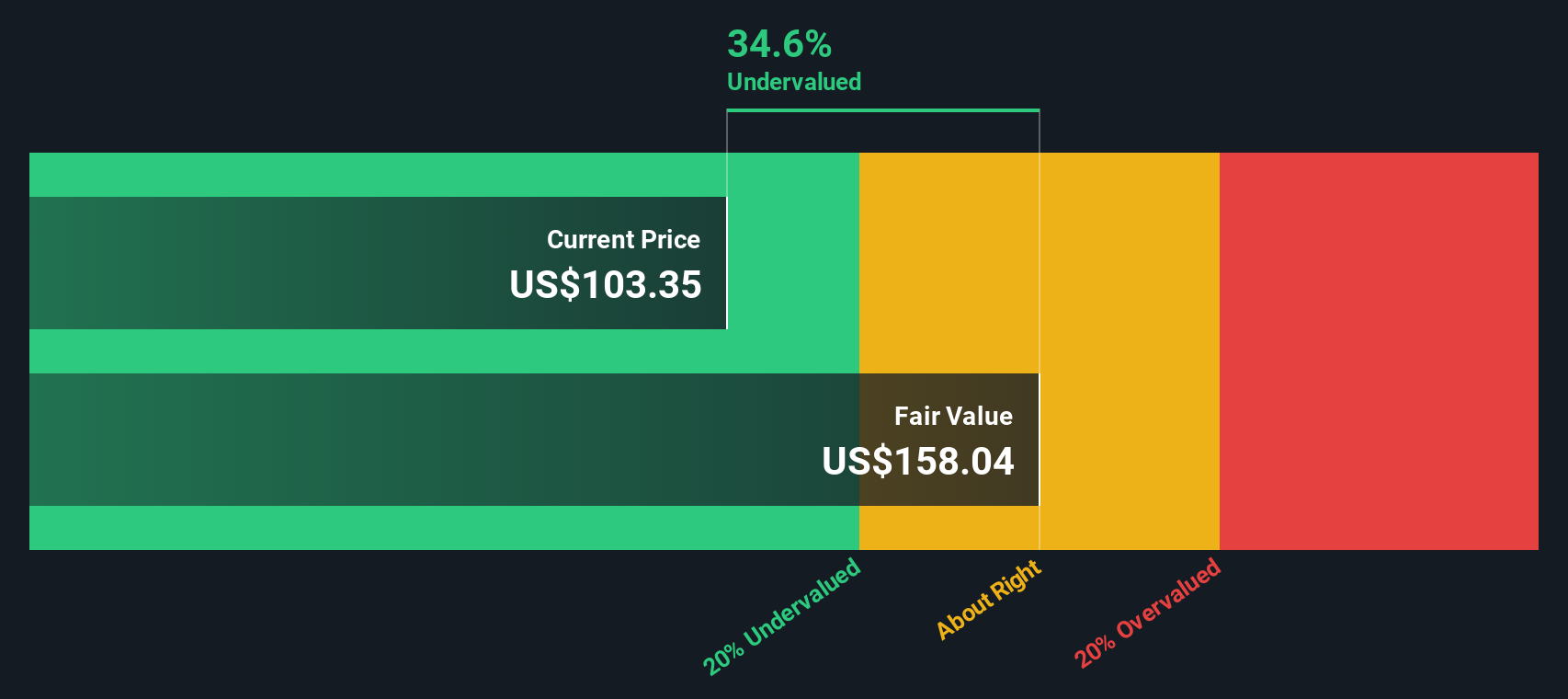

With these inputs, the model calculates a fair intrinsic value of $160.84 per share. This suggests that Dollar General is currently trading at a 32.4% discount compared to where the DCF model indicates fair value should be. In summary, Dollar General appears to be significantly undervalued based on cash flow fundamentals.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests Dollar General is undervalued by 32.4%. Track this in your watchlist or portfolio, or discover 923 more undervalued stocks based on cash flows.

