Advertisement

- United States

- /

- Luxury

- /

- NYSE:VFC

V.F Corp (VFC): Assessing Valuation Following Analyst Upgrade and Renewed Optimism on Turnaround Prospects

Kshitija Bhandaru

Reviewed by Simply Wall St

V.F (VFC) just got a confidence boost, with Baird upgrading the stock based on signs of a turnaround in the Vans brand, better product momentum, and clear progress on cost-cutting and debt management. This nod from analysts seems to have brightened investor spirits, especially as it lines up with the company’s announced changes to its revolving credit facility, giving them more financial flexibility to support their transformation plans. For shareholders on the sidelines, it is the kind of event that can lift uncertainty and spark new debates about where V.F goes next.

Zooming out, the recent analyst upgrade comes as V.F has shown signs of renewed momentum after a tough stretch. Over the past month, shares jumped nearly 30%, suggesting a shift in market sentiment following several quarters of disappointing returns. Still, looking at the bigger picture over the past year, the stock is down 18%, and the longer-term trajectory remains challenging with a decline of 74% from five years ago. That volatility helps set the stage for a deeper conversation about the company’s true value now that optimism is starting to build again.

So after this dramatic swing in share price over the month, are investors getting a rare chance to buy into a turnaround story, or is all of the good news already reflected in today’s valuation?

Most Popular Narrative: 0.4% Undervalued

The most widely followed narrative puts V.F just under its fair value, suggesting a balanced outlook between future opportunity and present challenges based on forecasted financial improvements.

The strategic focus on expanding higher-margin channels, including direct-to-consumer and e-commerce, is beginning to drive improved gross margins and deeper customer engagement. These efforts are expected to lift both revenue growth and net margins over time as V.F. capitalizes on the sustained consumer shift toward digital and premium shopping experiences.

Want to know what is powering this surprising fair value? This narrative is built on bold profit forecasts and a future price multiple rarely seen in this sector. Curious what assumptions underpin these projections for V.F’s rebound? The full story reveals the numbers driving a price target that nearly matches today’s market price.

Result: Fair Value of $15.19 (ABOUT RIGHT)

Have a read of the narrative in full and understand what's behind the forecasts.However, persistent challenges at big brands like Vans, or renewed pressure from tariff headwinds, could quickly undermine analyst optimism and stall a sustained recovery.

