Advertisement

- United States

- /

- Consumer Durables

- /

- OTCPK:TUPB.Q

Returns On Capital At Tupperware Brands (NYSE:TUP) Have Stalled

If you're looking for a multi-bagger, there's a few things to keep an eye out for. In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. Ultimately, this demonstrates that it's a business that is reinvesting profits at increasing rates of return. So while Tupperware Brands (NYSE:TUP) has a high ROCE right now, lets see what we can decipher from how returns are changing.

Return On Capital Employed (ROCE): What is it?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. To calculate this metric for Tupperware Brands, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

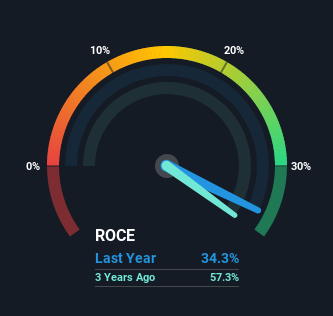

0.34 = US$240m ÷ (US$1.3b - US$556m) (Based on the trailing twelve months to December 2021).

Thus, Tupperware Brands has an ROCE of 34%. That's a fantastic return and not only that, it outpaces the average of 15% earned by companies in a similar industry.

See our latest analysis for Tupperware Brands

In the above chart we have measured Tupperware Brands' prior ROCE against its prior performance, but the future is arguably more important. If you'd like, you can check out the forecasts from the analysts covering Tupperware Brands here for free.

What Does the ROCE Trend For Tupperware Brands Tell Us?

We're a bit concerned with the trends, because the business is applying 33% less capital than it was five years ago and returns on that capital have stayed flat. When a company effectively decreases its assets base, it's not usually a sign to be optimistic on that company. However, the business's operational efficiency is still impressive considering the ROCE is high in absolute terms.

On a side note, Tupperware Brands' current liabilities are still rather high at 44% of total assets. This can bring about some risks because the company is basically operating with a rather large reliance on its suppliers or other sorts of short-term creditors. Ideally we'd like to see this reduce as that would mean fewer obligations bearing risks.

The Bottom Line On Tupperware Brands' ROCE

It's a shame to see that Tupperware Brands is effectively shrinking in terms of its capital base. Since the stock has declined 66% over the last five years, investors may not be too optimistic on this trend improving either. In any case, the stock doesn't have these traits of a multi-bagger discussed above, so if that's what you're looking for, we think you'd have more luck elsewhere.

One more thing: We've identified 3 warning signs with Tupperware Brands (at least 1 which doesn't sit too well with us) , and understanding these would certainly be useful.

If you'd like to see other companies earning high returns, check out our free list of companies earning high returns with solid balance sheets here.

Valuation is complex, but we're here to simplify it.

Discover if Tupperware Brands might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About OTCPK:TUPB.Q

Tupperware Brands

Operates as a consumer products company in the Asia Pacific, Europe, Africa, the Middle East, North America, and South America.

Low with weak fundamentals.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|6.3% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|26.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.7% overvalued

LI

Community Contributor