Advertisement

- United States

- /

- Leisure

- /

- NYSE:PII

Can Analyst Sentiment Shift and Flagship Event Revive Polaris’s (PII) Brand Strength?

Simply Wall St

Reviewed by Sasha Jovanovic

- On October 1, 2025, Citigroup analyst James Hardiman upgraded Polaris from a "Sell" to a "Neutral" rating, signaling a significant change in analyst sentiment for the company.

- This shift coincided with Polaris announcing the return of its flagship Camp RZR event and the launch of new product innovations, highlighting efforts to strengthen its brand and community engagement.

- We'll look at how Citigroup's upgraded outlook shapes Polaris's investment narrative amid its push to enhance brand and product offerings.

Find companies with promising cash flow potential yet trading below their fair value.

Polaris Investment Narrative Recap

To believe in Polaris as an investment, you need confidence in its ability to drive demand for premium powersports vehicles, manage tariff headwinds, and grow through innovation. Citigroup’s recent upgrade of Polaris to a "Neutral" from "Sell" and the higher price target may influence short-term sentiment, but fundamental threats, especially tariff-related cost uncertainty, remain the biggest near-term risk, while product momentum stands as the primary catalyst. The impact of this analyst action on either the tariff risk or product demand catalyst is, at this stage, not material.

Of Polaris’s recent news, the launch of the 2026 RANGER 500 is particularly interesting, aligning with management’s emphasis on new product introductions to stimulate interest and offset demand challenges. For investors, such announcements keep focus on the company's efforts to create momentum around its updated portfolio and could positively impact near-term retail sales volumes, though heightened cost pressures may temper these gains.

Yet, against signs of improved sentiment, the ongoing threat of higher tariff costs remains a risk investors must keep in mind...

Read the full narrative on Polaris (it's free!)

Polaris' outlook anticipates $7.5 billion in revenue and $224.6 million in earnings by 2028. This is based on a projected 2.4% annual revenue growth rate and a $332.4 million increase in earnings from the current level of -$107.8 million.

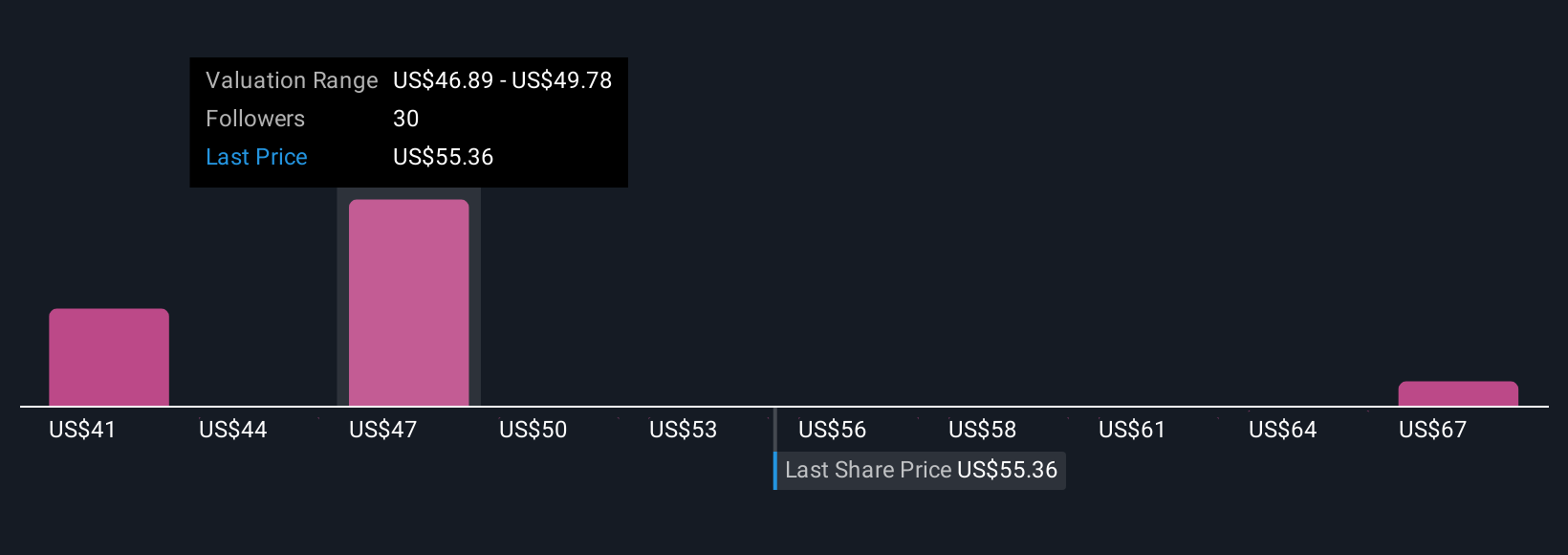

Uncover how Polaris' forecasts yield a $52.00 fair value, a 19% downside to its current price.

Exploring Other Perspectives

Six fair value estimates from the Simply Wall St Community span a wide US$42.41 to US$70 range. With tariff uncertainties still weighing on potential earnings, you can see how opinions vary on Polaris’s performance outlook, so explore all viewpoints.

Explore 6 other fair value estimates on Polaris - why the stock might be worth 34% less than the current price!

Build Your Own Polaris Narrative

Disagree with existing narratives? Create your own in under 3 minutes - extraordinary investment returns rarely come from following the herd.

- A great starting point for your Polaris research is our analysis highlighting 2 key rewards and 2 important warning signs that could impact your investment decision.

- Our free Polaris research report provides a comprehensive fundamental analysis summarized in a single visual - the Snowflake - making it easy to evaluate Polaris' overall financial health at a glance.

Contemplating Other Strategies?

Our daily scans reveal stocks with breakout potential. Don't miss this chance:

- Outshine the giants: these 24 early-stage AI stocks could fund your retirement.

- We've found 19 US stocks that are forecast to pay a dividend yield of over 6% next year. See the full list for free.

- AI is about to change healthcare. These 32 stocks are working on everything from early diagnostics to drug discovery. The best part - they are all under $10b in market cap - there's still time to get in early.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PII

Polaris

Designs, engineers, manufactures, and markets powersports vehicles in the United States, Canada, and internationally.

Reasonable growth potential with adequate balance sheet and pays a dividend.

Similar Companies

Market Insights

Advertisement

Community Narratives

The Next Phase of Energy Storage: How NeoVolta Is Tackling America’s Power Crunch

Fair Value US$7.50|35.1% undervalued

MA

Community Contributor

Why EnSilica is Worth Possibly 13x its Current Price

Fair Value UK£5.00|89.8% undervalued

DO

Community Contributor

M&A Activity, Industry Diversification & A Defense Contract Monopoly Will Push BWXT For Healthy Long-Term Growth

Fair Value US$220.00|15.2% undervalued

CL

Community Contributor

A case for Cassiar Gold Corp (TSXV: GLDC) to reach CAD$8-10 before 2030 (X30-37)

Fair Value CA$10.00|96.0% undervalued

AG

Community Contributor