- United States

- /

- Consumer Durables

- /

- NYSE:PHM

Can PulteGroup’s Strong Multi Year Rally Still Offer Value in 2025?

Reviewed by Bailey Pemberton

- If you are wondering whether PulteGroup's stock still offers value after a strong run, you are not alone. This article is designed to unpack exactly that question in plain language.

- The share price has climbed about 1.1% over the last week, 5.1% over the past month, and is up 15.6% year to date, adding to a striking 184.5% gain over 3 years and 187.6% over 5 years.

- Some of this momentum has been driven by ongoing strength in US housing demand and builder confidence, as markets continue to digest structurally tight housing supply and a gradual shift in interest rate expectations. Investors are also reacting to policy debates around housing incentives and infrastructure, which could meaningfully affect long term order growth and land values for large homebuilders like PulteGroup.

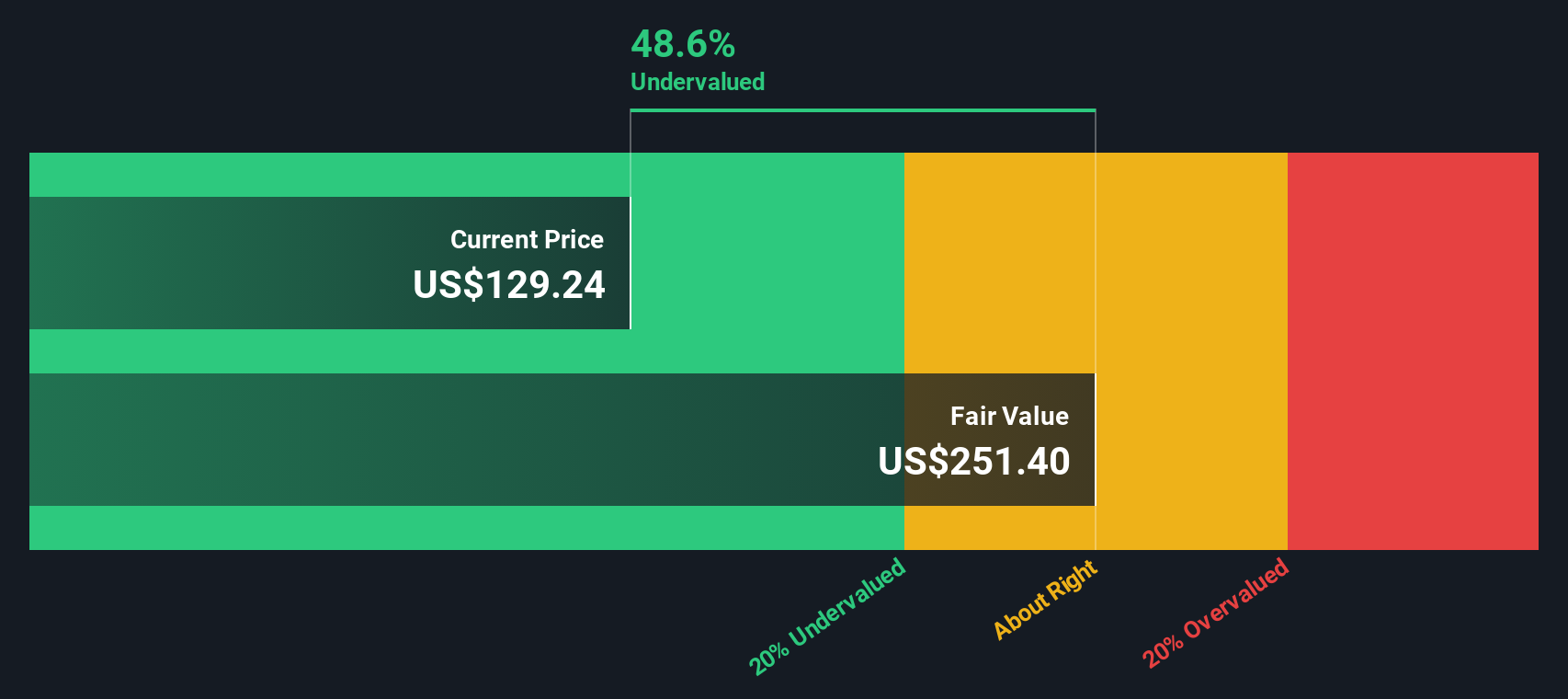

- Despite those gains, PulteGroup scores a 4/6 on our valuation checks. This suggests it still screens as undervalued on most, but not all, metrics. Next we will walk through the main valuation approaches, before finishing with a more holistic way to think about what the market might be missing.

Approach 1: PulteGroup Discounted Cash Flow (DCF) Analysis

A Discounted Cash Flow model estimates what a business is worth today by projecting the cash it could generate in the future and then discounting those cash flows back to their value in $ today.

For PulteGroup, the model starts with last twelve months Free Cash Flow of about $1.56 billion and uses analyst forecasts for the next few years, then gradually tapers growth in later years based on Simply Wall St extrapolations. By 2035, annual Free Cash Flow is projected to be roughly $2.03 billion in $ terms, reflecting steady but moderating growth as the business matures.

Adding up all of those discounted cash flows under a 2 Stage Free Cash Flow to Equity framework gives an estimated intrinsic value of about $153.86 per share. Compared with the current share price, the DCF implies PulteGroup is trading at roughly a 19.2% discount. This suggests there could be meaningful upside if these cash flow assumptions prove accurate.

Result: UNDERVALUED

Our Discounted Cash Flow (DCF) analysis suggests PulteGroup is undervalued by 19.2%. Track this in your watchlist or portfolio, or discover 910 more undervalued stocks based on cash flows.