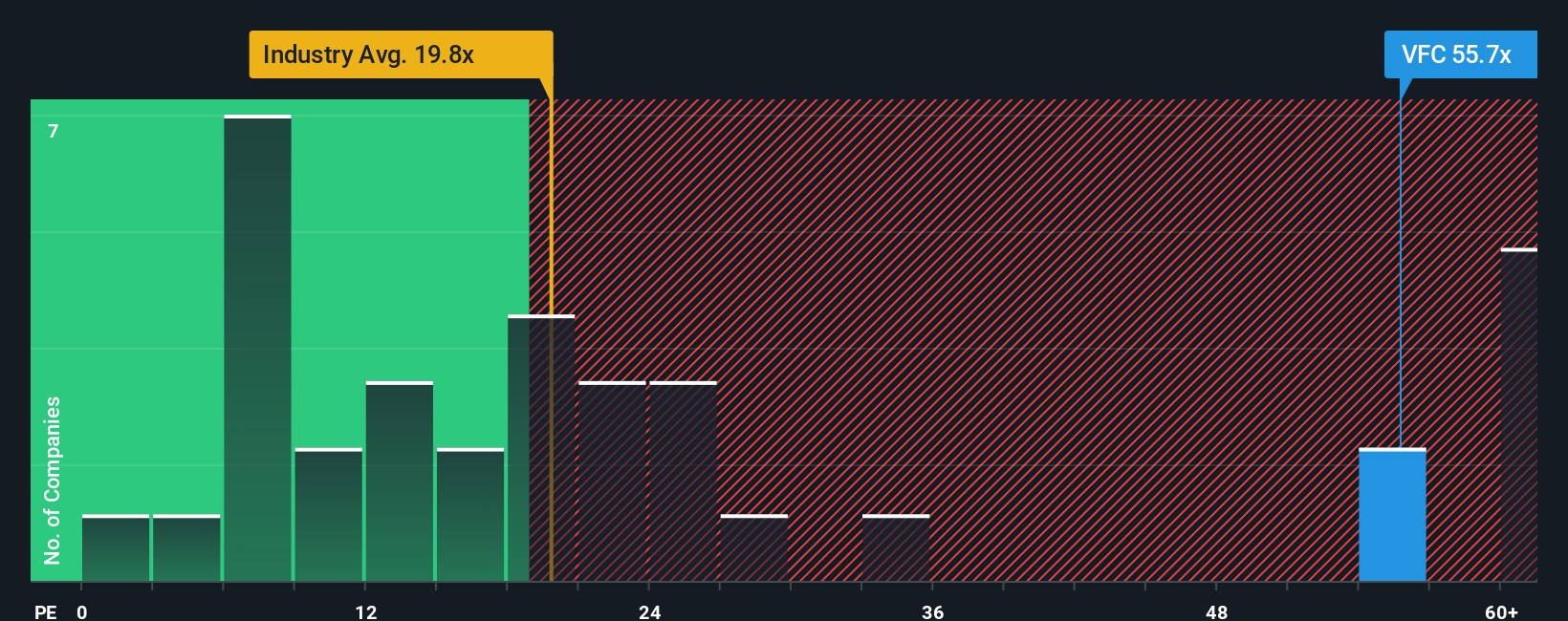

Find out about the key risks to this V.F narrative.Another View: Multiples Still Look Expensive

While some models hint at a fair price, looking at earnings multiples compared to industry averages raises doubts. V.F trades at a much higher level, which could point to optimism already priced in. Could the market be missing something?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own V.F Narrative

If you want to take a fresh perspective or analyze the numbers for yourself, you can easily build a custom narrative in just minutes. Do it your way

A great starting point for your V.F research is our analysis highlighting 3 key rewards and 3 important warning signs that could impact your investment decision.

Looking for more investment ideas?

Step ahead of the crowd by finding tomorrow’s winners today. The Simply Wall Street Screener offers a shortcut to smart, data-driven opportunities that other investors might overlook.

- Take advantage of the momentum in stocks undervalued by strong cash flows with our latest undervalued stocks based on cash flows.

- Explore emerging technologies and potential breakthroughs with a handpicked selection of AI penny stocks.

- Add reliability to your portfolio with income builders by accessing companies offering dividend stocks with yields > 3%.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Kshitija Bhandaru

Kshitija (or Keisha) Bhandaru is an Equity Analyst at Simply Wall St and has over 6 years of experience in the finance industry and describes herself as a lifelong learner driven by her intellectual curiosity. She previously worked with Market Realist for 5 years as an Equity Analyst.

About NYSE:VFC

V.F

Offers branded apparel, footwear, and accessories for men, women, and children in the Americas, Europe, and the Asia-Pacific.

Reasonable growth potential with low risk.

Similar Companies

Market Insights

Advertisement

Weekly Picks

RO

RockeTeller on Santacruz Silver Mining ·

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

Fair Value:CA$8696.7% undervalued

21 followersusers have followed this narrative

6 commentsusers have commented on this narrative

5 likesusers have liked this narrative

RO

Robbo on Fiducian Group ·

Fiducian: Compliance Clouds or Value Opportunity?

Fair Value:AU$126.1% undervalued

3 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

WO

woodworthfund on Willamette Valley Vineyards ·

Willamette Valley Vineyards (WVVI): Not-So-Great Value

Fair Value:US$242.5% overvalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

1 likeusers have liked this narrative

Recently Updated Narratives

MA

MarkoVT on Alphabet ·

Positioned globally, partnered locally

Fair Value:US$390.1919.1% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

JO

JohnJ on Worldline ·

When will fraudsters be investigated in depth. Fraud was ongoing in France too.

Fair Value:€0.5200.8% overvalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

MA

MarkoVT on Applied Digital ·

Staggered by dilution; positions for growth

Fair Value:US$35.4520.9% undervalued

4 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.6% undervalued

112 followersusers have followed this narrative

11 commentsusers have commented on this narrative

22 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3927.5% undervalued

949 followersusers have followed this narrative

6 commentsusers have commented on this narrative

24 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3407.1% undervalued

148 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative