Advertisement

- United States

- /

- Luxury

- /

- NYSE:HBI

A Look at Hanesbrands’s Valuation as Premium Strategy Boosts Optimism but Turnaround Hurdles Remain

Simply Wall St

Reviewed by Kshitija Bhandaru

Hanesbrands (HBI) shares have taken a positive turn amid renewed investor optimism, following its shift toward premium products, increased brand investment, and new offerings in categories like loungewear and scrubs. This strategy is sparking fresh debate over the company’s long-term trajectory.

See our latest analysis for Hanesbrands.

Hanesbrands’ recent rally, with an 8% share price return in the last month and a striking 47% jump over 90 days, signals that momentum is building as investors warm to its turnaround story. Yet, it’s worth noting the longer view remains mixed, with one-year total shareholder return still in the red at -5%, reflecting persistent turnaround challenges even as optimism grows.

If you’re watching these shifts and want to spot other companies with strong growth and management buy-in, now’s the perfect time to discover fast growing stocks with high insider ownership

With the stock rallying in recent months, investors face a crucial question: is Hanesbrands still undervalued after its run, or is the market already baking in the next phase of growth?

Most Popular Narrative: 11% Overvalued

With Hanesbrands closing at $6.97, the most popular narrative’s fair value lands at $6.26, pointing to the stock trading above analyst consensus. This sets the stage for a deeper look at the assumptions shaping this view.

Investments in e-commerce, direct-to-consumer channels, and exclusive partnerships (for example, Urban Outfitters and specialty retailers in Japan) are expanding reach and customer engagement, supporting higher revenues and an ongoing shift toward structurally higher margins through channel mix improvements.

Want to know what projections drive this pricing tension? See which ambitious assumptions about future earnings, margins, and market access give this outlook its edge. The full story reveals the financial strategies and growth bets analysts are staking Hanesbrands’ value on.

Result: Fair Value of $6.26 (OVERVALUED)

Have a read of the narrative in full and understand what's behind the forecasts.

However, ongoing softness in U.S. intimates and rising competition from private label brands could challenge Hanesbrands’ ability to sustain revenue growth in key categories.

Find out about the key risks to this Hanesbrands narrative.

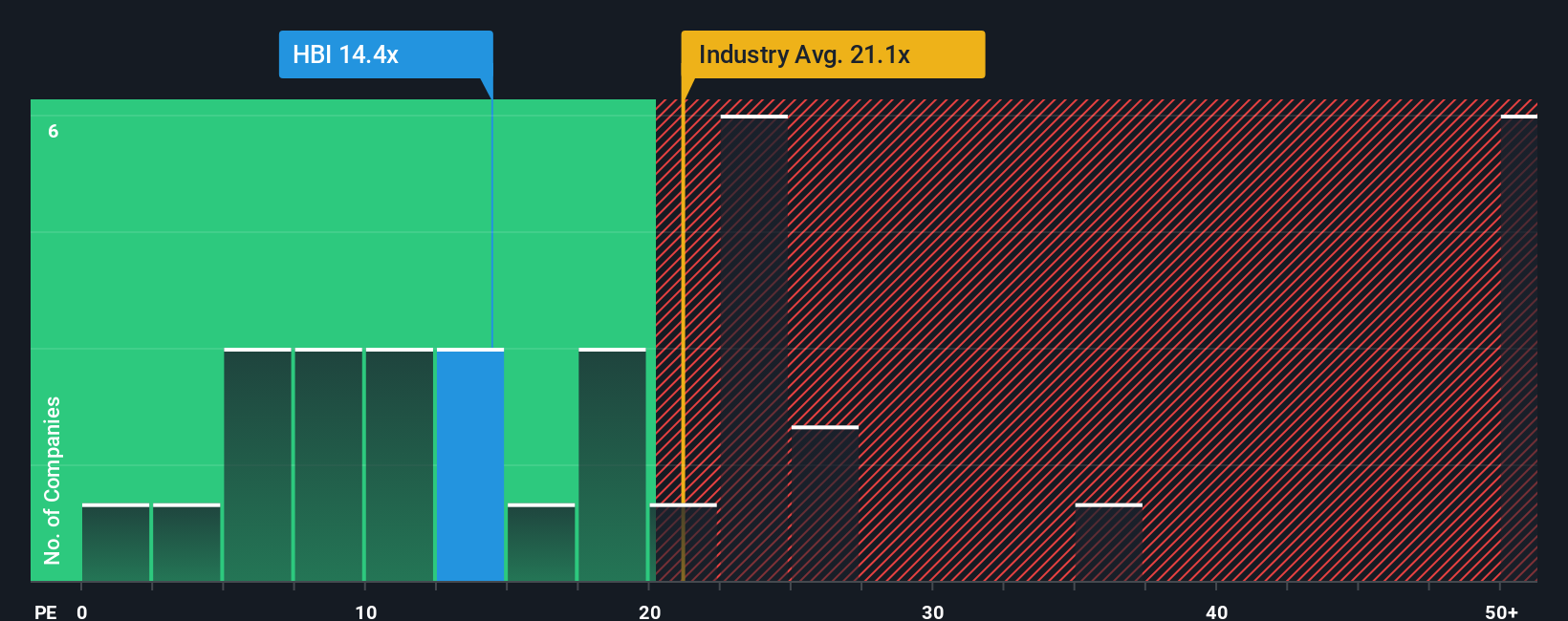

Another View: What Multiples Say

Looking instead at Hanesbrands' price-to-earnings ratio, the data shows the company trading at 14.5x, which is lower than both the US Luxury industry average of 20.5x and the peer average of 16.5x. It’s also below the fair ratio of 18.1x, suggesting more value than the first method implies. Does this mean risk is lower, or is the market just less optimistic?

See what the numbers say about this price — find out in our valuation breakdown.

Build Your Own Hanesbrands Narrative

If you see things differently, or want to dig deeper on your own terms, you can easily build a custom view in just a few minutes. Do it your way

A great starting point for your Hanesbrands research is our analysis highlighting 4 key rewards and 1 important warning sign that could impact your investment decision.

Looking for more investment ideas?

Smart investors never settle for the obvious. Broaden your opportunities by tapping into winning stock picks powered by the Simply Wall Street Screener. Don’t let a great opportunity slip by.

- Grab a head start on tomorrow’s market movers with these 3573 penny stocks with strong financials, highlighting companies with robust potential you won’t want to overlook.

- Catch trends in artificial intelligence early by scanning these 25 AI penny stocks, where breakthrough innovators are pushing the limits of what’s possible with smart technology.

- Secure your portfolio’s potential by zeroing in on real value. Find strong candidates at compelling prices in these 887 undervalued stocks based on cash flows.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Hanesbrands might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About NYSE:HBI

Hanesbrands

Designs, manufactures, sources, and sells a range of range of innerwear apparel for men, women, and children in the Americas, Europe, the Asia pacific, and internationally.

Good value with limited growth.

Similar Companies

Market Insights

Advertisement

Community Narratives

A formidable player in AI and enterprise computing.

Fair Value US$210.00|12.2% overvalued

CO

Community Contributor

IREN's Bold Moves in Sustainable Bitcoin Mining & AI Data Centers

Fair Value US$72.52|17.1% undervalued

BL

Community Contributor

Cooling the Champions: The Aussie Tech Behind F1's Victories

Fair Value AU$12.40|38.1% undervalued

TR

Community Contributor