Approach 2: Dollar General Price vs Earnings

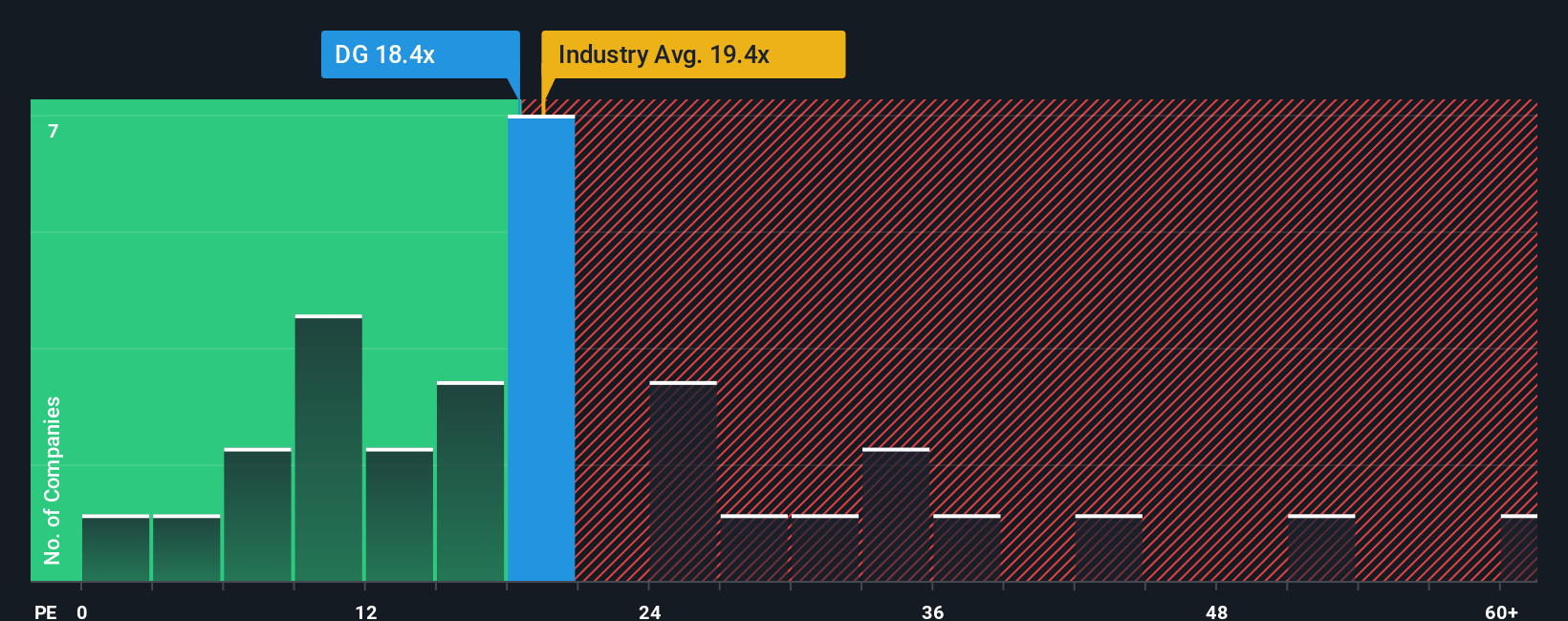

The price-to-earnings (PE) ratio is often the go-to metric when valuing profitable companies like Dollar General. It offers a simple yet effective way to gauge how much investors are willing to pay today for each dollar of earnings, making it highly relevant for established businesses generating steady profits.

A company's “normal” or “fair” PE ratio is shaped by growth expectations and perceived risks. Faster-growing, lower-risk companies typically command higher PE ratios, while slower-growing or riskier companies tend to attract lower multiples.

Currently, Dollar General trades at a PE ratio of 20.1x. This is slightly above the average of its industry peers at 19.3x, and roughly in line with the overall Consumer Retailing industry average of 20.1x. However, a more tailored view comes from Simply Wall St’s “Fair Ratio,” a proprietary benchmark designed to reflect the multiple Dollar General deserves considering factors such as its earnings growth outlook, profit margins, industry landscape, market cap, and company-specific risks.

Unlike a basic peer or industry comparison, the Fair Ratio integrates all key company dynamics and tailors the expected multiple accordingly. For Dollar General, the calculated Fair Ratio stands at 21.3x, just a shade above its current multiple.

With the actual PE ratio at 20.1x and the Fair Ratio at 21.3x, Dollar General is trading only slightly below its fair value multiple. This suggests that, on a PE basis, the stock is about right.

Result: ABOUT RIGHT

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1439 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose Your Dollar General Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let’s introduce you to Narratives. A Narrative is a simple, flexible story you create around Dollar General based on your personal perspective, your expectations for its future revenue, profit margins, and what you see driving or hindering growth. You can turn those assumptions into a financial forecast and fair value. Narratives link the company’s unique story to the numbers, giving meaning to the data and clarity to your investment decisions.