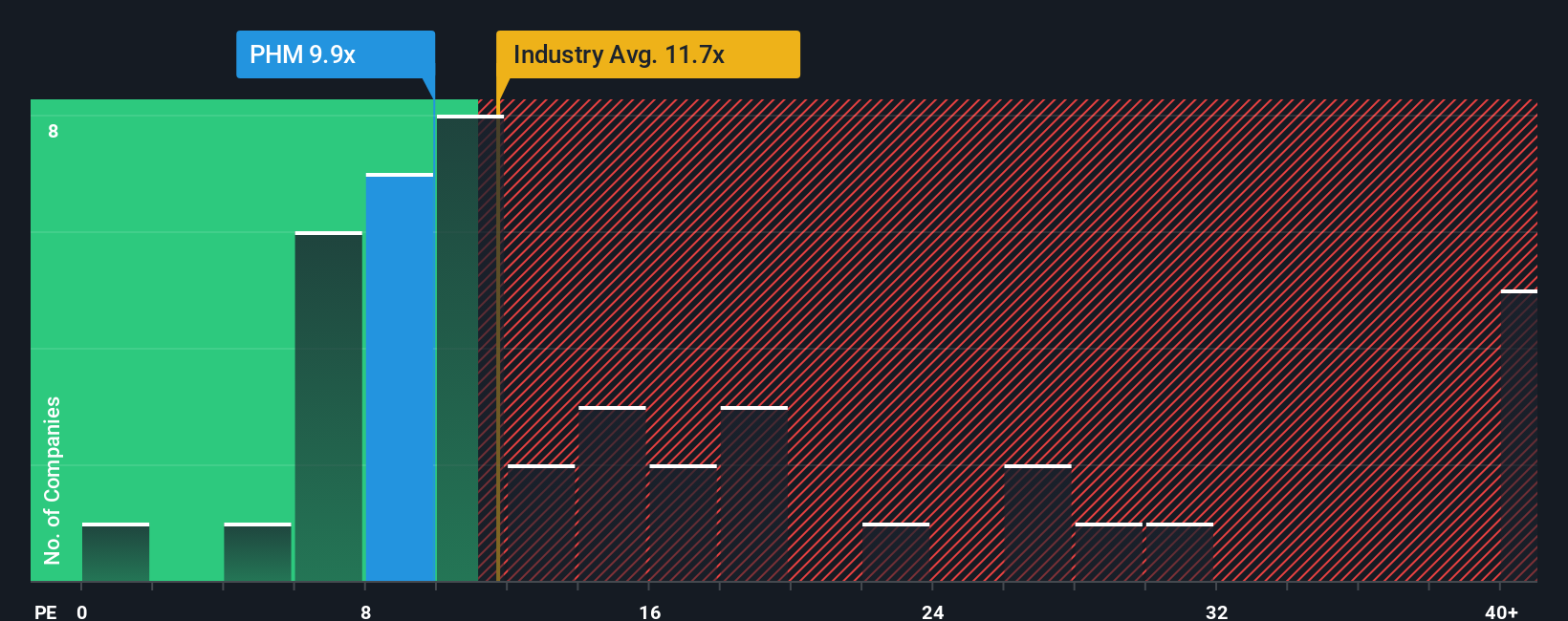

Approach 2: PulteGroup Price vs Earnings

For profitable companies like PulteGroup, the price to earnings, or PE, ratio is a straightforward way to see how much investors are willing to pay for each dollar of current earnings. A higher PE typically reflects stronger growth expectations or lower perceived risk, while a lower PE can signal slower growth, higher risk, or a potential bargain if the outlook is better than the market assumes.

PulteGroup currently trades on a PE of about 9.22x, which is below both the Consumer Durables industry average of roughly 10.66x and the broader peer group average of around 12.06x. Simply Wall St also calculates a proprietary Fair Ratio for each company. This is the PE you might reasonably expect given its earnings growth outlook, profitability, industry, market cap, and specific risk profile, rather than just how it compares with a generic peer set.

For PulteGroup, that Fair Ratio is estimated at about 15.56x, well above the current 9.22x. This gap suggests the market is not fully crediting the company for its fundamentals and risk profile, which points to a stock that still appears attractively priced on earnings.

Result: UNDERVALUED

PE ratios tell one story, but what if the real opportunity lies elsewhere? Discover 1463 companies where insiders are betting big on explosive growth.

Upgrade Your Decision Making: Choose your PulteGroup Narrative

Earlier we mentioned that there is an even better way to understand valuation. Let us introduce you to Narratives, a simple tool on Simply Wall St's Community page that lets you connect your view of PulteGroup's story with your own revenue, earnings, and margin assumptions. You can then link that forecast to a Fair Value and compare it to the current share price to decide whether to buy or sell. The numbers update dynamically as new news and earnings arrive. For example, a more optimistic investor might build a Narrative where resilient active adult demand, Sunbelt migration and margin discipline justify a Fair Value closer to the high analyst target of around 163 dollars. A more cautious investor could create a Narrative that leans into affordability risks, softer volumes and sector multiple pressure, landing nearer the low end of about 98 dollars. Each Narrative transparently shows how changes in the story flow through to the forecast and ultimately to what investors believe the stock is worth today.

Do you think there's more to the story for PulteGroup? Head over to our Community to see what others are saying!

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:PHM

PulteGroup

Through its subsidiaries, engages in the homebuilding business in the United States.

Flawless balance sheet, good value and pays a dividend.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Sunrun Stock: When the Energy Transition Collides With the Cost of Capital

Popular Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)