- United States

- /

- Food and Staples Retail

- /

- NasdaqGS:DLTR

Dollar Tree (DLTR) Partners With Uber for Nationwide Delivery Through Uber Eats

Reviewed by Simply Wall St

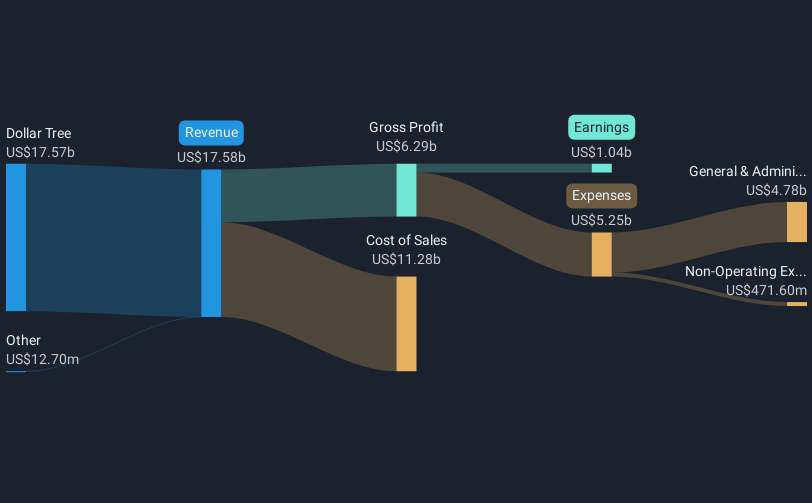

Dollar Tree (DLTR) recently benefited from a 25% price increase over the last quarter, with several key events likely contributing to this upward trajectory. The partnership with Uber Technologies, enabling on-demand delivery from nearly 9,000 Dollar Tree stores, aligns with trends of expanding retail convenience and e-commerce integration. Additionally, the company's increased share buyback authorization and strong Q1 earnings—exceeding both revenue and net income from the previous year—may have fortified investor confidence. Meanwhile, the broader market trends, with major indexes reaching record highs, likely provided additional support to Dollar Tree's share price performance.

We've spotted 3 weaknesses for Dollar Tree you should be aware of.

The recent developments at Dollar Tree, particularly its strategic alliance with Uber Technologies for on-demand delivery and the company's decision to increase share buybacks, hold potential implications for its operational narrative. These moves could enhance Dollar Tree's retail convenience and margin stability. Dollar Tree's focus on core business activities post-Family Dollar sale, combined with store format updates, is poised to improve efficiency and customer engagement. These initiatives support forecasted revenue and earnings growth. Analysts expect earnings to rise to US$1.4 billion by 2028, suggesting optimism about long-term value creation.

Over the past year, Dollar Tree's total shareholder return was 33.11%. Notably, this outperformed both the broader US market, which returned 16.2%, and the US Consumer Retailing industry, which saw a 14.6% gain over the same period. This performance underscores Dollar Tree's ability to capitalize on market trends and operational improvements.

The current share price of US$112.86 slightly exceeds the average analyst price target of US$110.43, indicating a 2% premium. This suggests that the market is pricing in recent positive developments, although the consensus implies a fair valuation near current levels. Investors should consider these dynamics when assessing potential future performance against the backdrop of Dollar Tree's strategic initiatives and market trends.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NasdaqGS:DLTR

Dollar Tree

Operates retail discount stores under the Dollar Tree and Dollar Tree Canada brands in the United States and Canada.

Adequate balance sheet with acceptable track record.

Similar Companies

Market Insights

Community Narratives