Narratives are an easy and accessible tool on Simply Wall St’s Community page, already used by millions of investors. They help you decide when to buy, sell, or hold by directly comparing your calculated fair value to the current share price. They automatically update as new news or earnings emerge, so your view always stays current.

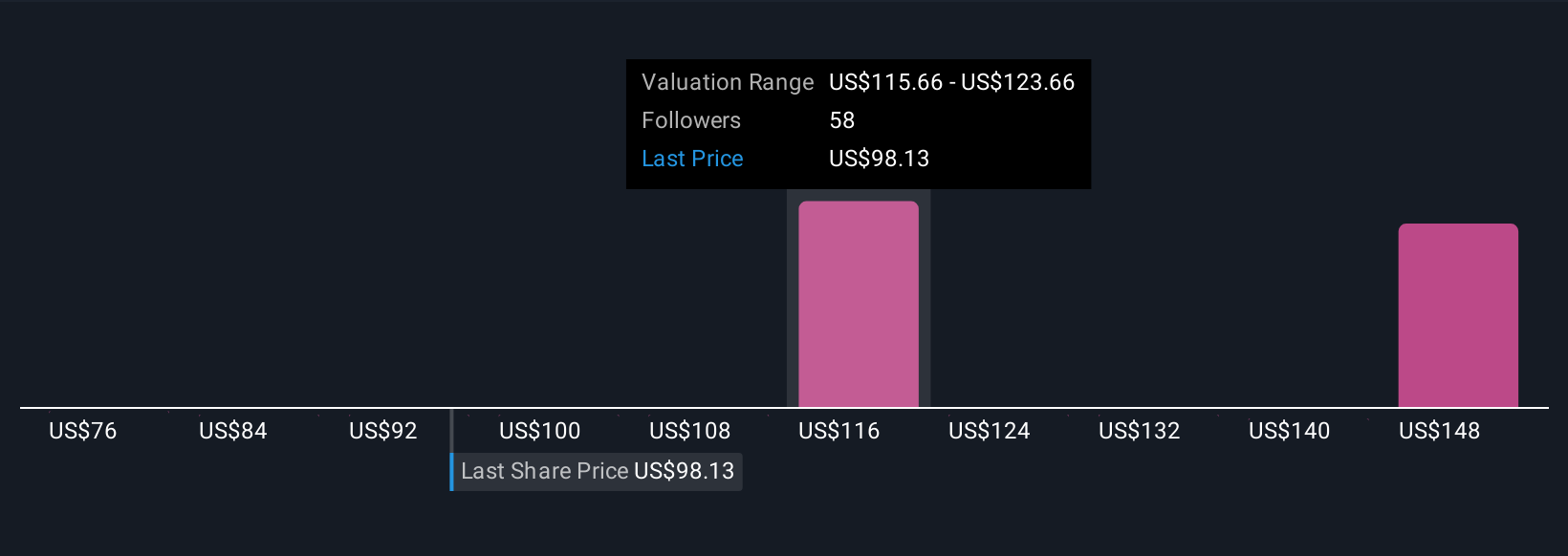

For example, some investors may focus on aggressive store expansion and digital strategies, forecasting strong earnings and setting a fair value above $138 per share. Others may worry about competition and rising costs, estimating a fair value closer to $80 per share. Narratives empower you to visualize and act on your unique viewpoint, blending company stories and financial rigor for smarter, more dynamic decision making.

Do you think there's more to the story for Dollar General? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:DG

Dollar General

A discount retailer, provides various merchandise products in the southern, southwestern, midwestern, and eastern United States.

Established dividend payer and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.8% undervalued

TI

Community Contributor

Recently Updated Narratives

AL

AlexLovell on Rocket Lab ·

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

Fair Value:US$16.25158.0% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on ANYCOLOR ·

Near zero debt, Japan centric focus provides future growth

Fair Value:JP¥7.61k15.3% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

CO

composite32 on TAV Havalimanlari Holding ·

TAV Havalimanlari Holding will fly high with 25.68% revenue growth

Fair Value:₺545.1648.6% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

93 followersusers have followed this narrative

10 commentsusers have commented on this narrative

18 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.9% undervalued

136 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$232.7922.6% undervalued

929 followersusers have followed this narrative

6 commentsusers have commented on this narrative

22 likesusers have liked this narrative